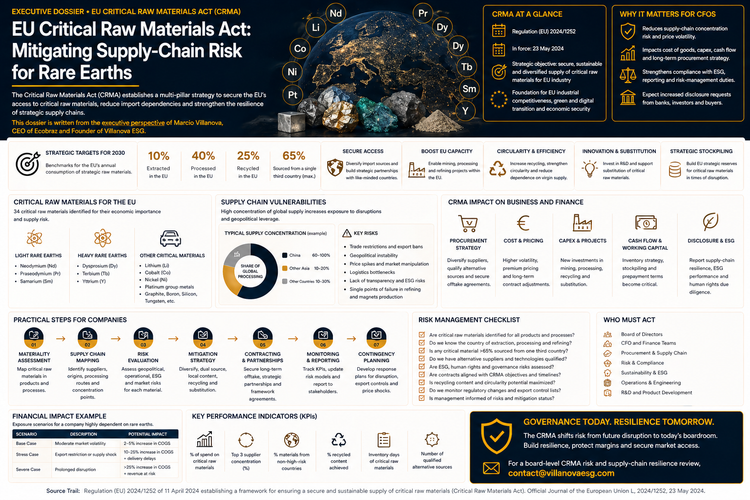

EU Critical Raw Materials Act: Mitigating Supply-Chain Risk for Rare Earths

The EU Critical Raw Materials Act turns rare earths and strategic minerals into a board-level supply-chain resilience test. CFOs must map material dependency, supplier concentration, price shocks, processing bottlenecks and ESG due diligence before disruption compresses margins.

Green Claims Risk: Proving Environmental Statements Under New EU Rules

Green claims risk did not disappear with the suspended Green Claims proposal. Directive (EU) 2024/825 makes vague environmental statements a legal, commercial and financing exposure from 2026. CFOs must control claims before they become liabilities.

WEEE Open-Scope: Financial Assurance and Producer Responsibility Exposure

WEEE open scope is not new in 2026. It has applied since 15 August 2018. CFOs must control product classification, producer registration, reporting, take-back, financial assurance and back-compliance exposure before EU market access is disrupted.

EU Textile Regulation: Product-Data Proof as Market-Access Risk

EU textile compliance is shifting from claims to product-data proof. CFOs must control composition, durability, recyclability, EPR cost, unsold stock and Digital Product Passport readiness before buyers, customs or market surveillance expose the evidence gap.

EU Forced-Labour Regulation: Import Restrictions and Due-Diligence Obligations

The EU Forced-Labour Regulation turns labour-risk evidence into a market-access control. CFOs must link products to supplier labour-risk data before investigations, buyer requests or customs action freeze revenue.

Board Duties Under CSDDD: Fiduciary Accountability for Supply-Chain Compliance

CSDDD board exposure is not an automatic EU-wide fiduciary-liability rule. It is an oversight, evidence and governance risk that can affect buyer contracts, lender scrutiny, D&O review and cash-flow continuity.

Scope 3 Emissions Baseline Mapping: Unlocking Access to Green Finance

Scope 3 baseline mapping converts supplier emissions from an uncontrolled estimate into finance-grade evidence. CFOs need auditable data to support disclosure, buyer confidence, transition planning and Sustainability-Linked Loan negotiations.

Supply-Chain Opacity: Brown Penalty and WACC Impact for CFOs

Supply-chain opacity can become a Brown Penalty through higher WACC, weaker buyer confidence, tighter financing, contract risk and lower valuation resilience. CFOs must convert supplier uncertainty into verified, finance-grade evidence.

Digital Product Passport: Transforming Primary Data Into Customs Clearance

The Digital Product Passport is becoming a market-access and customs-control system. CFOs must convert product, supplier and compliance data into machine-readable evidence before buyer requests, border checks and financing scrutiny expose the cost of fragmented data.

CSDDD Civil Liability: From 5% Turnover Exposure to the New 3% Sanctions Cap

CSDDD risk has shifted from the original 5% turnover exposure to a revised 3% sanctions cap, narrower scope and national civil liability. CFOs must still control supplier evidence, buyer pressure, litigation exposure and cash-flow risk.