Supply-Chain Opacity: Brown Penalty and WACC Impact for CFOs

Executive Dossier · Supply-Chain Opacity & WACC

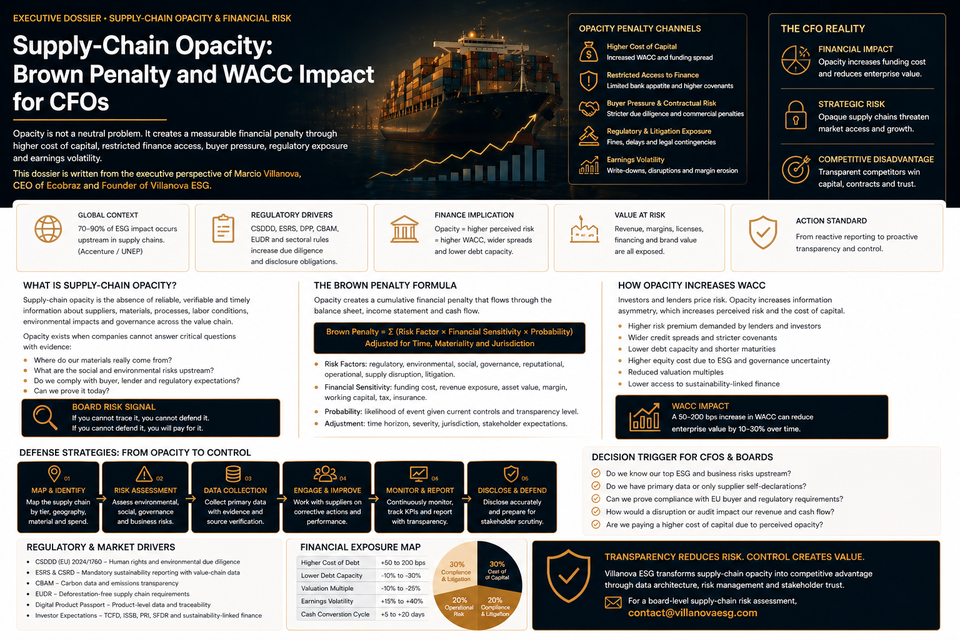

Supply-chain opacity is no longer a procurement weakness. It is a financial penalty that can increase perceived credit risk, compress valuation multiples, restrict financing access and weaken buyer confidence.

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. The analysis treats supply-chain opacity as a cash-flow and cost-of-capital control issue. The board question is direct: can the company prove the origin, risk profile, emissions footprint, labour conditions and compliance status of its upstream value chain before buyers, lenders and regulators price uncertainty into the business?

Risk Type

Information asymmetry

Financial Channel

Higher perceived risk premium

Regulatory Drivers

CSDDD · CBAM · EUDR · CSRD · DPP

Value at Risk

Margins, credit, contracts, valuation

Supply-Chain Opacity Has Become a Financial Variable

Supply-chain opacity is the absence of reliable, verifiable and timely information about suppliers, materials, emissions, labour conditions, origin, production practices and compliance status across the value chain.

It is not a soft governance problem. It creates information asymmetry. Information asymmetry increases perceived risk. Perceived risk affects financing terms, buyer confidence, audit intensity, contract conditions and market access.

The financial market does not need to prove that every supplier is non-compliant. It only needs to see that the company cannot prove control. That is enough to reprice risk.

Board Risk Signal

If the company cannot trace supply-chain risk, it cannot defend the margin, the contract or the cost of capital.

The CFO should treat opacity as a financial defect. It is measurable. It is contractually relevant. It is increasingly visible to lenders, buyers and regulators.

The Brown Penalty Is the Cost of Uncontrolled Risk

The “Brown Penalty” is the financial discount applied to companies, assets or supply chains perceived as more exposed to climate, environmental, social or governance risk. It can appear as higher financing cost, tighter covenants, lower valuation multiples, buyer discounts, insurer restrictions or reduced access to sustainability-linked finance.

The Brown Penalty is not always visible as a line item. It may appear inside the spread demanded by banks, the discount imposed by buyers, the valuation haircut applied by investors, or the operating cash trapped by delays and evidence rework.

Brown Penalty Channels

Cost of Debt

Lenders may increase spreads or covenants when supply-chain risks cannot be measured or monitored.

Cost of Equity

Investors may discount companies exposed to transition risk, regulatory uncertainty or weak governance evidence.

Commercial Pricing

Buyers can impose price reductions, audit costs, indemnities or preferred-supplier exclusion when evidence is weak.

The penalty is not ideological. It is a rational response to uncertainty.

How Opacity Moves Into WACC

Weighted Average Cost of Capital is the blended cost of debt and equity. Supply-chain opacity can affect both sides of the equation.

Debt providers price default risk, covenant risk, collateral risk and earnings volatility. Equity investors price future cash-flow uncertainty, regulatory exposure, litigation probability and margin stability. When the supply chain is opaque, each variable becomes harder to defend.

WACC Impact Formula Stack

WACC = Cost of Equity × Equity Weight + After-Tax Cost of Debt × Debt Weight

Opacity Premium = Risk Premium from Poor Traceability + Regulatory Uncertainty + Buyer Concentration Risk + Evidence Failure Risk

Adjusted Cost of Debt = Base Rate + Credit Spread + Opacity Premium + Covenant Risk Premium

Enterprise Value Drag = Expected Free Cash Flow / Adjusted WACC − Expected Free Cash Flow / Base WACC

The exact values must be calculated with internal company data. A responsible model requires current debt structure, credit spreads, equity valuation assumptions, EU revenue exposure, buyer concentration, supplier risk score, evidence maturity, contract exposure and cost of capital.

Climate and Nature Risks Are Now Banking Risks

European banking supervision now treats climate and nature-related risks as a prudential issue. The ECB’s 2026–2028 supervisory priorities state that banks should effectively assess and manage short-, medium- and long-term risks stemming from the climate and nature crises and remedy persistent weaknesses in risk management frameworks.

The practical consequence is direct. Banks are under pressure to understand how borrowers are exposed to climate transition risk, physical risk, nature risk and supply-chain vulnerabilities. Borrowers with weak data produce weaker credit files.

Credit Risk

Uncontrolled supply-chain exposure can increase perceived probability of disruption, margin loss or regulatory breach.

Collateral Risk

Inventory, receivables and production assets linked to vulnerable supply chains can lose reliability as collateral.

Transition Risk

Regulatory cost, carbon exposure, forced-labour risk, deforestation risk and product-data gaps can affect future cash flows.

The lender’s question will be simple: can the company prove that supply-chain risk is controlled?

Regulatory Pressure Is Converging on the Same Data Gap

Different EU regulations create different legal tests. The data gap is often the same: the company lacks verified primary evidence from suppliers and operations.

CSDDD demands risk-based due diligence across operations and value chains. CBAM requires embedded-emissions evidence for covered imported goods. EUDR requires origin, legality and deforestation-free evidence for covered commodities and products. The Digital Product Passport pushes product-level data into structured, machine-readable formats. CSRD and ESRS increase pressure for reliable disclosure and assurance-ready information.

Regulatory Data Convergence Map

CSDDD

Human rights and environmental due diligence evidence across value chains.

CBAM

Embedded-emissions data, product classification and carbon-cost exposure.

EUDR

Geolocation, legality, deforestation-free status and due diligence statement support.

The CFO should not fund separate data silos for each regulation. The correct architecture is one controlled evidence layer with regulation-specific outputs.

Due Diligence Must Be Measurable

The OECD due diligence framework is built around a risk-based process: identify, prevent, mitigate and account for actual and potential adverse impacts in operations, supply chains and business relationships. The OECD’s 2025 work on measuring due diligence uptake and impact reinforces the need for indicators that can assess firm-level outcomes.

This matters for finance. If due diligence is not measurable, it cannot support credit negotiation, buyer confidence or board-level risk control.

Supplier Coverage

Percentage of high-risk suppliers covered by verified evidence, not only self-declarations.

Corrective Action Closure

Rate of material corrective actions closed within defined deadlines and supported by evidence.

Revenue Protected

Share of EU revenue supported by audit-ready supply-chain compliance files.

A lender can price measurable control. It cannot price vague intent with the same confidence.

Supply-Chain Opacity Creates Contractual Exposure

European buyers will not wait for the CFO’s WACC model. They will use contracts.

Opacity is increasingly managed through supplier codes, audit rights, termination clauses, corrective action plans, disclosure obligations, indemnities and data-delivery deadlines. If the exporter accepts buyer-facing obligations without upstream control, it carries the liability without controlling the evidence source.

Contracts should define:

- supplier data obligations by risk category;

- emissions, origin, labour, environmental and product-data evidence requirements;

- audit rights over high-risk suppliers and sub-suppliers where commercially feasible;

- corrective action deadlines and verification standards;

- consequences for false, late or incomplete supplier data;

- buyer evidence deadlines and pass-through obligations;

- risk allocation for customs delays, regulatory blocks and buyer suspension;

- confidentiality controls for sensitive supplier and product data.

CFO Decision Rule

Do not accept buyer due diligence obligations unless upstream supplier contracts give the company enforceable rights to obtain, verify and update the evidence.

Opacity becomes expensive when obligations move downstream faster than evidence rights move upstream.

Opacity Reduces Sustainability-Linked Loan Credibility

Sustainability-Linked Loans require credible targets, measurable indicators and verification logic. A company with opaque supply chains may struggle to defend KPIs linked to emissions reduction, supplier due diligence, deforestation risk, human rights controls or product traceability.

This creates a financing paradox. The company may seek better credit terms through ESG performance, but the evidence needed to defend those terms sits upstream in supplier systems it does not control.

SLL Readiness Indicators

Primary Data Coverage

Share of critical suppliers providing verified data rather than unsupported self-declarations.

KPI Auditability

Evidence that sustainability-linked targets can be calculated, monitored and independently reviewed.

Risk Reduction Proof

Documented reduction in supplier risk, data gaps, adverse impacts or regulatory exposure.

The financing benefit exists only when performance can be proven.

The Financial Exposure Model

A CFO-grade opacity model should quantify the cost of not knowing. It must treat data gaps as expected financial loss, not as administrative backlog.

Supply-Chain Opacity Financial Formula Stack

Brown Penalty = Opacity Premium in Debt + Opacity Premium in Equity + Buyer Discount + Compliance Rework Cost

Regulatory Evidence Gap = Required Evidence Fields − Verified Evidence Available Before Buyer or Regulatory Deadline

Contract Revenue at Risk = Buyer Revenue × Probability of Evidence Failure × Suspension Period / Contract Period

Working-Capital Drag = Delayed Invoice Value × Evidence Delay Days × Cost of Capital / 365

The exact values require internal company data. A responsible model requires debt cost, equity assumptions, buyer revenue, supplier segmentation, regulatory scope, evidence gap rate, contract terms, average delay days and cost of capital.

The Villanova ESG Control Architecture

Villanova ESG operates exclusively at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains. For supply-chain opacity, the objective is not to create a sustainability dashboard. The objective is to build a financial defense system that converts upstream uncertainty into measurable, auditable and finance-grade control.

01 · Supplier Exposure Map

Map suppliers by revenue dependency, geography, product line, regulatory exposure, buyer pressure and materiality.

02 · Regulatory Data Matrix

Connect CSDDD, CBAM, EUDR, CSRD and DPP evidence requirements to supplier and product data fields.

03 · Primary Data File

Replace unsupported declarations with source evidence, verification logic, audit trail and update controls.

04 · Contract Shield

Align buyer obligations with upstream supplier evidence rights, audit rights, deadlines and risk allocation.

05 · WACC Risk Model

Quantify opacity premium, working-capital drag, buyer suspension risk, evidence rework cost and valuation sensitivity.

06 · SLL Readiness

Convert traceability, supplier due diligence and emissions evidence into lender-ready indicators for Sustainability-Linked Loans.

Decision Trigger for CFOs

The CFO should escalate supply-chain opacity when any of the following signals appear:

- critical suppliers are known only at Tier 1 level;

- supplier data depends on self-declarations without verification;

- EU buyers request evidence faster than internal teams can produce it;

- contracts impose due diligence obligations without upstream evidence rights;

- CBAM, EUDR, CSDDD, CSRD or DPP evidence is managed in separate silos;

- banks ask for transition-risk, emissions, deforestation or human rights evidence;

- the company cannot quantify the effect of opacity on WACC, margin or buyer retention;

- corrective action plans exist but are not tied to financial exposure;

- management cannot identify which supply-chain data supports Sustainability-Linked Loan KPIs;

- board reporting focuses on sustainability activity rather than cash-flow protection.

These are not operational imperfections. They are financing, market-access and valuation risk indicators.

Regulatory Source Trail

This dossier relies on official regulatory and supervisory sources verified for supply-chain due diligence, climate and nature risk supervision, sustainability-linked finance relevance and responsible business conduct measurement:

- OECD — Due Diligence for Responsible Business Conduct

- European Commission — Corporate Sustainability Due Diligence

- ECB Banking Supervision — Supervisory Priorities 2026–2028

- European Central Bank — Climate and Nature Risks in ECB Processes

- OECD — Measuring the Uptake and Impact of Due Diligence for Responsible Supply Chains

- World Bank Group — Climate Change and Development Finance

Closing CTA · WACC and Supply-Chain Risk Defense

If lenders and buyers cannot see through your supply chain, they will price the uncertainty into your cost of capital and contracts.

Villanova ESG structures the regulatory shield required to convert supply-chain opacity into auditable evidence, reduce perceived risk, protect cash flow and strengthen Sustainability-Linked Loan readiness.

For a board-level supply-chain opacity and WACC exposure review, contact contact@villanovaesg.com.