Board Duties Under CSDDD: Fiduciary Accountability for Supply-Chain Compliance

Executive Dossier · CSDDD Board Duties

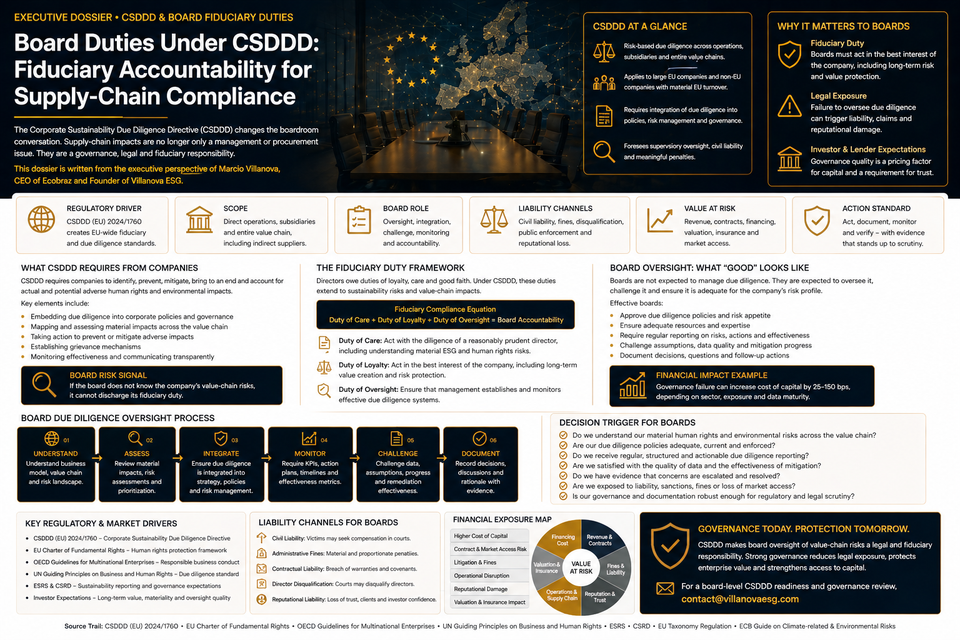

CSDDD board exposure is not an automatic EU-wide fiduciary-liability rule. It is an oversight, evidence and governance risk that can move through national law, buyer contracts, lender scrutiny and director accountability.

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. The analysis treats board duties under CSDDD as a cash-flow and governance control issue. The board question is direct: can directors prove that supply-chain risks are identified, escalated, challenged, documented and connected to financial exposure before regulators, buyers, lenders or claimants test the file?

Legal Basis

Directive (EU) 2024/1760

Omnibus Position

EU civil liability harmonisation removed

Compliance Date

26 July 2029

Board Exposure

Oversight failure, contract risk, lender scrutiny

The Board Risk Must Be Framed Correctly

CSDDD does not create a simple automatic EU-wide director liability rule for every supply-chain failure. That interpretation is legally unsafe. The current Omnibus position removes the EU-harmonised civil liability regime and leaves civil liability to national legal systems.

This does not eliminate board exposure. It changes the channel. Directors remain exposed through governance obligations, national company law, fiduciary standards, reporting controls, buyer commitments, lender due diligence, D&O insurance review and failure to supervise material risks.

The board issue is not theoretical. If management cannot prove how human rights and environmental risks were identified, prioritised, mitigated and monitored, the board’s oversight quality becomes part of the financial risk file.

Board Risk Signal

CSDDD board exposure is not only about sanctions. It is about whether directors can prove informed oversight over value-chain risk before cash flow is disrupted.

The CFO and the board should treat CSDDD as a governance evidence problem. A policy is not enough. The company needs a record of risk-based decisions.

What CSDDD Still Requires From Corporate Governance

The CSDDD establishes a corporate due diligence duty. The core duty is to identify and address actual and potential adverse human rights and environmental impacts in the company’s own operations, subsidiaries and value chains.

Even after simplification, governance remains central. Due diligence cannot operate without board-level oversight, resource allocation, risk appetite, internal controls and escalation procedures.

01 · Risk Identification

Management must identify actual and potential adverse impacts across operations, subsidiaries and relevant value-chain relationships.

02 · Risk Response

The company must prevent, mitigate, bring to an end or minimise impacts through documented measures where required.

03 · Board Oversight

The board must be able to challenge management, demand evidence and connect material value-chain risk to financial exposure.

The board does not need to run the due diligence system. It must prove that the system is governed, resourced, challenged and monitored.

The Climate Transition Plan Change Alters the Board Agenda

The Omnibus simplification removes the CSDDD obligation for companies to adopt a transition plan for climate change mitigation. This is a material regulatory change and must be reflected in board materials.

That does not make climate governance irrelevant. Transition-plan expectations may still appear through CSRD reporting, lender due diligence, investor scrutiny, voluntary commitments, buyer requirements and sector-specific financing expectations.

Climate Governance After Omnibus

CSDDD Requirement

The specific CSDDD transition-plan obligation has been removed under the Omnibus position.

Market Expectation

Banks, investors and buyers may still require credible transition evidence through separate frameworks.

Board Control

The board should distinguish legal obligation from financing expectation and disclosure risk.

Precision protects the board. Overstating a removed CSDDD obligation creates legal noise. Ignoring remaining market pressure creates financial risk.

The Fiduciary Issue Is Oversight, Not Slogan Governance

Fiduciary accountability depends on national law, corporate structure and facts. The defensible position is not to claim that CSDDD automatically rewrites director duties across all Member States. The defensible position is to show that directors exercised informed oversight over material risk.

For boards, the practical question is evidence: what did the board know, when did it know it, what did it ask management to do, and how did it monitor execution?

Board Oversight Formula Stack

Board Accountability Strength = Risk Visibility × Challenge Quality × Resource Allocation × Documentation Depth × Follow-Up Discipline

Oversight Failure Risk = Material Supply-Chain Exposure × Evidence Gap × Board Inaction Probability

Governance Defense Value = Board Minutes + Risk Reports + Escalation Logs + Mitigation Decisions + Follow-Up Evidence

Cash-Flow Exposure = At-Risk EU Revenue × Probability of Buyer or Regulatory Action × Disruption Period / Contract Period

The exact values require internal company data. A responsible model requires EU customer revenue, supplier risk concentration, board reporting cadence, unresolved adverse impacts, buyer contract terms, evidence gap rate, insurance coverage and cost of capital.

What “Good Board Oversight” Looks Like

A board is not expected to audit every supplier personally. It is expected to ensure that management has a credible system and that material risks are visible at the right level.

Effective board oversight should include:

- approval of due diligence governance and risk appetite;

- regular review of material human rights and environmental risk maps;

- clear escalation thresholds for high-risk suppliers, sectors and geographies;

- review of corrective action plans and unresolved adverse impacts;

- challenge of data quality, supplier response rates and verification gaps;

- oversight of buyer evidence requests and contractual risk allocation;

- integration of due diligence risk into financing, insurance and M&A discussions;

- formal documentation of board questions, decisions, assumptions and follow-up actions.

CFO Decision Rule

If the board packet does not quantify supply-chain risk in financial terms, directors are supervising a compliance narrative, not a cash-flow exposure.

Governance must be visible in the record. Unrecorded oversight is weak defense.

Board Minutes Are a Liability Shield Only When They Show Substance

Board minutes should not be decorative. They should evidence that directors received risk information, challenged assumptions, demanded corrective action and monitored unresolved issues.

A strong board record should show:

- which material supply-chain risks were presented;

- which suppliers, regions or commodities were escalated;

- which data gaps were accepted temporarily and why;

- which mitigation plans were approved;

- which budgets or resources were allocated;

- which unresolved risks were carried forward;

- which buyer or lender requests were discussed;

- which follow-up actions were assigned to management.

The board minutes should not overstate control. They should accurately document decisions, limitations and remediation commitments. That is stronger than polished language without evidence.

The Contract Channel Is Where Board Risk Becomes Commercial Risk

Large European buyers will push due diligence obligations into supplier contracts. Even companies outside direct CSDDD scope may face pass-through obligations, audit clauses, data-delivery duties and termination rights.

Boards should require management to identify whether buyer commitments are matched by upstream supplier rights. If not, the company accepts downstream liability without upstream control.

Contract Governance Map

Buyer Obligations

Audit rights, supplier codes, evidence deadlines, corrective action plans and termination triggers.

Supplier Rights

Origin evidence, labour records, environmental data, audit access, remediation duties and indemnity logic.

Board Question

Does the company have enforceable upstream control over every material downstream commitment?

Contract asymmetry is a board issue because it can convert compliance pressure into margin loss, claims exposure and customer disruption.

Lender and D&O Insurance Scrutiny Will Increase

Even when CSDDD liability is tested under national regimes, lenders and insurers will examine governance quality. They will ask whether directors knew about material supply-chain exposure and whether management had a credible system to address it.

D&O insurers may focus on board process, disclosure accuracy, previous incidents, unresolved supplier risks, controls over public statements and litigation probability. Lenders may focus on buyer concentration, regulatory disruption, transition risk and covenant sensitivity.

Lender Review

Credit teams may examine whether value-chain risk can affect revenue, margin, working capital and covenant strength.

Insurance Review

D&O underwriters may examine whether the board had adequate information, process and documentation.

Investor Review

Investors may treat governance quality as a signal for resilience, valuation and long-term cash-flow protection.

Board oversight is becoming a financing signal. Weak governance increases perceived risk.

Board Oversight and Sustainability-Linked Finance

Sustainability-Linked Loans require credible governance over KPIs and performance targets. If the company uses supplier due diligence, human rights risk, emissions coverage or traceability as financing indicators, the board must understand the evidence system behind those metrics.

Board-level governance should cover:

- why each KPI is financially material;

- which business unit owns the data;

- which suppliers or products are included;

- how evidence is verified;

- how data gaps are corrected;

- how underperformance affects financing costs;

- how management reports progress to the board;

- how external review or assurance is handled.

A sustainability-linked financing structure without board-level governance becomes a covenant risk.

SLL Governance Formula Stack

SLL Governance Strength = KPI Materiality × Data Control × Board Oversight × External Review Readiness

Covenant Failure Risk = KPI Ambition × Data Uncertainty × Operational Execution Gap

Financing Defense Value = Verified Performance Evidence + Board Monitoring + Corrective Action Record

The exact values require internal financing data. A responsible model needs loan terms, KPI definitions, margin ratchet structure, evidence maturity, external review requirements, supplier coverage and board reporting cadence.

The Villanova ESG Control Architecture

Villanova ESG operates exclusively at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains. For CSDDD board duties, the objective is not to create a governance narrative. The objective is to build a board-level evidence architecture that proves oversight, protects cash flow and supports financing credibility.

01 · Board Risk Map

Translate CSDDD exposure into board-level risk categories: revenue, litigation, sanctions, contracts, financing and reputation.

02 · Oversight Protocol

Define board cadence, escalation triggers, risk appetite, management reporting and documentation standards.

03 · Evidence Dashboard

Track supplier risk, corrective actions, evidence gaps, buyer demands, unresolved impacts and financial exposure.

04 · Contract Shield

Align buyer obligations with upstream supplier rights, audit clauses, data duties, remediation rights and indemnity logic.

05 · CFO Risk Model

Quantify buyer suspension, litigation exposure, working-capital drag, insurance implications and financing sensitivity.

06 · Board Evidence File

Prepare defensible records of board review, challenge, decisions, assumptions, limitations and follow-up actions.

Decision Trigger for CFOs and Boards

The board should escalate CSDDD governance exposure when any of the following signals appear:

- management cannot identify material human rights and environmental risks across the value chain;

- board packs discuss compliance activity but not revenue, contract or financing exposure;

- supplier due diligence is limited to generic questionnaires without verification;

- buyer contracts contain due diligence obligations not mirrored in upstream supplier contracts;

- corrective action plans are not tracked with owners, deadlines and evidence of closure;

- board minutes do not record challenge, assumptions, limitations and follow-up;

- D&O insurance renewal requests more information on ESG, supply-chain or human rights risk;

- lenders ask for due diligence evidence, transition-risk information or supplier-risk controls;

- management cannot quantify the cash-flow impact of buyer suspension, regulatory friction or litigation exposure;

- the company assumes Omnibus simplification removes the need for board-level value-chain oversight.

These are not governance formalities. They are liability, financing and market-access indicators.

Regulatory Source Trail

This dossier relies on official EU legal and institutional materials verified for the CSDDD, Omnibus simplification, due diligence duty, civil liability changes, transition-plan removal and implementation timing:

- European Commission — Corporate Sustainability Due Diligence

- Council of the EU — Simplification of Sustainability Reporting and Due Diligence Requirements

- Council of the EU — Provisional Agreement on Sustainability Simplification

- European Parliament — Simplified Sustainability Reporting and Due Diligence Rules

- EUR-Lex — Directive (EU) 2024/1760

- EUR-Lex — Accounting Directive 2013/34/EU

Closing CTA · Board-Level CSDDD Defense

If the board cannot prove oversight over value-chain risk, CSDDD simplification will not protect the company from buyer pressure, lender scrutiny or governance claims.

Villanova ESG structures the board-level evidence architecture required to protect European market access, defend cash flow, reduce oversight risk and convert supply-chain compliance into finance-grade governance proof.

For a confidential board-level CSDDD governance review, contact contact@villanovaesg.com.