Scope 3 Emissions Baseline Mapping: Unlocking Access to Green Finance

Executive Dossier · Scope 3 Baseline & Green Finance

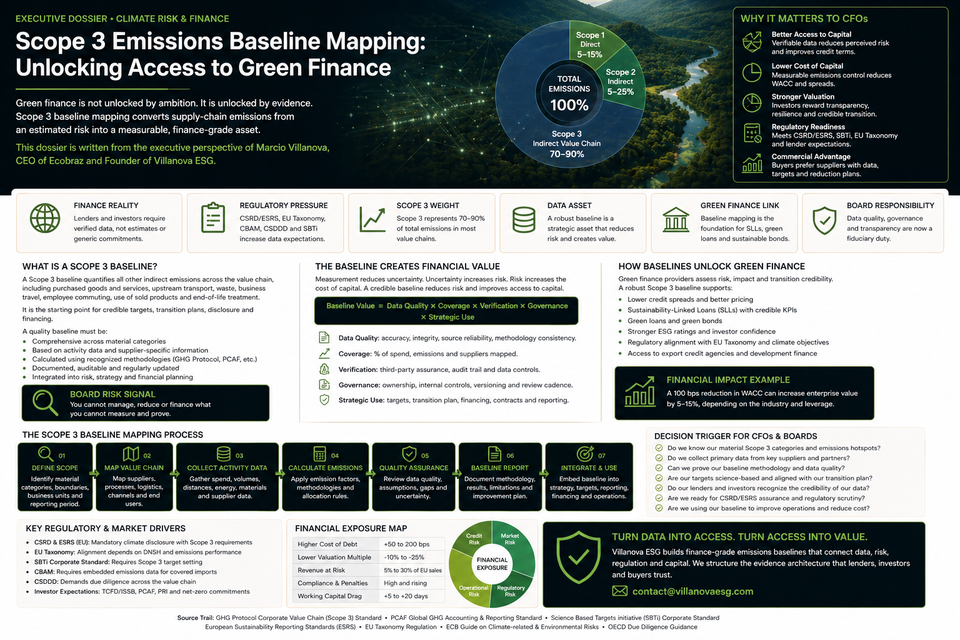

Green finance is not unlocked by ambition. It is unlocked by evidence. A Scope 3 baseline converts supplier emissions from an uncontrolled estimate into a finance-grade risk asset.

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. The analysis treats Scope 3 baseline mapping as a capital-access and cash-flow protection issue. The board question is direct: can the company prove its value-chain emissions exposure with enough accuracy, governance and auditability to support lender confidence, buyer scrutiny and Sustainability-Linked Loan negotiation?

Accounting Standard

GHG Protocol Scope 3 Standard

Disclosure Pressure

IFRS S2 · CSRD · ESRS · Buyer reporting

Finance Link

Sustainability-Linked Loans

Financial Exposure

WACC, covenants, buyer trust, margin defense

Scope 3 Is the Emissions Exposure Lenders Cannot Ignore

Scope 3 emissions are indirect emissions across a company’s value chain. They include upstream and downstream sources such as purchased goods and services, capital goods, transportation, waste, business travel, employee commuting, use of sold products, end-of-life treatment, franchises and investments.

For many companies, Scope 3 is the largest emissions exposure. The exact percentage cannot be responsibly stated without company-specific data, sector boundaries and accounting methodology. A CFO-grade baseline must therefore start with materiality, activity data and supplier-specific evidence, not generic benchmarks.

The financial point is clear. If the company cannot measure its value-chain emissions, it cannot credibly reduce them, finance them, disclose them or defend them before buyers and lenders.

Board Risk Signal

A Scope 3 baseline is not an emissions inventory. It is the first financial control layer for climate-linked credit, buyer confidence and transition-risk defense.

The board should treat Scope 3 data as a risk-pricing input. Poor data increases uncertainty. Uncertainty increases perceived risk. Perceived risk affects financing terms, buyer retention and strategic valuation.

The Baseline Is the Difference Between Claim and Credit Evidence

A Scope 3 baseline quantifies value-chain emissions for a defined reporting period using a documented methodology, activity data, emission factors, supplier information and quality controls. It creates the reference point against which future reductions, targets, financing KPIs and transition plans are measured.

Without a baseline, the company cannot prove whether its emissions performance is improving. It can only claim directionally that it is acting. That is too weak for lender due diligence.

01 · Baseline Year

Define the reporting period, organisational boundary, operational boundary and recalculation policy.

02 · Category Boundary

Assess all 15 Scope 3 categories and document exclusions, materiality judgments and calculation logic.

03 · Finance Link

Convert baseline data into lender-readable indicators for transition planning and Sustainability-Linked Loan structuring.

The baseline is not a static report. It is the control point from which the company manages reduction pathways, supplier engagement, disclosure integrity and financing credibility.

IFRS S2 Raises the Disclosure Bar

IFRS S2 requires entities to disclose information about Scope 3 greenhouse gas emissions so users of general purpose financial reports can understand the sources of those emissions. The standard requires the entity to consider its entire value chain, both upstream and downstream, and consider the 15 Scope 3 categories described in the GHG Protocol Corporate Value Chain Standard.

This changes the finance discussion. Scope 3 is no longer only a sustainability team issue. It is becoming part of investor-grade climate disclosure, risk management and capital-market communication.

Disclosure-Grade Scope 3 Baseline Requirements

Full Value Chain

The baseline must evaluate upstream and downstream activities, not only direct operations.

15 Categories

Each Scope 3 category must be assessed for relevance, data availability, calculation method and materiality.

Source Transparency

Users of financial reports need to understand where emissions originate and how they were measured.

The CFO should assume that weak Scope 3 data will become visible in financial reporting, buyer audits and lender review.

Green Finance Requires Baseline Integrity

Sustainability-Linked Loans depend on credible KPIs and Sustainability Performance Targets. If the borrower uses Scope 3 emissions as a KPI, the baseline must be robust enough to support measurement, monitoring, external review and future target testing.

A lender will not price ambition. It will price evidence. The baseline must therefore be auditable, repeatable and connected to operational levers.

Scope 3 Green Finance Formula Stack

Baseline Credibility = Data Quality × Category Coverage × Supplier-Specific Evidence × Verification Readiness × Governance Control

SLL KPI Bankability = Materiality × Measurability × Ambition × External Review Capacity × Reporting Frequency

Financing Risk Reduction = Opacity Premium Before Baseline − Opacity Premium After Verified Baseline

Transition Plan Credibility = Baseline Integrity + Reduction Pathway + Supplier Engagement + Capex Alignment + Governance Oversight

The exact values must be calculated with internal company data. A responsible model requires purchase volumes, supplier spend, transport distances, emission factors, supplier-specific emissions, product mix, financing terms, current credit spread, lender KPI requirements and external assurance costs.

The 15 Categories Must Be Treated as a Risk Map

The GHG Protocol Scope 3 framework contains 15 categories. A CFO should not treat them as a checklist. They are a risk map for cost, procurement, logistics, customer use, product design, end-of-life exposure and financed emissions.

The baseline must identify which categories are material and which categories require deeper data collection. Not every category will have the same financial relevance. The company must document the logic.

Scope 3 Category Risk Map

Procurement Exposure

Purchased goods and services, capital goods and upstream transport often drive supplier engagement and procurement leverage.

Logistics Exposure

Transportation, distribution, business travel and employee commuting connect emissions data to cost control and routing decisions.

Revenue Exposure

Use of sold products, processing, end-of-life treatment and downstream distribution can affect buyer pressure and product strategy.

Materiality must be defended. Excluding a category without evidence weakens disclosure credibility and financing negotiations.

Supplier-Specific Data Changes the Credit Conversation

Spend-based estimates can help build an initial baseline. They are not enough for high-confidence finance. As the company matures, the baseline must move toward activity data, supplier-specific emissions and verified source evidence where material.

This is where Scope 3 becomes a commercial control. Supplier engagement is no longer only a procurement exercise. It is part of capital strategy.

Low-Maturity Data

Spend-based estimates provide directional exposure but carry high uncertainty and weak supplier accountability.

Medium-Maturity Data

Activity data improves calculation quality by connecting emissions to volumes, distances, materials and operating parameters.

Finance-Grade Data

Supplier-specific and verified data improves credibility for targets, lender review, buyer audits and performance-linked financing.

The transition from estimate to evidence is where financing value is created.

Scope 3 Baselines Must Connect to Contracts

The baseline will fail if suppliers have no obligation to provide the required data. Procurement contracts must align with emissions accounting and financing objectives.

Supplier contracts should define:

- which emissions data must be provided;

- whether data must be spend-based, activity-based or supplier-specific;

- which methodology and emission factors are acceptable;

- which source documents must support the data;

- how frequently suppliers must update emissions information;

- whether third-party verification is required for material suppliers;

- what happens if data is false, late or incomplete;

- how emissions reduction initiatives are documented and measured;

- which data can be used for disclosure, buyer reporting and lender review.

CFO Decision Rule

Do not build a Scope 3 financing strategy unless supplier contracts give the company enforceable rights to obtain, verify and update emissions data.

The company cannot finance a reduction pathway it cannot evidence.

SBTi and Target Credibility

The SBTi Corporate Net-Zero Standard allows companies to set Scope 3 targets through different boundary structures, including category-specific targets or a single target covering relevant Scope 3 categories. This creates flexibility, but it also increases the need for clear target logic.

A target that does not connect to baseline quality, supplier coverage, reduction levers and financing metrics will not carry credit weight.

Target Credibility Map

Boundary Integrity

The target must state which categories, emissions sources and entities are included.

Reduction Logic

The company must identify how emissions will fall through procurement, logistics, design, supplier engagement or customer use changes.

Finance Relevance

Targets should support credit risk reduction, buyer retention, margin resilience and transition-plan credibility.

The CFO should reject targets that are ambitious but financially disconnected.

Baseline Governance Is the Hidden Financing Requirement

Scope 3 data crosses procurement, logistics, finance, sustainability, legal, IT, product teams and suppliers. Without governance, the baseline becomes a spreadsheet exercise with weak audit value.

The governance file should define ownership, methodology, data sources, assumptions, approval workflow, recalculation triggers, quality controls, assurance readiness and board oversight.

Baseline Governance Formula

Baseline Governance Strength = Methodology Discipline + Data Ownership + Supplier Controls + Internal Review + External Assurance Readiness

Data Quality Score = Source Reliability + Completeness + Accuracy + Timeliness + Verification Level

Disclosure Risk = Material Emissions Exposure × Data Uncertainty × Assurance Gap

The exact scoring model must be built with internal company data. It requires category-level data maturity, supplier response rate, evidence availability, audit findings, recalculation events and reporting controls.

Scope 3 and EU Market Access

Scope 3 baseline mapping also supports EU regulatory defense. It does not replace CBAM, EUDR, CSDDD, CSRD or DPP evidence. It strengthens the evidence architecture behind them.

CBAM may require product-level embedded-emissions data for covered goods. CSDDD increases pressure for value-chain risk control. CSRD and ESRS increase disclosure and assurance expectations. The Digital Product Passport is pushing product-level data into structured formats. The Scope 3 baseline becomes the connective layer between climate data, supplier evidence and finance.

CBAM Link

Supplier and production data help reduce embedded-emissions uncertainty for covered goods.

CSDDD Link

Supplier mapping and value-chain evidence support broader risk-based due diligence controls.

CSRD Link

Scope 3 data quality supports climate disclosure, assurance readiness and financial-reporting credibility.

Scope 3 is not isolated climate accounting. It is part of the EU compliance and capital-access stack.

The Villanova ESG Control Architecture

Villanova ESG operates exclusively at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains. For Scope 3 baseline mapping, the objective is not to produce an emissions number. The objective is to build a finance-grade evidence system that supports credit negotiations, buyer confidence, EU compliance and board-level transition governance.

01 · Category Materiality Map

Assess all 15 Scope 3 categories by spend, emissions relevance, buyer exposure, regulatory pressure and financing relevance.

02 · Supplier Data Architecture

Collect activity data, supplier-specific emissions, source evidence, update frequency and quality-control metadata.

03 · Calculation Engine

Apply recognised methodologies, emission factors, allocation rules and recalculation policies with documented assumptions.

04 · Contract Shield

Insert supplier data obligations, verification rights, update duties, correction mechanisms and disclosure permissions.

05 · CFO Finance Model

Translate Scope 3 data into WACC sensitivity, SLL KPI readiness, buyer exposure, capex planning and transition-risk defense.

06 · Lender Evidence Pack

Prepare finance-grade baseline documentation for banks, investors, external reviewers, buyers and assurance providers.

Decision Trigger for CFOs

The CFO should escalate Scope 3 baseline mapping when any of the following signals appear:

- Scope 3 emissions are material but still based mainly on spend-based estimates;

- the company cannot identify which Scope 3 categories drive the largest financial exposure;

- supplier contracts do not require emissions data, source evidence or update rights;

- buyers request emissions evidence faster than internal teams can validate it;

- banks request transition-risk evidence for credit review or Sustainability-Linked Loan discussions;

- climate targets exist but are not connected to supplier-specific reduction levers;

- the baseline has no documented recalculation policy;

- data ownership is fragmented across sustainability, procurement, finance and operations;

- Scope 3 disclosure is prepared separately from CBAM, CSDDD, CSRD and product-data controls;

- management cannot quantify how emissions data quality affects WACC, covenant strength or buyer retention.

These are not reporting weaknesses. They are financing, market-access and capital-cost indicators.

Regulatory Source Trail

This dossier relies on official technical and market references verified for Scope 3 accounting, climate-related disclosure, target-setting and sustainability-linked finance:

- GHG Protocol — Corporate Value Chain Scope 3 Standard

- GHG Protocol — Technical Guidance for Calculating Scope 3 Emissions

- IFRS Foundation — IFRS S2 Climate-related Disclosures

- IFRS Foundation — GHG Emissions Disclosure Requirements Applying IFRS S2

- Science Based Targets initiative — Corporate Net-Zero Standard

- Science Based Targets initiative — Corporate Net-Zero Standard V1.3.1

- Loan Market Association — Sustainable Lending Resources and SLLP Guidance

Closing CTA · Scope 3 Finance Defense

If your Scope 3 baseline cannot survive lender review, your green finance strategy is exposed before negotiation begins.

Villanova ESG structures finance-grade Scope 3 baselines that connect supplier data, EU regulatory risk, transition planning, buyer confidence and Sustainability-Linked Loan readiness.

For a board-level Scope 3 baseline and green finance readiness review, contact contact@villanovaesg.com.