WEEE Open-Scope: Financial Assurance and Producer Responsibility Exposure

Executive Dossier · WEEE Open-Scope Exposure

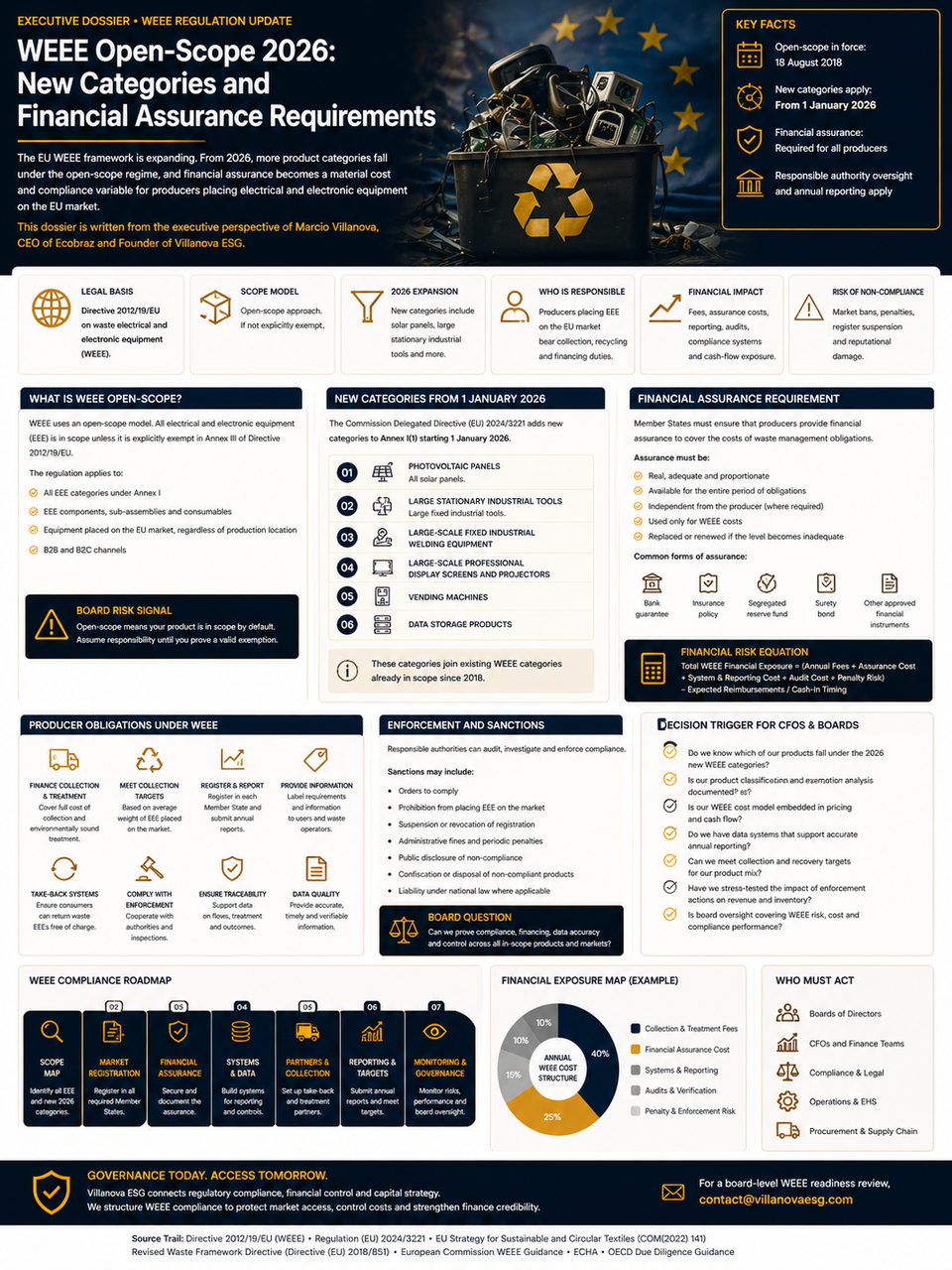

WEEE open scope is not new in 2026. It has applied since 15 August 2018. The current financial risk is accumulated misclassification, producer registration failure, reporting gaps and unfunded end-of-life obligations across EU Member States.

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. The analysis treats WEEE compliance as a cash-flow and market-access control issue. The board question is direct: can the company prove which electrical and electronic products are in scope, where they are placed on the EU market, which entity is the producer, and how collection, treatment, reporting and financial assurance obligations are funded?

Legal Basis

Directive 2012/19/EU

Open Scope

In force since 15 August 2018

Market Data

14.4m tonnes EEE placed on market

Financial Exposure

Fees, assurance, reporting, take-back, enforcement

The First Correction: Open Scope Is Already in Force

The WEEE open-scope regime is frequently misunderstood. It is not a new 2026 regime. Since 15 August 2018, electrical and electronic equipment is generally within the WEEE Directive’s open-scope structure unless a valid exclusion applies.

The commercial risk today is not that open scope suddenly begins. The risk is that companies have continued selling products into EU Member States under outdated assumptions, incomplete category mapping or weak producer-registration controls.

For CFOs, that creates accumulated exposure. The liability may sit in unpaid national fees, missing reports, lack of financial assurance, unsupported category decisions, distributor friction, blocked marketplace access or enforcement by national authorities.

Board Risk Signal

If the company cannot prove why an electrical or electronic product is out of scope, the financially safer assumption is that the product must be tested for WEEE obligations.

The board should not approve a WEEE position based on product intuition. Scope must be documented product by product, market by market and legal entity by legal entity.

WEEE Is a Producer-Responsibility Cost System

The WEEE Directive is designed to prevent and reduce the adverse impacts of waste electrical and electronic equipment. It requires separate collection, proper treatment, recovery and recycling. It also supports resource efficiency and recovery of secondary raw materials.

For the CFO, the practical meaning is direct. A product placed on the EU market can create cost obligations beyond manufacturing, logistics and sales. The producer may need to register, report volumes, finance collection and treatment, provide information, join a compliance scheme and maintain evidence of compliance.

01 · Product Scope

Determine whether the product is electrical or electronic equipment and whether an exclusion applies.

02 · Producer Status

Identify which entity is treated as producer in each Member State and sales channel.

03 · Financial Duty

Model registration, scheme fees, reporting, take-back, treatment, recovery and financial guarantee exposure.

The financial control point is not only whether the product is recyclable. It is whether the company has priced the legal cost of placing that product on the EU market.

The EU Data Shows Why Enforcement Pressure Will Continue

The Commission reports that 14.4 million tonnes of electrical and electronic equipment were placed on the market, while 5 million tonnes of e-waste were collected in 2022. That collection gap is a policy pressure signal.

WEEE is also tied to critical raw materials. Modern electronics contain valuable and strategic materials that can be recycled and reused. This makes WEEE enforcement relevant not only to environmental policy, but also to industrial resilience and resource security.

WEEE Policy Pressure Map

Waste Growth

Electrical and electronic waste is increasing rapidly, creating enforcement pressure on producers and national systems.

Resource Recovery

Electronics contain valuable and critical materials that the EU wants to recover and reuse.

Illegal Shipment Control

The WEEE framework supports efforts to prevent illegal disguise and export of waste electrical equipment.

The CFO should assume the enforcement direction is toward better data, stronger producer accountability and less tolerance for unsupported classifications.

The Financial Assurance Question

WEEE financial assurance is not a cosmetic compliance item. It exists to ensure that the cost of future waste management is covered. In practice, assurance mechanics vary by Member State, product type, B2C or B2B status, compliance scheme model and national implementation.

That variability creates a finance problem. A single product portfolio can generate different producer duties, fee structures, reporting cadences and financial guarantee requirements across EU markets.

WEEE Financial Exposure Formula Stack

Total WEEE Cost Exposure = Registration Fees + Compliance Scheme Fees + Reporting Cost + Financial Assurance Cost + Take-Back Cost + Treatment and Recovery Cost

Back-Compliance Exposure = Historical Units Placed on Market × Applicable Fee Rate × Non-Compliance Period + Penalties + Remediation Cost

Market Access Exposure = EU Product Revenue × Probability of Registration or Marketplace Block × Disruption Period / Contract Period

Working-Capital Drag = Blocked Sales or Inventory Value × Evidence Delay Days × Cost of Capital / 365

The exact values require internal company data. A responsible model needs product categories, Member States served, units placed on market, product weight, B2C/B2B status, producer entity, sales channel, compliance scheme fees, assurance mechanics, historical reporting gaps and cost of capital.

Product Classification Is the First Control Failure

WEEE exposure usually starts with classification. A product that looks minor may still be electrical or electronic equipment. Components, accessories, embedded electronics, connected devices, chargers, tools, displays, sensors and professional equipment can all require review.

Open scope means the company must document exclusions carefully. Silence is not evidence. A product master file must carry the classification rationale, category, Member State treatment, producer responsibility and reporting logic.

Product Data

Electrical function, voltage, battery status, embedded components, accessories and product weight.

Scope Rationale

Category decision, exclusion analysis, B2C/B2B logic, country-specific interpretation and documentation owner.

Reporting File

Units, weights, market placement dates, national registration numbers, scheme reports and evidence retention.

A CFO should not approve EU sales expansion before the product master file can support WEEE classification and reporting.

Marketplaces and Distributors Can Become Compliance Gatekeepers

Even where national authorities have not yet acted, marketplaces, distributors and large buyers may require WEEE registration evidence. This can turn a regulatory gap into an immediate sales block.

The commercial pathway is predictable. The company lists or ships a product. The buyer or platform asks for national registration. The internal team discovers that producer status, category mapping or representative appointment is incomplete. Sales pause while finance funds emergency compliance work.

CFO Decision Rule

Do not launch EEE products into an EU market until the company can prove producer registration, category logic, reporting process and financial responsibility for that Member State.

WEEE failures often appear first as commercial friction, not regulatory letters.

WEEE Is Fragmented by Member State

The WEEE Directive is an EU framework, but implementation and enforcement are handled nationally. That creates fragmentation. Companies must manage national registers, national compliance schemes, national reporting deadlines, authorised representative requirements and local fee structures.

This fragmentation is where finance teams often lose control. A single EU revenue number hides many local obligations.

Member State Exposure Map

Registration

Identify which entity must register and whether an authorised representative is required.

Reporting

Track reporting cadence, product weights, categories, B2B/B2C splits and evidence retention.

Cost Recovery

Model compliance scheme costs, treatment fees, take-back liabilities and financial assurance mechanics.

The board should demand a country-level WEEE matrix. One EU-wide answer is not enough.

Historical Exposure Requires Back-Compliance Analysis

If the company has sold electrical or electronic equipment into the EU without clear WEEE controls, the CFO should assess historical exposure. The risk is not only future compliance. It is whether past sales created unfunded producer obligations.

Back-compliance analysis should cover:

- products placed on EU markets since 15 August 2018;

- Member States where products were sold;

- product weights and units placed on the market;

- producer status by channel and legal entity;

- registration gaps;

- missed reports;

- unpaid scheme fees;

- financial assurance gaps;

- take-back obligations;

- marketplace or distributor requests already received.

Back-compliance is a finance exercise. It must quantify exposure before authorities, buyers or platforms do it for the company.

WEEE and Sustainability-Linked Finance

WEEE compliance can support finance when it proves producer responsibility control, circular-economy performance and resource-efficiency discipline. Lenders and investors do not finance generic recycling claims. They finance measurable systems that reduce regulatory and operating risk.

Relevant finance-grade indicators may include:

- percentage of EU EEE revenue covered by WEEE registration evidence;

- percentage of in-scope products with documented category classification;

- reporting accuracy rate by Member State;

- collection and treatment compliance coverage;

- financial assurance coverage for applicable products;

- reduction in historical back-compliance gaps;

- share of product portfolio designed for easier treatment, reuse, recovery or recycling;

- percentage of distributor and marketplace requests answered within deadline.

The financing value is not created by the presence of a recycling symbol. It is created by evidence that the company controls end-of-life obligations and avoids unfunded liabilities.

WEEE Finance Readiness Map

Market Access Control

National registration and reporting evidence reduce sales-block risk from authorities, distributors and marketplaces.

Cash-Flow Control

Accurate WEEE cost modeling prevents unexpected scheme fees, assurance costs and back-compliance exposure.

Circular Economy Evidence

Verified treatment, recovery and recycling data support lender review and sustainability-linked finance indicators.

Exporter Scenario Planning

WEEE exposure should be modeled through product, country and channel scenarios. A company selling the same device through distributors, online platforms and direct B2B contracts may have different registration and reporting obligations depending on the market structure.

WEEE Risk Scenarios

Base Case

All in-scope products are classified, registered, reported and covered by financial responsibility arrangements in each Member State.

Stress Case

A marketplace requests national WEEE registration evidence for a high-revenue product and sales pause until the file is corrected.

Severe Case

Historical sales reveal missed registration, unpaid fees and reporting gaps across multiple Member States, triggering back-compliance and enforcement cost.

The scenario output should include affected EU revenue, country-level fee exposure, back-compliance cost, registration delay, marketplace disruption, financial assurance cost and working-capital drag.

The Villanova ESG Control Architecture

Villanova ESG operates exclusively at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains. For WEEE, the objective is not to create a recycling narrative. The objective is to build a producer-responsibility control system that protects EU market access, cash flow and financing credibility.

01 · Product Scope Map

Map all electrical and electronic products, accessories, components, categories, exclusions and market channels.

02 · Member State Matrix

Identify registration, authorised representative, scheme participation, reporting and assurance requirements by country.

03 · Financial Assurance File

Document funding model, guarantee mechanics, treatment-cost assumptions, scheme fees and take-back obligations.

04 · Reporting Control Layer

Connect product weights, units placed on market, categories, countries, sales channels and reporting deadlines.

05 · CFO Risk Model

Quantify WEEE fees, assurance cost, back-compliance exposure, sales-block risk and working-capital drag.

06 · Finance Readiness

Convert producer-responsibility controls into lender-readable indicators for circular economy, risk reduction and SLL readiness.

Decision Trigger for CFOs

The CFO should escalate WEEE exposure when any of the following signals appear:

- the company sells electrical or electronic products into the EU without a product-level WEEE scope file;

- classification relies on assumptions rather than documented category and exclusion analysis;

- EU sales occur through marketplaces or distributors that may request national registration evidence;

- product weights and units placed on market are not linked to reporting systems;

- Member State registration status is unclear;

- financial assurance or take-back obligations are not priced into product margins;

- historical EU sales since 15 August 2018 have not been assessed for back-compliance;

- scheme fees and reporting obligations are managed outside finance controls;

- the company cannot quantify compliance cost by country, product line and sales channel;

- lenders or buyers request circular economy or producer-responsibility evidence.

These are not recycling issues. They are market-access, margin and cash-flow risk indicators.

Regulatory Source Trail

This dossier relies on official EU legal and institutional materials verified for the WEEE Directive, open-scope position, market data, collection and treatment objectives, reporting harmonisation and current evaluation process:

- European Commission — Waste from Electrical and Electronic Equipment (WEEE)

- European Commission — Frequently Asked Questions on the WEEE Directive

- EUR-Lex — Consolidated Directive 2012/19/EU on WEEE

- EUR-Lex — Implementing Regulation (EU) 2019/290 on Producer Registration and Reporting Format

- EUR-Lex — Implementing Regulation (EU) 2017/699 on Common Methodology for EEE and WEEE Calculation

- European Commission — WEEE Directive Evaluation, July 2025

Closing CTA · WEEE Financial Responsibility Defense

If WEEE cost is not priced before market entry, the company may discover producer responsibility only after revenue is already exposed.

Villanova ESG structures the producer-responsibility control architecture required to protect EU market access, quantify financial assurance exposure, reduce back-compliance risk and convert circular-economy performance into finance-grade evidence.

For a confidential WEEE scope and financial assurance exposure review, contact contact@villanovaesg.com.