CBAM 2026–2034: The Financial Impact on Your Supply Chain and the Cost of Inaction

CBAM now converts embedded emissions into margin exposure. CFOs must control product scope, emissions evidence, certificate-price sensitivity and contract allocation before European buyers price uncertainty into procurement.

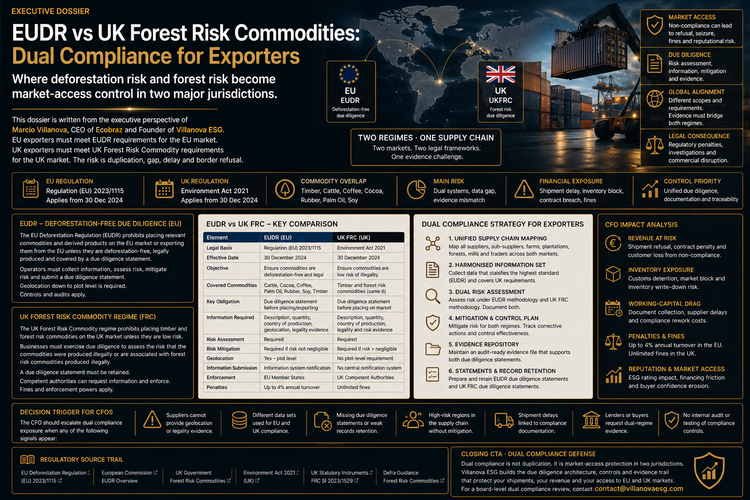

EUDR vs UK Forest Risk Commodities: Dual Compliance for Exporters

EUDR and UK Forest Risk Commodities rules create two different compliance tests for exporters. CFOs must unify origin, legality, geolocation, chain-of-custody and buyer evidence while keeping EU and UK legal outputs separate.

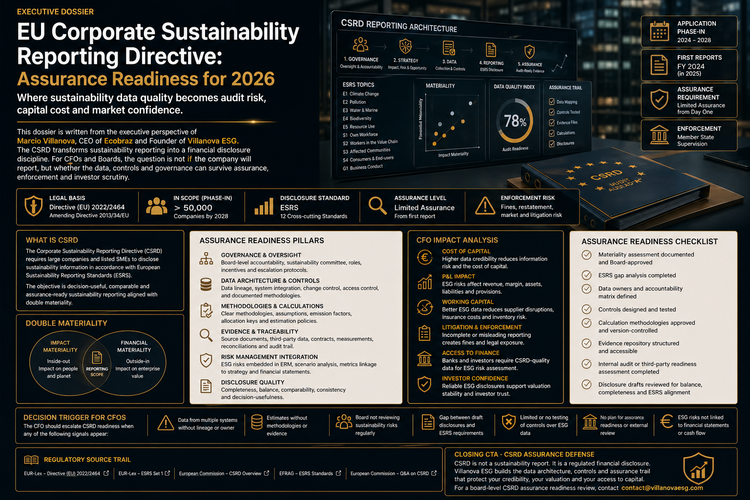

EU Corporate Sustainability Reporting Directive: Assurance Readiness for 2026

CSRD assurance readiness turns sustainability data into audit evidence. CFOs must control ESRS data ownership, source systems, materiality files, supplier evidence, internal controls and disclosure consistency before reporting becomes capital-market friction.

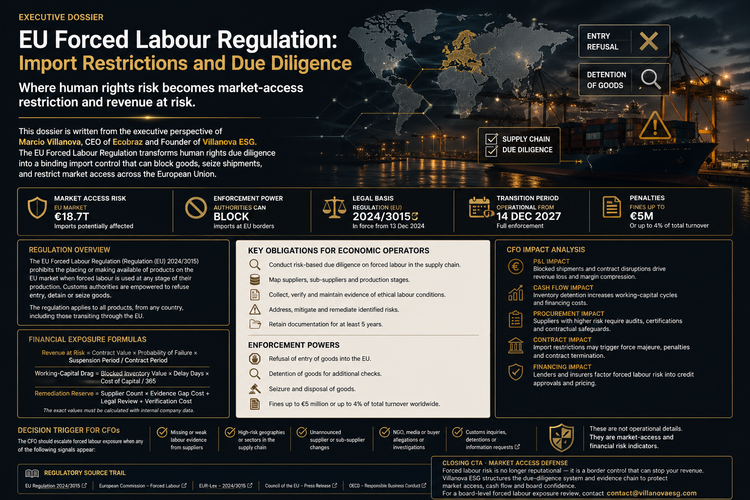

EU Forced Labour Regulation: Import Restrictions and Due Diligence

The EU Forced Labour Regulation turns human rights risk into market-access exposure. CFOs must control supplier mapping, labour-risk evidence, product linkage, customs readiness, remediation reserves and buyer contracts before forced labour allegations block shipments or revenue.

EU Textile Regulation: Product Data Is Becoming a Market-Access Risk

The EU textile regime is moving from product claims to product proof. For exporters, suppliers and CFOs exposed to Europe, product data is becoming a financial control.

WEEE Open-Scope 2026: New Categories and Financial Assurance Requirements

WEEE open scope is not new in 2026; it has applied since 15 August 2018. The current risk is SKU-level classification, producer registration, financial assurance, national reporting, take-back reserves and back-compliance exposure across EU Member States.

CSDDD and Board Duties: Fiduciary Responsibilities for Directors

CSDDD board exposure is not an automatic EU-wide fiduciary-liability rule. Directors face risk through national law, disclosure, oversight failure, D&O friction and weak governance evidence. CFOs must convert supplier due diligence into board-ready financial controls.

Green Claims Directive: Proving Environmental Statements under New Rules

The Green Claims Directive is not yet binding law, but environmental statements already create greenwashing and financial exposure.

EU Critical Raw Materials Act: Supply-Chain Risk for Rare Earths

The EU Critical Raw Materials Act turns rare earth dependency into strategic supply-chain risk. CFOs must map component-level exposure, supplier concentration, processing bottlenecks, recycling options, substitution cost and inventory buffers before critical raw material disruption damages margin.

EU Social Taxonomy: Preparing for Social Performance Metrics

The EU has not adopted a binding Social Taxonomy, but social performance metrics are already financially relevant through CSRD, CSDDD, SFDR, UNGPs and OECD due diligence.