EUDR vs UK Forest Risk Commodities: Dual Compliance for Exporters

Executive Dossier · EUDR vs UK Forest Risk Commodities

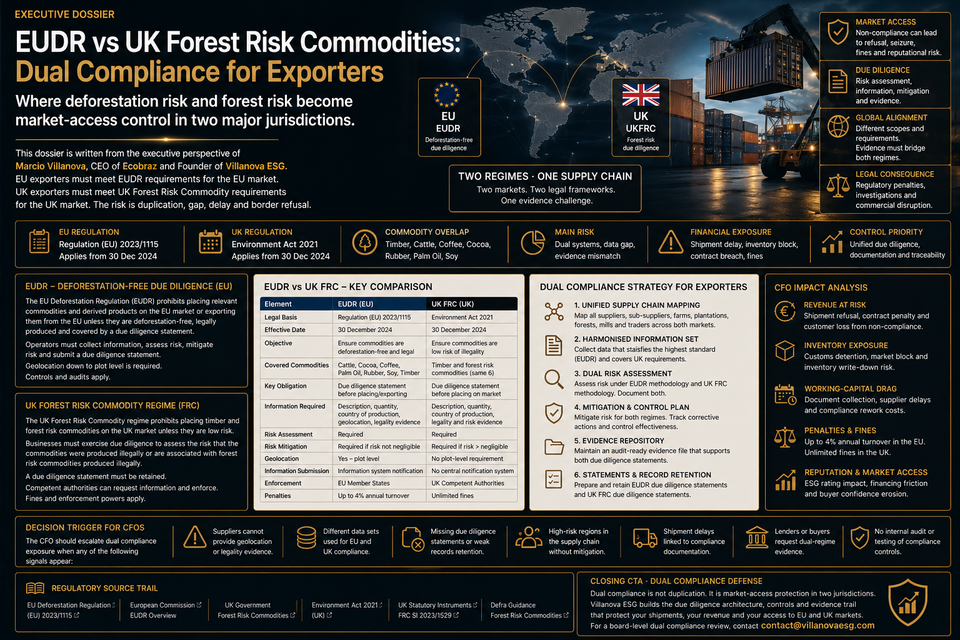

EUDR and UK Forest Risk Commodities rules create two different compliance systems for the same physical supply chain. Exporters that treat them as identical will overpay, under-control or misstate market-access risk.

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. The analysis treats dual deforestation compliance as a cash-flow and market-access control issue. The board question is direct: can the company build one evidence architecture strong enough to satisfy EU deforestation-free requirements and UK legality-based commodity due diligence without duplicating cost or creating disclosure gaps?

EU Regime

Regulation (EU) 2023/1115

UK Regime

Environment Act 2021 · Schedule 17

Compliance Gap

Deforestation-free vs legal production

Financial Exposure

Evidence duplication, shipment delay, buyer suspension

Two Jurisdictions. One Supply Chain. Different Legal Tests.

The EU and UK regimes are often discussed together because both target forest-risk supply chains. That comparison is useful but dangerous. The two systems are not identical.

The EUDR requires covered commodities and products to be deforestation-free, legally produced and covered by a due diligence statement before being placed on the EU market or exported from the EU. The UK Forest Risk Commodities regime, as enabled by the Environment Act 2021, is structured around the use of forest risk commodities in UK commercial activities where those commodities were not produced in accordance with relevant local laws.

Board Risk Signal

A shipment can satisfy one regime and still create evidence friction under the other if the control file is not designed for dual compliance.

The CFO should not fund two disconnected compliance systems. The correct architecture is a unified evidence layer with jurisdiction-specific outputs.

The Legal Status Must Be Kept Clear

The EUDR is adopted EU law. Its application has been delayed, but the legal framework is already established. Large and medium operators and traders are expected to comply from 30 December 2026, with a later date for micro and small operators.

The UK FRC regime is enabled by the Environment Act 2021, but the operational details depend on secondary legislation. The UK government announced intended initial commodities including palm oil, cocoa, beef, leather and soy. Until the secondary legislation is fully implemented, exporters must avoid claiming that the complete UK FRC regime is already operational in the same way as the EUDR.

01 · EUDR

Adopted regulation with delayed application dates and defined covered commodities and products.

02 · UK FRC

Enabled by primary legislation, but full operational details depend on secondary legislation.

03 · Exporter Control

Build evidence now, but label legal status correctly to avoid overclaiming or misdirecting resources.

Legal precision is not academic. Misstating the UK status can create customer confusion, contract risk and greenwashing exposure.

Commodity Scope: Overlap and Divergence

The EUDR covers cattle, cocoa, coffee, oil palm, rubber, soya and wood, plus listed derived products. The UK government’s stated initial FRC scope has focused on palm oil, cocoa, beef, leather and soy, while timber is already regulated separately in the UK.

Exporters must therefore avoid assuming full commodity equivalence. Coffee and rubber are EUDR commodities, but they are not necessarily within the UK initial FRC scope unless included by future UK secondary legislation. Timber is central to EUDR but interacts with the UK through existing timber legality controls.

Dual Commodity Exposure Map

High Overlap

Cocoa, soy, palm oil, beef and leather require dual-market evidence planning.

EUDR-Specific Risk

Coffee, rubber and wood require EUDR analysis and separate UK status review.

UK Timber Interaction

Timber must be mapped against EUDR and the UK’s existing timber legality framework.

The board should require commodity mapping by destination market. A single global “deforestation compliance” label is too weak for EU and UK exposure.

The Core Difference: Deforestation-Free vs Local-Law Legality

The EUDR creates a deforestation-free test based on a cut-off date, geolocation and legality. The UK FRC approach focuses on whether the commodity was produced in compliance with relevant local laws connected to the country of origin.

This difference changes the evidence file.

Dual Compliance Logic

EUDR Test = Deforestation-Free Status + Legal Production + Due Diligence Statement

UK FRC Test = Forest Risk Commodity + Relevant Local Law Compliance + Due Diligence and Reporting

Dual Evidence Gap = Evidence Needed for EU Test − Evidence Available for UK Test, and vice versa

Market Access Exposure = Product Revenue × Probability of Evidence Failure × Delay or Suspension Period / Contract Period

The exact values must be calculated with internal company data. A responsible model requires product revenue, commodity exposure, country of production, buyer deadlines, evidence maturity and market split between the EU and UK.

One Evidence Architecture, Two Outputs

Exporters should not build one system for EUDR and another system for UK FRC. That creates duplication, inconsistent records and cost. The better model is one evidence architecture that produces EU and UK outputs.

The unified evidence file should include:

- commodity and product classification;

- CN or tariff code where relevant;

- country of production;

- farm, plot, plantation, ranch or production area evidence;

- geolocation data where required for EUDR;

- local-law legality records;

- deforestation and land-use screening;

- supplier and sub-supplier chain-of-custody evidence;

- risk assessment and mitigation records;

- customer-specific due diligence output.

Control Principle

The evidence repository should be unified. The legal conclusions must remain jurisdiction-specific.

This is the key operating model for exporters selling into both markets.

Geolocation: Mandatory for EUDR, Not the Same UK Trigger

EUDR requires geolocation information for relevant plots of land. That makes origin data a legal control. The UK FRC regime is structured around legality under local laws, and current UK implementation details depend on secondary legislation. Exporters should therefore avoid assuming the UK will require identical geolocation mechanics unless the final rules say so.

Commercially, however, geolocation can still be valuable for UK buyers. It can help evidence legality, sourcing discipline, supplier risk controls and alignment with retailer or lender expectations.

EU Use Case

Geolocation is central to proving deforestation-free status under EUDR.

UK Use Case

Geolocation may support local-law legality evidence and buyer confidence, subject to final operational rules.

Exporter Control

Collect origin evidence once, then tag which fields satisfy each jurisdiction.

The CFO should fund a data architecture capable of separating mandatory legal fields from commercial evidence fields.

Due Diligence Reporting and Customer Pressure

The UK regime is expected to require regulated businesses to operate due diligence systems and report annually. The EUDR requires due diligence and submission of due diligence statements for covered products. Different reporting channels can create different evidence deadlines.

Exporters will feel the pressure through customers before regulators. EU and UK buyers may request supplier evidence, origin data, legality documents and risk mitigation records to protect their own compliance position.

Buyer Evidence Pressure Points

EU Importers

Need EUDR evidence, due diligence statement support and product-level traceability.

UK Retailers

May request local-law legality evidence, annual reporting support and supplier documentation.

Multinational Buyers

Will likely demand the stricter evidence package to protect both market channels.

The exporter that answers buyer evidence requests faster will protect margin and preferred-supplier status.

Financial Exposure Model

A CFO-grade model should convert dual compliance gaps into measurable P&L exposure.

Dual Compliance Financial Formula Stack

Revenue at Risk = EU and UK Customer Revenue × Probability of Evidence Failure × Suspension Period / Contract Period

Evidence Duplication Cost = Duplicate Data Fields × Collection Cost + Legal Review + System Reconciliation + Supplier Rework

Inventory Exposure = Affected Lot Value × Probability of Market Diversion, Delay or Rejection

Working-Capital Drag = Blocked Invoice Value × Evidence Delay Days × Cost of Capital / 365

The exact values must be calculated with internal company data. A responsible model requires EU and UK revenue split, commodity exposure, supplier count, evidence gap rate, affected lot value, buyer deadlines and cost of capital.

Contract Clauses Must Avoid Dual-System Asymmetry

Exporters selling into EU and UK channels must avoid accepting broad customer obligations without upstream supplier rights. Contracts should define which data must be delivered, when, in which format, and for which jurisdiction.

Supplier contracts should address:

- commodity origin disclosure;

- country-of-production evidence;

- geolocation data where required;

- local-law legality evidence;

- deforestation and land-use screening evidence;

- chain-of-custody records;

- supplier and sub-supplier disclosure;

- audit rights over farms, mills, processors and traders where commercially feasible;

- data delivery deadlines aligned with EU and UK buyer requirements;

- indemnity for false or incomplete origin or legality data where enforceable.

CFO Decision Rule

Do not accept dual-market compliance obligations from buyers unless upstream contracts give the company enforceable rights to origin, legality and traceability evidence.

The exporter should not carry evidence risk without contractual control over the data source.

The Data Architecture Must Tag Jurisdictional Relevance

The same raw evidence may support both regimes, but the legal use is different. The data system must tag each evidence field against its jurisdictional relevance.

EU Field Tag

Shows whether the data supports deforestation-free status, legality, risk assessment or due diligence statement submission.

UK Field Tag

Shows whether the data supports local-law legality, due diligence system operation or annual reporting evidence.

Commercial Field Tag

Shows whether the data supports customer evidence packs, lender diligence or sustainability-linked financing.

This prevents overcollection in one area and undercollection in another.

Exporter Scenario Planning

Dual compliance should be modelled through scenarios by commodity and market.

Dual Compliance Risk Scenarios

Base Case

One evidence repository satisfies EU and UK customer requests without duplicative supplier work.

Stress Case

UK buyer requests legality evidence that was not collected for an EU-focused EUDR workflow.

Severe Case

A material commodity lot cannot support either deforestation-free evidence or local-law legality evidence, triggering market diversion or customer suspension.

The scenario output should include revenue at risk, remediation cost, buyer delay, inventory exposure and contract renegotiation risk.

Dual Compliance and Sustainability-Linked Finance

Dual compliance can support financing when evidence is controlled. Banks and trade finance providers increasingly assess whether commodities tied to deforestation risk can maintain market access.

A unified evidence architecture can support:

- trade finance approvals;

- sustainability-linked loan evidence;

- buyer-backed supply-chain finance;

- insurance review;

- working-capital planning;

- customer risk segmentation.

The threshold is auditability. Claims about responsible sourcing do not improve credit posture unless the evidence file can survive EU and UK diligence.

The Villanova ESG Control Architecture

Villanova ESG operates exclusively at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains. For EUDR and UK FRC dual compliance, the objective is not to duplicate reporting. The objective is to build one evidence system that supports two markets, two buyer groups and two legal tests.

01 · Dual Commodity Map

Map EU and UK commodity exposure by product, buyer, market, tariff code, supplier and country of production.

02 · Unified Evidence File

Build one repository for geolocation, legality, deforestation screening, supplier evidence and chain-of-custody records.

03 · Jurisdictional Tagging

Tag each data field against EUDR, UK FRC, buyer, lender and internal governance requirements.

04 · Contract Control

Insert origin disclosure, legality proof, geolocation rights, audit rights, evidence deadlines and indemnity clauses where enforceable.

05 · CFO Risk Model

Quantify revenue at risk, evidence duplication cost, inventory exposure, buyer delay and working-capital drag.

06 · Board Dashboard

Translate dual compliance into EU/UK market exposure, customer retention risk, margin exposure and lender-readable evidence.

Decision Trigger for CFOs

The CFO should escalate dual compliance exposure when any of the following signals appear:

- products are sold into both the EU and UK and contain cocoa, soy, palm oil, beef, leather, coffee, rubber or timber inputs;

- the company assumes EUDR and UK FRC require identical evidence without legal review;

- geolocation data exists for EU purposes but local-law legality evidence is incomplete;

- UK buyer evidence requests are handled separately from the EUDR evidence repository;

- supplier contracts do not require origin, legality, geolocation and chain-of-custody evidence;

- timber exposure is not mapped separately against UK timber legality rules and EUDR requirements;

- the company cannot produce market-specific evidence packs within buyer deadlines;

- lenders ask for responsible sourcing evidence across EU and UK channels;

- management cannot quantify evidence duplication, buyer delay, inventory exposure or revenue at risk.

These are not documentation issues. They are dual-market access and cash-flow risk indicators.

Regulatory Source Trail

This dossier relies on official EU and UK legal materials and current implementation references verified for the EUDR and UK Forest Risk Commodities position:

- European Commission — Regulation on Deforestation-free Products

- European Commission Access2Markets — EUDR delay until December 2026

- EUR-Lex — Regulation (EU) 2023/1115

- UK Legislation — Environment Act 2021, Schedule 17

- UK Government — Initial forest risk commodities announcement

- DEFRA — Implementing due diligence on forest risk commodities

Closing CTA · Dual Compliance Defensibility

If your commodity evidence can satisfy only one jurisdiction, the other market may become the hidden source of margin loss.

Villanova ESG structures buyer-readable, audit-grade evidence architecture to support EU and UK regulatory defensibility, reduce exposure to cash-flow disruption and convert deforestation due diligence into finance-grade documentation for boards, buyers, lenders and compliance teams.

For a board-level EUDR and UK FRC exposure review, contact contact@villanovaesg.com.