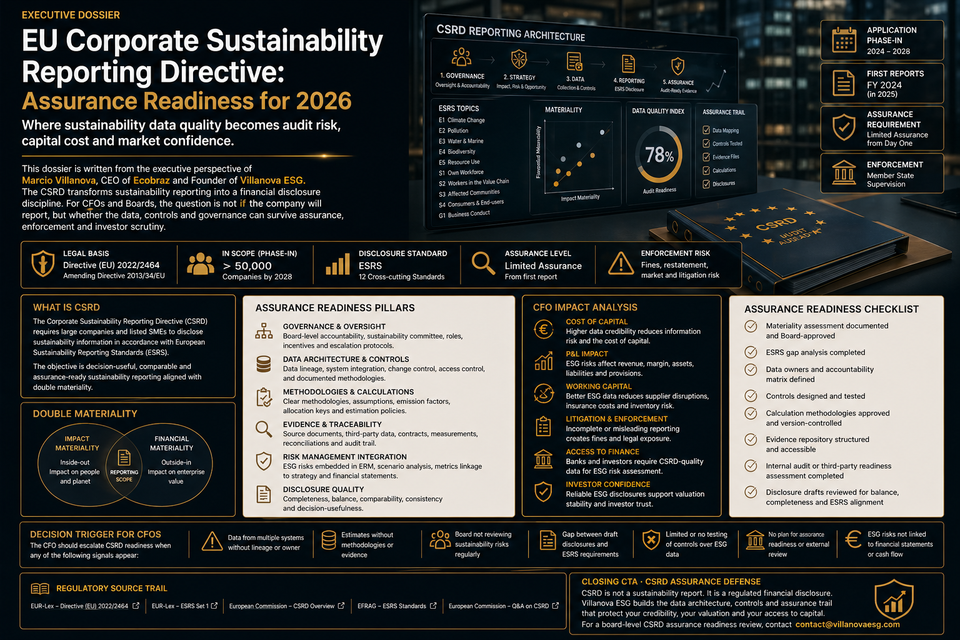

EU Corporate Sustainability Reporting Directive: Assurance Readiness for 2026

Executive Dossier · CSRD Assurance Readiness

CSRD assurance readiness is not a reporting project. It is a control-system test. If sustainability data cannot be traced, reconciled and governed, the company carries audit delay, disclosure correction and capital-market risk.

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. The analysis treats CSRD assurance as a finance-grade evidence discipline. The board question is direct: can the company prove sustainability information with the same control logic used for financial reporting before auditors, lenders, investors or buyers challenge the statement?

Legal Framework

CSRD and ESRS

Assurance Exposure

Limited assurance and audit evidence

2026 Control Issue

Data controls, evidence files, governance ownership

Financial Exposure

Audit delay, restatement risk, credit friction

CSRD Assurance Is a Control Test, Not a Narrative Review

The CSRD requires in-scope companies to report sustainability information under the ESRS. The purpose is not to produce a polished sustainability report. The purpose is to provide structured, comparable and decision-useful information that can be assured.

For CFOs, the assurance challenge is operational. Sustainability data often sits across procurement, HR, legal, EHS, finance, operations, supplier portals, spreadsheets, emissions platforms and customer systems. Auditors will test whether the reported data is complete, traceable, controlled and consistent with the company’s materiality assessment.

Board Risk Signal

A CSRD statement without audit-ready source evidence is not a disclosure asset. It is a reporting liability.

The board should treat CSRD assurance readiness as a financial-control maturity exercise. If the data cannot survive assurance, it cannot support lender confidence, investor communication or buyer due diligence.

The Omnibus Simplification Does Not Remove Evidence Risk

Omnibus I simplified sustainability reporting and due diligence requirements, reduced administrative burden and limited the trickle-down effect on smaller companies. That does not eliminate assurance exposure for companies that remain in scope or that supply data to in-scope customers, investors or lenders.

In practice, simplification changes the perimeter. It does not remove the need for evidence. In-scope companies still need defensible sustainability information. Suppliers outside the direct scope may still face buyer data requests where their information is required for customer reporting, assurance, procurement or financing.

01 · Direct Reporting Exposure

The company remains within CSRD scope and must prepare ESRS-based disclosures with assurance evidence.

02 · Buyer-Driven Exposure

A supplier outside direct scope may still need to provide auditable ESG data to EU customers.

03 · Financing Exposure

Banks, funds and insurers may rely on sustainability data for credit, pricing, covenants and diligence.

The CFO should not wait for legal scope clarity to build data controls. Assurance readiness is also a commercial capability.

Assurance Readiness Starts with Data Ownership

The first failure point is unclear ownership. Sustainability data often has no single accountable owner, no formal review process and no reconciliation to operational systems.

Every material data point should have a control owner, source system, calculation method, evidence file, review procedure and approval trail.

CSRD Data-Control Stack

Data Owner

Executive or functional owner accountable for completeness, methodology and evidence.

Source System

ERP, HRIS, EHS system, supplier portal, utility data, meter, legal record or finance system.

Evidence Trail

Invoices, meter readings, contracts, supplier declarations, audit reports, calculations and review logs.

Approval Control

Documented review, sign-off, exception handling, version control and board escalation where material.

If the company cannot identify who owns a data point, it is not ready for assurance.

Double Materiality Must Be Assurance-Ready

The materiality assessment is the gatekeeper of CSRD reporting. It determines which sustainability matters, impacts, risks and opportunities become reportable. If the materiality process is weak, the entire sustainability statement is exposed.

Assurance readiness requires a defensible materiality file:

- methodology and scoring criteria;

- impact materiality thresholds;

- financial materiality thresholds;

- stakeholder input records;

- value-chain mapping;

- risk and opportunity rationale;

- included and excluded topic rationale;

- management review records;

- board approval evidence;

- updates after regulatory or business-model changes.

Control Principle

An elegant materiality matrix is not assurance evidence. The methodology and source records are.

The CFO should require materiality evidence to be reviewable by internal audit before external assurance begins.

Internal Controls Must Extend Beyond Finance

CSRD assurance pushes sustainability information into the internal-control environment. Finance teams understand close processes, reconciliations and audit evidence. Sustainability teams often work with looser data flows. That gap must be closed.

Assurance Readiness Formula Stack

Assurance Readiness = Data Ownership + Source Evidence + Control Testing + Board Approval

Audit Delay Risk = Material Data Points × Evidence Gap Rate × Assurance Rework Factor

Restatement Exposure = Probability of Material Error × Disclosure Correction Cost + Legal Review + Investor Communication

Capital Friction = Debt or Equity Exposure × Basis-Point Impact from Weak ESG Controls

The exact values must be calculated with internal company data. A responsible model requires ESRS data-point inventory, assurance scope, evidence gap rate, auditor findings, debt exposure, investor sensitivity and cost of capital.

Supplier Data Is the Weakest Link

CSRD assurance risk often sits outside the company. Value-chain information depends on suppliers, logistics providers, contractors, customers and external data sources.

Supplier data becomes risky when it is based on self-declarations, estimates, unsupported spreadsheets or outdated questionnaires. Auditors may challenge the reliability, boundary, consistency and documentation of that data.

Supplier Emissions Data

Scope 3, product carbon, CBAM and energy data must be source-controlled and methodologically documented.

Human Rights Data

Supplier audits, grievances, remediation records and forced-labour controls must be traceable.

Product Compliance Data

EUDR, WEEE, DPP, battery, ecodesign and product evidence must reconcile to operational records.

The CFO should require supplier data rights in procurement contracts. No audit-ready supplier data, no assurance-ready CSRD statement.

The Evidence Room Becomes a Reporting Asset

A CSRD evidence room should be built before the reporting deadline. Waiting until the auditor requests documents creates rework, delays and weak response discipline.

The evidence room should include:

- ESRS data-point inventory;

- materiality assessment file;

- data owner matrix;

- calculation methodology;

- source-system exports;

- supplier evidence;

- review and approval logs;

- internal-control testing records;

- board and committee minutes;

- assurance questions and management responses.

The evidence room is not an archive. It is the operating infrastructure for assurance.

Disclosure Consistency Is a Capital-Market Control

CSRD disclosures must align with investor presentations, lender materials, sustainability-linked loans, website claims, green claims, SFDR data requests and customer due diligence responses.

The risk is inconsistency. A company can pass one disclosure process and still create exposure if another public or private statement says something stronger, weaker or contradictory.

Disclosure Consistency Controls

CSRD Statement

Main sustainability disclosure under ESRS, linked to materiality and assurance evidence.

Capital Materials

Investor decks, loan materials, green bond frameworks and sustainability-linked facility documentation.

Commercial Materials

Customer ESG questionnaires, supplier scorecards, green claims, product claims and procurement documents.

The CFO should enforce one evidence spine across all sustainability communications.

Assurance Findings Must Feed Risk Management

Assurance should not be treated as a one-year reporting event. Auditor findings should recalibrate internal controls, data ownership, supplier contracts, board reporting and remediation plans.

Findings should be classified by severity:

- data gap;

- methodology weakness;

- control deficiency;

- source-system weakness;

- supplier evidence failure;

- boundary inconsistency;

- materiality rationale issue;

- board governance gap;

- disclosure inconsistency;

- potential restatement exposure.

CFO Decision Rule

Do not close the CSRD cycle until assurance findings have been converted into control remediation, budget and ownership.

Audit findings are not criticism. They are a risk-control map.

Financial Exposure Model

A CFO-grade model should translate CSRD assurance weakness into measurable financial exposure.

CSRD Assurance Financial Formula Stack

Assurance Rework Cost = Data Gap Count × Closure Cost + Auditor Rework + Legal Review + Management Time

Reporting Delay Cost = Delay Days × Reporting Team Cost + Investor Communication Cost + Governance Escalation Cost

Disclosure Correction Exposure = Probability of Material Error × Correction Cost + Assurance Rework + Legal Review

Credit Friction = Debt Exposure × Basis-Point Increase from Weak Sustainability-Control Environment

The exact values must be calculated with internal company data. A responsible model requires assurance workplan, auditor findings, ESRS data-point inventory, reporting timeline, debt exposure, lender sensitivity and remediation budget.

Assurance Readiness and Sustainability-Linked Loans

CSRD assurance readiness can strengthen financing discussions when sustainability data is controlled. Lenders do not finance narratives. They finance risk evidence.

A CSRD-ready control environment can support:

- sustainability-linked loan KPI credibility;

- green bond evidence;

- trade finance diligence;

- buyer-backed financing;

- credit risk assessment;

- investor confidence in transition strategy.

Weak assurance readiness can do the opposite. It can expose unverified claims, inconsistent KPIs and weak governance behind lender-facing statements.

Board Oversight Must Be Documented

The board should not only approve the CSRD report. It should oversee the assurance-readiness architecture.

The board file should show:

- approval of materiality methodology;

- review of material IROs;

- review of data-control maturity;

- budget for assurance readiness;

- internal audit involvement;

- supplier data risk escalation;

- review of assurance findings;

- approval of remediation plan;

- disclosure consistency review;

- capital-market communication alignment.

Board minutes should prove challenge, not just acceptance.

The Villanova ESG Control Architecture

Villanova ESG operates exclusively at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains. For CSRD assurance readiness, the objective is not to write a sustainability report. The objective is to build an evidence architecture that protects disclosure credibility, financing access and board defensibility.

01 · ESRS Data Inventory

Map required disclosures, data points, owners, source systems, evidence maturity and assurance-risk status.

02 · Materiality Evidence File

Document double materiality methodology, thresholds, IRO rationale, stakeholder inputs and board approval.

03 · Internal Control Layer

Build review, approval, reconciliation, exception, version control and evidence retention procedures for material data.

04 · Supplier Evidence Protocol

Secure value-chain data rights, methodology requirements, assurance support and audit evidence from strategic suppliers.

05 · CFO Exposure Model

Quantify assurance rework, reporting delay, disclosure correction, remediation budget and credit-friction exposure.

06 · Board Dashboard

Translate CSRD assurance readiness into governance action, capital access, risk appetite and disclosure confidence.

Decision Trigger for CFOs

The CFO should escalate CSRD assurance exposure when any of the following signals appear:

- ESRS data points do not have named owners and source systems;

- materiality decisions cannot be traced to methodology, evidence and board approval;

- supplier data is based on self-declarations without source evidence or contractual data rights;

- sustainability KPIs used in lender materials are not reconciled to the CSRD evidence file;

- internal audit has not tested material sustainability controls;

- assurance requests are being answered manually through spreadsheets and emails;

- board minutes do not show challenge of materiality, data quality and assurance findings;

- CSRD disclosures are inconsistent with green claims, investor decks or customer ESG responses;

- management cannot quantify assurance rework, reporting delay, disclosure correction or credit-friction exposure.

These are not reporting details. They are audit, governance and capital-access risk indicators.

Regulatory Source Trail

This dossier relies on official EU and EFRAG materials verified for the current CSRD, ESRS and assurance-readiness position:

- European Commission — Corporate sustainability reporting

- EUR-Lex — Directive (EU) 2022/2464, Corporate Sustainability Reporting Directive

- EUR-Lex — Commission Delegated Regulation (EU) 2023/2772 on ESRS

- EFRAG — Draft Simplified ESRS

- Council of the European Union — Simplification of sustainability reporting and due diligence requirements

- EFRAG — ESRS Implementation Guidance Documents

Closing CTA · CSRD Assurance Defense

If your sustainability data cannot be traced from disclosure to source evidence, CSRD assurance risk is already inside the reporting process.

Villanova ESG structures the regulatory shield required to protect disclosure credibility, preserve capital access and convert CSRD assurance readiness into finance-grade evidence for boards, auditors, buyers and lenders.

For a board-level CSRD assurance exposure review, contact contact@villanovaesg.com.