EU Forced Labour Regulation: Import Restrictions and Due Diligence

Executive Dossier · EU Forced Labour Regulation

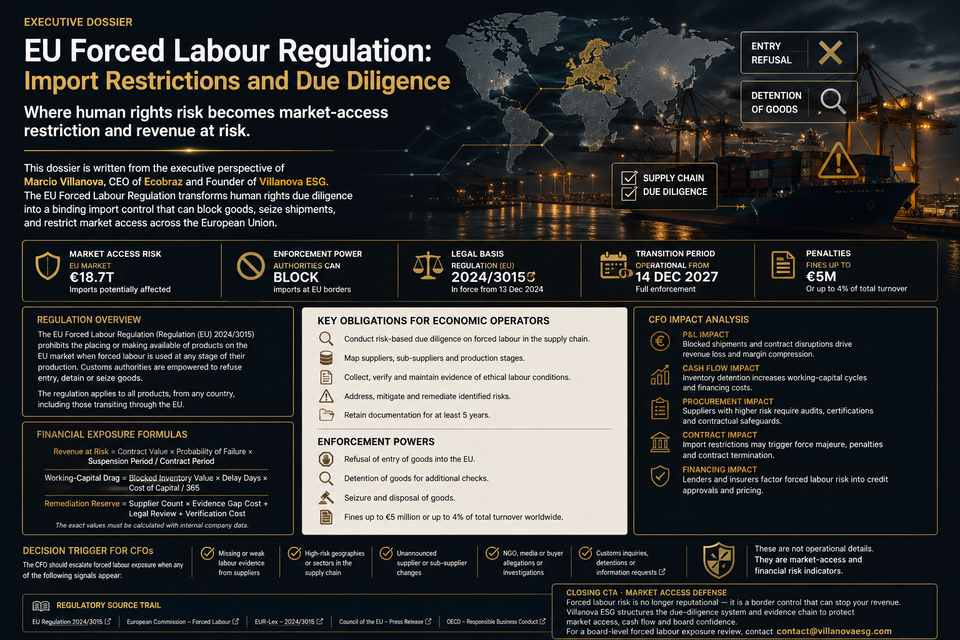

The EU Forced Labour Regulation converts human rights risk into a market-access control. For CFOs, the exposure is no longer only reputational. It is border restriction, inventory seizure, buyer suspension and cash-flow interruption.

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. The analysis treats forced labour compliance as a supply-chain evidence and revenue-protection issue. The board question is direct: can the company prove that products, components, raw materials and supplier relationships are not exposed to forced labour before EU authorities, customs systems, buyers or lenders challenge market access?

Legal Instrument

Regulation (EU) 2024/3015

Entered into Force

13 December 2024

Application Date

14 December 2027

Core Exposure

Market ban, withdrawal, disposal, customs enforcement

Forced Labour Risk Is Now a Border-Control Problem

The EU Forced Labour Regulation prohibits products made with forced labour from being placed or made available on the EU market. It also applies to exports from the EU. The scope is broad: all products, all sectors, and all origins can be captured where forced labour is used at any stage of production, manufacture, harvest or extraction.

This changes the risk model for exporters and EU importers. Forced labour risk is no longer only a social audit issue. It can become a customs, inventory, contract and financing event.

Board Risk Signal

A product with unresolved forced labour exposure is not saleable inventory. It is market-access risk waiting for a border decision.

The CFO should treat forced labour compliance as a revenue-continuity control. The question is whether the company can prove supplier evidence before authorities, buyers or lenders ask for it.

The Scope Is Product-Based, Not Company-Size-Based

The Forced Labour Regulation is not built around a company-size threshold in the same way as CSRD or CSDDD. It is product-based. The prohibition applies to products made with forced labour, regardless of whether the economic operator is large, medium or small.

That creates a practical commercial exposure for suppliers outside the EU. Even if a supplier is not directly subject to EU corporate due diligence rules, its product can still be blocked if forced labour is found in the supply chain.

01 · Imported Products

Goods entering the EU can face investigation, refusal, withdrawal or disposal where forced labour is substantiated.

02 · EU-Made Products

Products made within the EU can also fall within the prohibition where forced labour is used.

03 · EU Exports

Products made with forced labour cannot be exported from the EU market.

The board should not wait for direct statutory scope analysis. The real exposure is product eligibility.

How Enforcement Works

The enforcement model is risk-based. The Commission and competent authorities can assess information from stakeholders, reports, risk indicators and other relevant sources. Where there are substantiated concerns, they can launch formal investigations. Where forced labour is found, authorities can prohibit the product, order withdrawal and disposal, and coordinate enforcement with customs and competent authorities.

The Commission leads cases involving forced labour outside the EU. National competent authorities lead cases involving forced labour within the EU. EU countries must designate competent authorities, and the Commission will develop support tools, including a forced labour database, guidelines, the Forced Labour Single Portal and information systems for case management.

Enforcement Control Path

Preliminary Assessment

Authorities assess risk indicators, reports, stakeholder information and operator responses.

Formal Investigation

Operators may be required to provide documents, supply-chain information and evidence concerning the product.

Decision

If forced labour is found, authorities can prohibit market entry, order withdrawal and require disposal.

Customs Enforcement

Customs and competent authorities enforce prohibition decisions at the EU border and market level.

The commercial risk is time. A product can be contractually sold and logistically shipped, but still become blocked if the evidence file cannot answer forced labour concerns.

Due Diligence Is Not Formally a Safe Harbour

The Regulation does not create a simple safe harbour where generic due diligence automatically protects a product. However, due diligence evidence is commercially and procedurally critical. Authorities will use a risk-based approach, and operators that can produce credible supplier evidence are better positioned to respond.

The correct board position is disciplined: due diligence does not guarantee immunity, but weak due diligence increases market-access exposure.

Control Principle

Forced labour due diligence is not a certificate. It is a defense file for market-access decisions.

The CFO should ask whether the company can produce forced labour evidence within authority, buyer or lender deadlines.

High-Risk Sectors and Inputs

The Regulation applies across sectors, but enforcement will focus on high-risk sectors, products and regions. The Commission will publish a database with indicative forced labour risks in specific geographic areas or products. That database should become a procurement-control input.

Companies should expect higher scrutiny where products involve:

- agricultural commodities;

- textiles and apparel;

- electronics and solar components;

- mining and mineral inputs;

- seafood and processing chains;

- logistics-intensive subcontracting;

- migrant labour dependence;

- labour brokers or recruitment agencies;

- state-imposed labour risk;

- high-risk geographies flagged by credible sources.

The risk is not only the direct supplier. It may sit in raw materials, subcontracting, processing, labour recruitment or state-linked labour schemes.

The Supplier Evidence File

Supplier declarations are not enough. Forced labour risk must be supported by evidence that reaches the production stage where risk can occur.

Forced Labour Evidence Architecture

Supplier Mapping

Supplier, sub-supplier, production site, labour broker, subcontractor and raw-material origin mapping.

Labour Controls

Recruitment fee controls, worker contracts, document-retention policy, grievance access and non-retaliation controls.

Audit Evidence

Worker interviews, third-party assessments, corrective action plans, closure records and follow-up monitoring.

Product Linkage

Evidence must connect to specific products, batches, components, supplier lots, purchase orders and customer contracts.

The evidence file must be product-linked. A general supplier policy will not protect a specific shipment if the allegation concerns a specific factory, region, input or labour scheme.

Import Restrictions Create Working-Capital Exposure

Forced labour enforcement can create direct working-capital pressure. Goods can be delayed, refused, withdrawn or disposed of. Customers may suspend orders. Invoices can be blocked while evidence is reviewed. Inventory can become unsellable in the EU.

Forced Labour Financial Risk Formula Stack

Revenue at Risk = EU Contract Revenue × Probability of Forced Labour Evidence Failure × Suspension Period / Contract Period

Inventory Exposure = Affected Inventory Value × Probability of Refusal, Withdrawal or Disposal

Working-Capital Drag = Blocked Invoice Value × Delay Days × Cost of Capital / 365

Remediation Reserve = Supplier Count × Evidence Gap Cost + Audit Cost + Worker Remediation + Legal Review

The exact values must be calculated with internal company data. A responsible model requires EU revenue exposure, supplier segmentation, product inventory value, buyer deadlines, evidence maturity, audit cost, remediation cost and cost of capital.

Forced Labour Risk Is Not Limited to Tier One

Most forced labour risk sits below tier one. It can arise through recruitment agencies, migrant worker channels, raw material extraction, state-imposed labour, subcontracted production, informal workshops, processing facilities or logistics labour.

Boards should require risk mapping by:

- product category;

- country and region;

- sector and commodity;

- supplier and sub-supplier;

- labour broker and recruitment channel;

- production site;

- worker profile;

- audit history;

- complaint history;

- customer revenue dependency.

Forced labour risk cannot be controlled if procurement only sees direct supplier names.

Buyer Contracts Will Transfer the Burden Upstream

EU buyers will not wait until 2027 to request evidence. Strategic customers will begin shifting burden upstream through supplier codes, contract clauses, audit rights, evidence requests and indemnities.

Supplier contracts should address:

- forced labour and forced child labour prohibition;

- supplier and sub-supplier disclosure;

- labour broker disclosure;

- audit rights and worker interview rights where lawful;

- recruitment fee prohibition and repayment obligations;

- document retention and passport retention controls;

- grievance access and non-retaliation safeguards;

- corrective action plan deadlines;

- shipment suspension and rejection rights;

- indemnity for false or incomplete labour-risk information where enforceable.

CFO Decision Rule

Do not accept forced labour evidence obligations from EU customers unless upstream supplier contracts give the company the right to obtain and verify the evidence.

The commercial risk is asymmetry: accepting buyer obligations without supplier rights converts compliance into margin risk.

Customs and Product-Linkage Controls

Market-access restriction is product-specific. That means evidence must connect human rights due diligence to customs, logistics and product records.

Product Code

The company must link forced labour evidence to product classification, SKU and customs documentation.

Supplier Lot

Evidence must connect to supplier lots, batches, components or raw materials in the relevant product chain.

Shipment File

Shipping records, invoices, purchase orders and product evidence must be reconciled before border challenge.

A strong human rights policy without shipment-level evidence is commercially weak.

Remediation Must Protect Workers and Market Access

Forced labour remediation is operationally sensitive. Immediate supplier termination can worsen harm if workers are left without remedy. But slow action can increase buyer, regulator and lender risk.

A credible remediation protocol should define:

- worker protection measures;

- repayment of recruitment fees where applicable;

- safe grievance channels;

- non-retaliation controls;

- corrective action owner;

- timeline and verification method;

- supplier suspension logic;

- buyer communication protocol;

- evidence preservation;

- financial reserve for remediation and substitution.

Remediation must protect affected workers and preserve defensible evidence for market-access decisions.

Scenario Planning for Import Restrictions

The CFO should run scenario planning before the Regulation applies. The worst position is to face a forced labour allegation after goods have been shipped and invoices are pending.

Forced Labour Risk Scenarios

Base Case

Supplier evidence is complete, buyer diligence is satisfied and shipments continue without delay.

Stress Case

A high-risk supplier or region is flagged, forcing urgent evidence collection, buyer notification and temporary shipment hold.

Severe Case

Authorities conclude forced labour exposure, triggering market prohibition, withdrawal, disposal and customer contract damage.

The scenario output should include revenue at risk, inventory exposure, remediation reserve, substitution cost and working-capital impact.

Forced Labour Regulation and Sustainability-Linked Finance

Forced labour controls can affect financing. Lenders increasingly test whether supply-chain human rights risks are identified, governed and evidenced. A company using sustainability-linked loans or social-risk claims must be able to prove supplier controls.

Weak forced labour evidence can undermine:

- sustainability-linked loan KPIs;

- trade finance approvals;

- buyer-backed supply-chain finance;

- public procurement eligibility;

- insurance review;

- investor disclosure credibility.

The financing issue is evidence quality. Human rights claims without supply-chain proof are not credit-positive.

The Villanova ESG Control Architecture

Villanova ESG operates exclusively at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains. For the EU Forced Labour Regulation, the objective is not a social policy. The objective is to protect market access with product-linked forced labour evidence that can survive buyers, customs authorities, regulators and lenders.

01 · Product Exposure Map

Map EU-bound products, components, raw materials, supplier lots and customer contracts exposed to forced labour risk.

02 · Supplier Risk Segmentation

Classify suppliers by country, sector, labour profile, recruitment model, subcontracting opacity and auditability.

03 · Evidence File

Build product-linked evidence for labour controls, audits, grievance channels, remediation and supplier documentation.

04 · Contract Shield

Insert forced labour prohibitions, supplier disclosure, audit rights, remediation duties, suspension triggers and indemnity clauses.

05 · CFO Risk Model

Quantify revenue at risk, inventory exposure, working-capital drag, remediation reserve and supplier substitution cost.

06 · Board Dashboard

Translate forced labour exposure into market-access readiness, buyer confidence, shipment risk and lender-ready evidence.

Decision Trigger for CFOs

The CFO should escalate forced labour exposure when any of the following signals appear:

- EU-bound products involve high-risk countries, sectors, commodities or labour-intensive production stages;

- supplier mapping stops at tier one and does not reach subcontractors, labour brokers or raw-material origins;

- workers may be exposed to recruitment fees, debt bondage, document retention or coercive labour conditions;

- buyers request forced labour evidence the company cannot produce quickly;

- supplier contracts lack audit rights, labour-broker disclosure, remediation obligations or shipment suspension rights;

- product, batch, shipment and supplier evidence cannot be reconciled;

- NGO, media, worker, union or authority reports identify forced labour risk in the product chain;

- lenders or insurers request human rights evidence linked to trade finance or sustainability-linked facilities;

- management cannot quantify revenue at risk, inventory exposure and working-capital drag from forced labour enforcement.

These are not social-compliance details. They are market-access and cash-flow risk indicators.

Regulatory Source Trail

This dossier relies on official EU regulatory materials and implementation references verified for the current EU Forced Labour Regulation position:

- European Commission — The Forced Labour Regulation

- EUR-Lex — Regulation (EU) 2024/3015

- European Commission — Questions and answers on prohibiting products made with forced labour

- European Parliament — Products made with forced labour to be banned from EU single market

- International Labour Organization — Forced labour, modern slavery and human trafficking

- OECD — Due Diligence Guidance for Responsible Business Conduct

Closing CTA · Forced Labour Market-Access Defense

If your product can be challenged for forced labour exposure but your evidence file is supplier-level only, EU market access is already exposed.

Villanova ESG structures the regulatory shield required to protect EU revenue, preserve cash flow and convert forced labour due diligence into finance-grade evidence for boards, buyers, customs authorities and lenders.

For a board-level forced labour exposure review, contact contact@villanovaesg.com.