The Hidden Cost of Supplier Non-Readiness Under EU Regulation

Financial Risk Memo

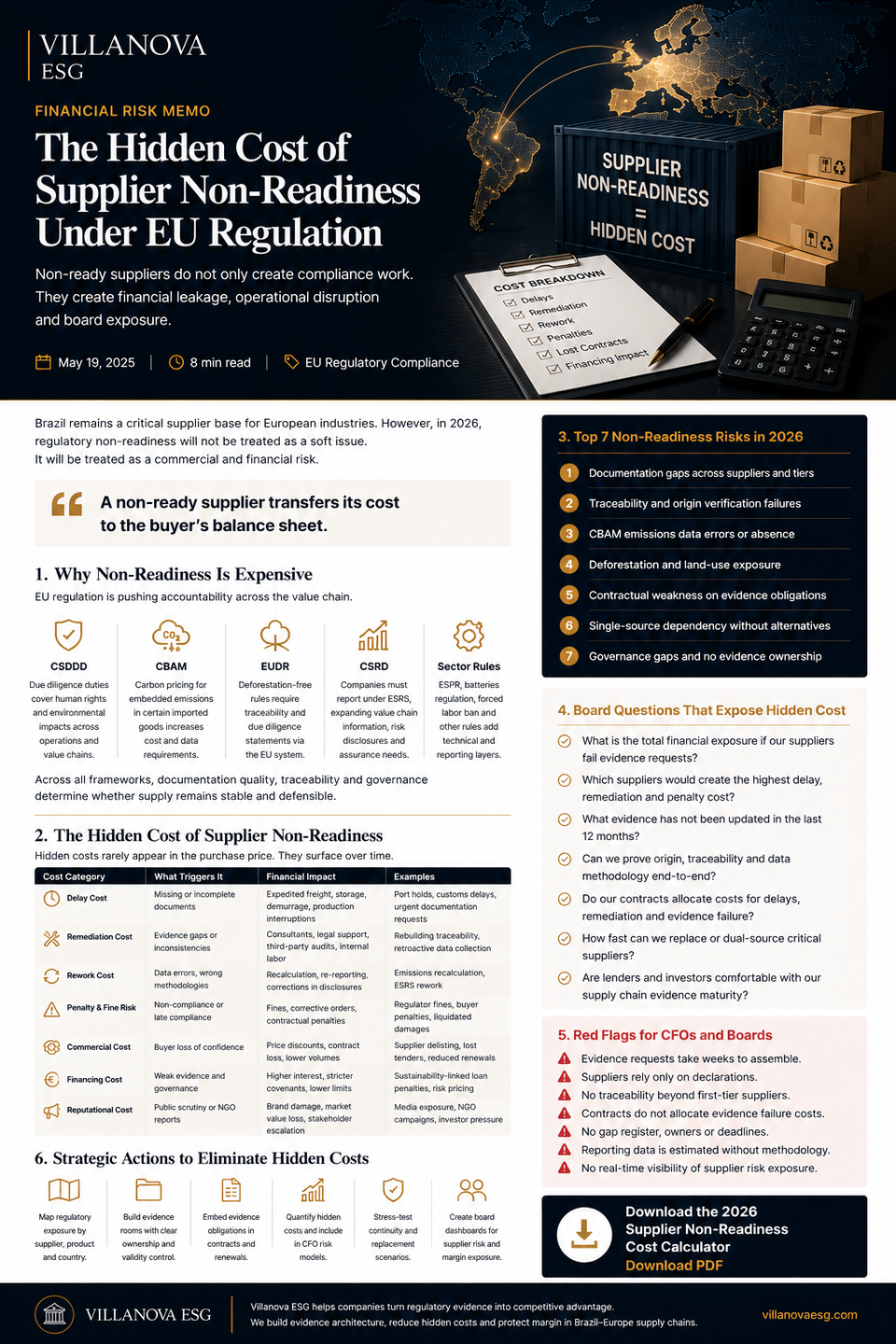

The Hidden Cost of Supplier Non-Readiness Under EU Regulation

Supplier non-readiness is not a soft compliance issue. It creates hidden cost across remediation, delays, contract friction, financing review and board-level exposure.

Cost Driver

Non-Readiness

CFO Exposure

Hidden Cost

Board Question

Price or Absorb

Executive Thesis

Supplier non-readiness rarely appears in the purchase price. It appears later as emergency documentation work, delayed shipments, re-testing, legal review, audit response, financing friction, customer escalation and replacement cost.

For EU buyers sourcing from Brazil, non-readiness is not theoretical. It is the gap between what a supplier declares and what the buyer can prove.

A non-ready supplier transfers its cost to the buyer’s balance sheet.

CFOs should therefore stop treating supplier readiness as an ESG maturity question. It is a financial control question.

Why Non-Readiness Is Becoming Expensive

The Corporate Sustainability Due Diligence Directive entered into force on 25 July 2024. The European Commission states that the directive aims to foster sustainable and responsible corporate behaviour across companies’ own operations, subsidiaries and global value chains. This makes supplier due diligence and evidence readiness relevant to governance and risk control for companies in scope.

CBAM increases the cost relevance of supplier data for covered imports. The European Commission describes CBAM as a system to confirm that a carbon price has been paid for embedded carbon emissions generated in the production of certain goods imported into the EU.

EUDR reinforces traceability discipline. The Information System acts as the repository of due diligence statements submitted by operators and traders pursuant to the regulation. This makes supplier origin, commodity exposure and document readiness a material issue for covered product categories.

CSRD adds reporting pressure for companies in scope because they report according to European Sustainability Reporting Standards. Supplier data quality can therefore affect internal reporting discipline, lender review and investor confidence.

The Hidden Cost Stack

Supplier non-readiness creates cumulative financial leakage. The cost is usually distributed across departments, which makes it difficult to see until pressure rises.

| Cost Category | Trigger | Financial Impact | Typical Owner |

|---|---|---|---|

| Delay Cost | Missing documents, incomplete declarations or unresolved buyer requests. | Expedited freight, storage, demurrage, production interruption and delivery penalties. | Logistics / Operations |

| Remediation Cost | Evidence gaps, weak traceability or outdated supplier records. | Consultants, legal review, supplier audits, data reconstruction and internal labor. | Compliance / Legal |

| Rework Cost | Wrong methodology, poor data quality or inconsistent reporting inputs. | Recalculations, re-submissions, reclassification and report correction. | ESG / Finance |

| Commercial Cost | Buyer loses confidence in supplier defensibility. | Discount pressure, reduced order volume, tender loss or supplier delisting. | Sales / Procurement |

| Financing Cost | Lenders or investors question evidence quality, governance or data reliability. | Higher diligence burden, weaker credit signal or reduced sustainability-linked readiness. | CFO / Treasury |

| Reputation Cost | Public scrutiny, customer challenge, NGO report, media inquiry or investor concern. | Brand damage, stakeholder pressure, market value risk and board escalation. | Board / Communications |

Seven Non-Readiness Risks CFOs Should Track

1. Documentation Gaps

Missing, outdated or incomplete records across suppliers, products, inputs or subcontractors.

2. Traceability Weakness

Inability to prove origin, custody, movement, subcontracting or processing history.

3. Data Methodology Failure

ESG, emissions, product or land-use data based on unclear assumptions or unsupported estimates.

4. Contractual Weakness

Supplier contracts lacking evidence obligations, audit rights, update cycles or remediation cost allocation.

5. Single-Source Dependency

Critical suppliers cannot be replaced quickly if evidence failure creates buyer, customs or regulatory friction.

6. Governance Gaps

No owner, no refresh cycle, no gap register and no escalation process for supplier evidence.

7. Financing Readiness Gap

Evidence is not structured for lender review, investor diligence or sustainability-linked credit discussions.

8. Customer Response Delay

The company cannot answer buyer questionnaires or due diligence requests within commercially acceptable timelines.

CFO Formula for Hidden Supplier Cost

Supplier non-readiness should be priced before regulatory pressure forces the cost into the P&L.

Hidden Supplier Cost = Evidence Gap × Regulatory Exposure × Remediation Cost × Business Criticality

This formula requires internal data. CFOs need supplier criticality, revenue exposure, margin contribution, buyer dependency, evidence maturity, replacement lead time, remediation cost and financing sensitivity.

Non-Readiness Premium = Delay Cost + Remediation Cost + Rework Cost + Commercial Loss + Financing Friction

If this premium is not measured, the supplier is not cheap. The cost is simply being deferred.

Board Questions That Expose Hidden Cost

- Which suppliers would create the highest cost if evidence requests failed?

- Which suppliers require emergency documentation work most often?

- What evidence has not been updated in the last 12 months?

- Can we prove origin, traceability and data methodology end-to-end?

- Do our contracts allocate costs for delays, remediation and evidence failure?

- How fast can we replace or dual-source critical suppliers?

- Are lenders and investors comfortable with our supply-chain evidence maturity?

- Where is non-readiness currently hidden inside departmental budgets?

Red Flags for CFOs and Boards

- Evidence requests take weeks to assemble.

- Suppliers rely only on declarations without supporting documents.

- No traceability exists beyond first-tier suppliers.

- Contracts do not allocate evidence failure costs.

- There is no gap register with owners and deadlines.

- Reporting data is estimated without clear methodology.

- Supplier remediation cost is not tracked by finance.

- There is no real-time view of supplier evidence maturity.

Decision Trigger for CFOs

Do not wait for non-readiness to become a visible cost.

Price the evidence gap, assign the owner, define the remediation path and protect the company before supplier weakness reaches the P&L.

The CFO’s role is to convert hidden supplier weakness into measurable exposure before it becomes margin leakage, delayed revenue or financing friction.

Villanova ESG Position

Villanova ESG helps companies identify, quantify and reduce the hidden cost of supplier non-readiness in Brazil-Europe supply chains.

The objective is not to promise compliance, guarantee legal certainty or eliminate risk. The objective is to structure regulatory evidence, supplier readiness controls and CFO-grade risk visibility so companies can reduce avoidable cost and strengthen defensibility.

In regulated supply chains, non-readiness is not neutral. It is deferred cost.

Regulatory Source Trail

- European Commission — Corporate Sustainability Due Diligence Directive: Directive 2024/1760 entered into force on 25 July 2024 and aims to foster responsible corporate behaviour across companies’ operations, subsidiaries and global value chains.

- European Commission — Carbon Border Adjustment Mechanism: CBAM is designed to confirm that a carbon price has been paid for embedded carbon emissions generated in the production of certain goods imported into the EU.

- European Commission — EUDR Information System: the Information System acts as the repository of due diligence statements submitted by operators and traders under the EUDR.

- European Commission — Corporate Sustainability Reporting: companies subject to CSRD report according to European Sustainability Reporting Standards.

Executive Review

Turn supplier non-readiness into measurable financial exposure.

Villanova ESG supports CFOs, Boards and procurement teams with supplier readiness diagnostics, regulatory evidence architecture and hidden-cost analysis for Brazil-Europe supply chains.

For private board-level briefings: contact@villanovaesg.com