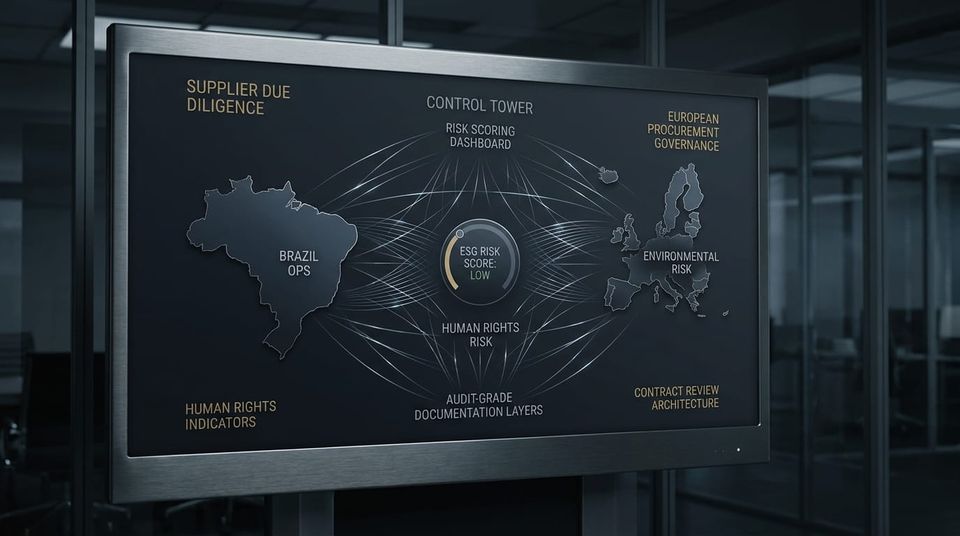

Supplier Due Diligence and Brazilian Operations: Why Procurement Becomes a Regulatory Control Point

Villanova ESG | Executive Regulatory Dossier

Supplier Due Diligence and Brazilian Operations: Why Procurement Becomes a Regulatory Control Point

Supplier due diligence changes the function of procurement. In European-facing value chains, supplier selection is no longer based only on price, delivery, capacity and commercial reliability. It increasingly depends on whether operational risk can be identified, documented, mitigated and defended.

Risk Vector

Supplier Controls

Procurement becomes a compliance checkpoint when buyers must evaluate environmental, human-rights, operational and documentation risks across suppliers.

Financial Exposure

Contract Continuity

Weak supplier evidence can affect onboarding, renewal, pricing power, audit burden, remediation cost and buyer confidence.

Board Relevance

Regulatory Defensibility

The board-level question is whether supplier decisions can be defended with evidence, not whether procurement followed a checklist.

The Strategic Change

Supplier due diligence is moving from a discretionary procurement practice to a regulatory and governance expectation. The European direction is clear: companies exposed to sustainability due diligence expectations need stronger visibility over risks in their operations, subsidiaries and business relationships. This affects how suppliers are selected, monitored and retained.

For Brazilian operations, the exposure is often indirect. A Brazilian supplier may not be directly subject to every European rule. But if its customer is a European company under due diligence pressure, procurement can become the channel through which regulation reaches the supplier. The supplier is then evaluated not only by what it sells, but by what it can prove.

Board-Level Interpretation

Supplier due diligence converts procurement into a regulatory control point. The supplier that cannot evidence risk management may become commercially weaker than the supplier with audit-grade documentation.

Why Brazilian Operations Are Exposed

Brazil is commercially relevant to European value chains across commodities, manufacturing, services, logistics, waste management, technology assets, industrial inputs and operational support. That relevance creates opportunity. It also creates documentation pressure. European buyers increasingly need suppliers that can support risk assessment with structured evidence.

The exposure is not limited to large exporters. It can reach second-tier and third-tier suppliers when their activity affects the buyer’s ability to document environmental, social, human-rights, traceability or operational risk. In this context, procurement becomes the transmission mechanism for regulatory expectations.

Brazilian Supplier Evidence Gap

- Supplier policies not connected to operational proof.

- Environmental records fragmented across vendors and facilities.

- Human-rights and labor-risk controls not documented in supplier files.

- Corrective actions recorded informally or without follow-up evidence.

- Procurement decisions based on price without documented risk scoring.

European Buyer Concern

- Can supplier risk be identified before contract signature?

- Can the supplier prove mitigation actions?

- Can documentation support internal and external review?

- Can procurement justify supplier retention under due diligence pressure?

- Can the buyer defend its supplier file if challenged by investors, regulators or auditors?

Finance-Grade Risk Formula

Supplier Due Diligence Exposure Model

Supplier Due Diligence Exposure = EU Customer Dependency × Supplier Risk Severity × Evidence Gap × Contract Replacement Probability

This is a board-level risk model, not a statutory formula. To quantify it, a company needs internal data: revenue by European customer, supplier-risk classification, documentation maturity, contract renewal dates, buyer due diligence requirements, audit history, remediation cost and substitution risk.

The CFO Problem: Procurement Risk Becomes Cash-Flow Risk

CFOs should not treat supplier due diligence as a compliance back-office function. The financial effect can be direct. A supplier that cannot satisfy due diligence expectations may face longer sales cycles, additional audits, buyer-imposed remediation, contract clauses, price discounts or lower renewal probability.

The risk appears before sanctions. It appears when procurement committees classify the supplier as administratively difficult, insufficiently documented or hard to defend. Once that label enters the buyer’s internal file, commercial exposure has already started.

CFO Diagnostic Question

If a European customer requested supplier due diligence evidence before contract renewal, could the company deliver a structured risk file — or only policies, certificates and disconnected operational records?

What a Supplier Due Diligence File Should Include

A supplier due diligence file should not be a collection of generic compliance documents. It should show how the company identifies risks, evaluates suppliers, documents decisions, monitors execution and escalates gaps. The file must be usable by procurement, legal, compliance, finance and board-level committees.

1. Supplier Risk Classification

Segmentation of suppliers by geography, activity, materiality, environmental exposure, labor-risk profile, data sensitivity and operational dependency.

2. Procurement Decision Trail

Evidence showing why a supplier was approved, what risks were identified, what controls were required and how the decision was documented.

3. Corrective Action Evidence

Records showing gap identification, remediation requests, deadlines, supplier responses, escalation logic and verification of implemented actions.

4. Contract and Renewal Risk Map

Mapping of contracts, renewal windows, critical customers, buyer due diligence clauses and financial exposure if the supplier file fails review.

Brazil-Europe Evidence Bridge

Where Ecobraz and Villanova ESG Fit

Ecobraz proves what happens in the Brazilian operation. Villanova ESG translates that proof into regulatory evidence European boards, CFOs, procurement and compliance teams can use.

In supplier due diligence, the value is not a generic ESG presentation. The value is a defensible procurement file. The objective is to reduce uncertainty before it becomes contract friction, audit escalation or supplier substitution.

Decision Trigger for CFOs

A CFO should trigger a supplier due diligence evidence review when at least one of the following conditions exists:

- The company supplies European customers or multinational groups with formal due diligence expectations.

- European buyers request supplier questionnaires, audits, corrective action plans or policy evidence.

- Procurement files are not connected to operational records and risk controls.

- Critical revenue depends on contract renewals with due diligence clauses.

- Supplier approval depends mainly on price, capacity and delivery without documented risk scoring.

- The company cannot produce a supplier evidence file within a short procurement review window.

Executive Position

In European-facing supply chains, procurement is becoming a risk gate. The supplier that can document due diligence discipline may become easier to approve, retain and defend.

Regulatory Source Trail

This dossier is based on official and institutional due diligence references. The analysis does not create legal advice and does not guarantee compliance outcomes. Company-specific risk assessment requires contract data, supplier records, buyer requirements, operational evidence, legal review and jurisdiction-specific analysis.

- European Commission — Corporate sustainability due diligence: official CSDDD page.

- European Commission — EU Due Diligence Navigator for partner countries: official CSDDD navigator page.

- OECD — Due Diligence Guidance for Responsible Business Conduct: official OECD guidance page.

Executive Review

Assess Supplier Due Diligence Evidence Before Procurement Becomes Contract Risk

Villanova ESG supports companies that need to translate Brazilian operational evidence into European-facing regulatory documentation. The objective is not generic sustainability communication. The objective is supplier-risk clarity, procurement defensibility and board-level evidence architecture.

For confidential executive reviews: contact@villanovaesg.com