EU Supply Chain Audit Readiness: Why Brazilian Suppliers Need Evidence Before the Audit Notice

Villanova ESG | Executive Regulatory Dossier

EU Supply Chain Audit Readiness: Why Brazilian Suppliers Need Evidence Before the Audit Notice

European buyer audits are not isolated compliance events. They are commercial tests of supplier defensibility. For Brazilian suppliers, the audit notice is not the beginning of preparation. It is the moment when evidence gaps become visible to procurement, legal, compliance and finance teams.

Risk Vector

Audit Evidence

Buyer audits test whether supplier claims can be supported by documents, process records, ownership, traceability and corrective action evidence.

Financial Exposure

Audit Cost

Weak audit readiness can increase legal review, evidence reconstruction, management escalation, remediation cost and renewal risk.

Board Relevance

Audit Defensibility

The board-level question is whether the company can survive buyer review without reconstructing evidence under deadline pressure.

The Strategic Change

European regulation is increasing buyer sensitivity to supply-chain evidence. CSDDD raises the relevance of due diligence over business relationships. CSRD increases demand for value-chain data. CBAM, EUDR, Scope 3 and product traceability frameworks increase pressure for specific operational records. Procurement teams respond through audits.

For Brazilian suppliers, this means audit readiness must be treated as a continuous governance discipline. The supplier should not wait for an audit notice to collect documents. At that point, the buyer has already identified a need for review. The supplier is already in a risk-test environment.

Board-Level Interpretation

Audit readiness is not the ability to answer under pressure. It is the ability to produce evidence immediately, consistently and defensibly before buyer confidence deteriorates.

Why Brazilian Suppliers Are Exposed

Brazilian suppliers often believe that an audit is a rare event. That assumption is becoming less reliable in European-facing value chains. Buyers under regulatory, reporting, lender or investor pressure may audit suppliers to verify claims, investigate inconsistencies, prepare contract renewal or support internal compliance files.

The exposure is operational and financial. If evidence is scattered, teams lose time. If answers conflict, legal risk rises. If documents cannot be connected to specific operations, the buyer may impose remediation. If the audit weakens supplier confidence, renewal terms may deteriorate.

Audit Readiness Gaps

- Documents stored across departments without a controlled index.

- Certificates not linked to operational records or chain-of-custody proof.

- Questionnaire answers not connected to evidence attachments.

- Corrective actions recorded informally without closure proof.

- Supplier files lacking ownership, version control or review history.

Buyer Audit Concerns

- Can the supplier prove each material claim?

- Can records be produced quickly and consistently?

- Can evidence be linked to the specific product, contract or operation?

- Can identified gaps be corrected and verified?

- Can the buyer rely on this supplier for future regulatory requests?

Finance-Grade Risk Formula

Audit Readiness Exposure Model

Audit Readiness Exposure = Audit Probability × Evidence Gap × Contract Value × Buyer Sensitivity

This is a management risk model, not a statutory formula. To quantify it, a company needs internal data: audit history, buyer requirements, contract value, renewal date, evidence maturity, questionnaire answers, corrective action backlog, internal response cost and remediation budget.

The CFO Problem: Audit Response Can Become a Cash-Flow Event

CFOs should not treat buyer audits as operational interruptions. They can become cash-flow events. The audit may trigger external advisory cost, legal review, supplier requalification, process correction, system upgrades, additional reporting obligations or contract repricing.

The more reactive the response, the higher the cost. If evidence must be reconstructed after the audit notice, teams operate under pressure. If evidence is already organized, the company can respond with speed, discipline and stronger negotiation posture.

CFO Diagnostic Question

If a European buyer issued an audit notice today, could the company produce a complete evidence file within 48 hours — or would finance, legal, ESG and operations begin reconstructing proof from scratch?

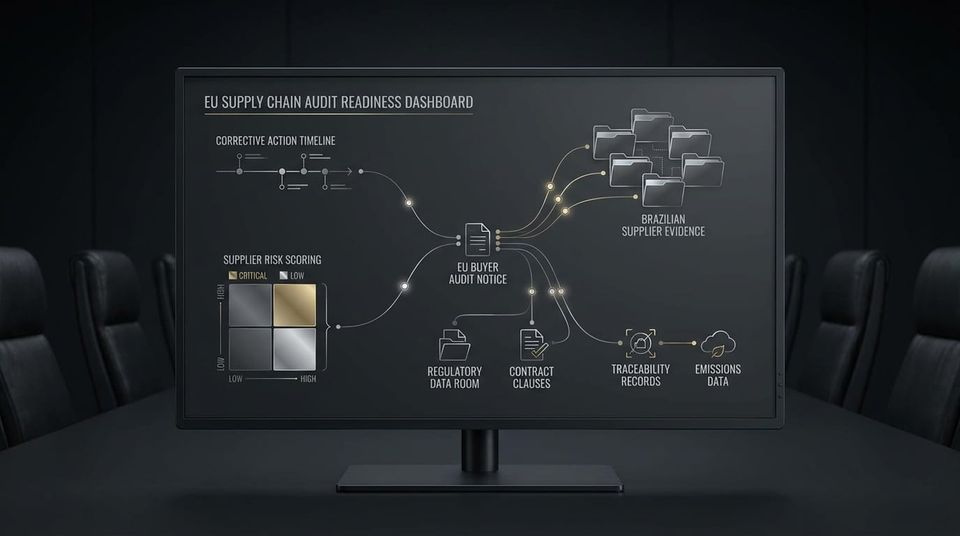

What an Audit-Ready Evidence File Should Include

Audit readiness is not a folder of certificates. It is a controlled file that connects claims, documents, process owners, timelines, corrective actions and financial exposure. It must be usable by procurement, legal, compliance, finance, operations and executive leadership.

1. Audit Evidence Index

Master list of documents mapped to buyer claims, regulatory themes, contracts, suppliers, products, operations and responsible owners.

2. Claim-to-Evidence Matrix

Direct linkage between each submitted answer, certificate, policy, emissions figure, traceability claim or due diligence statement and its evidence source.

3. Corrective Action Register

Record of findings, remediation owners, deadlines, evidence of closure, unresolved gaps, buyer communications and residual exposure.

4. Financial Exposure Summary

Executive view of contract value, renewal timing, audit cost, remediation cost, margin sensitivity and customer dependency.

CFO Audit Cost Model

Audit Response Cost

Audit Response Cost = Evidence Search + Validation + Legal Review + Management Escalation + Remediation + Buyer Reporting

This model should be applied by customer and audit theme. A recurring audit requirement from a high-revenue buyer may justify pre-investment in evidence architecture. A low-margin buyer with high audit burden may require price adjustment or contract renegotiation.

Brazil-Europe Evidence Bridge

Where Ecobraz and Villanova ESG Fit

Ecobraz proves what happens in the Brazilian operation. Villanova ESG translates that proof into regulatory evidence European boards, CFOs, procurement, legal and compliance teams can use.

In audit readiness, the value is not last-minute response. The value is pre-audit control. Brazilian operational proof becomes commercially stronger when it is organized before a European buyer tests it.

Decision Trigger for CFOs and Compliance Teams

An EU supply-chain audit readiness review should be triggered when at least one of the following conditions exists:

- European buyers include audit rights in contracts or renewal terms.

- Supplier questionnaires request evidence that has not been centrally validated.

- Corrective action plans exist but closure evidence is incomplete.

- Commercial teams submit claims without a claim-to-evidence matrix.

- Previous audits required urgent evidence reconstruction.

- The company cannot estimate audit response cost by customer or contract.

Executive Position

Audit readiness must precede audit pressure. The supplier that waits for the notice loses time, leverage and cost control. The supplier with a board-ready evidence file enters the audit with defensibility.

Regulatory Source Trail

This dossier is based on official and institutional due diligence and reporting references. The audit-readiness models presented here are executive financial models, not statutory formulas, legal opinions or assurance methodologies. Company-specific assessment requires buyer audit clauses, contracts, submitted questionnaires, operational records, supplier files, corrective action history, cost allocation and jurisdiction-specific review.

- European Commission — Corporate sustainability due diligence: official CSDDD page.

- European Commission — Corporate sustainability reporting: official CSRD and sustainability reporting page.

- OECD — Due Diligence Guidance for Responsible Business Conduct: official OECD guidance page.

Executive Review

Build Audit Readiness Before European Buyer Review Becomes Contract Pressure

Villanova ESG supports companies that need to translate Brazilian operational evidence into European-facing audit-ready documentation. The objective is not reactive audit response. The objective is evidence control, audit cost reduction, buyer-risk mitigation and board-level defensibility.

For confidential executive reviews: contact@villanovaesg.com