EU Buyer Questionnaires and Brazilian Suppliers: Why ESG Forms Become Financial Risk

Villanova ESG | Executive Regulatory Dossier

EU Buyer Questionnaires and Brazilian Suppliers: Why ESG Forms Become Financial Risk

European buyer questionnaires are often treated as administrative forms. That is a mistake. For Brazilian suppliers connected to EU-facing value chains, these questionnaires can become the first formal test of evidence maturity, supplier risk, reporting readiness and contract resilience.

Risk Vector

Supplier Disclosure

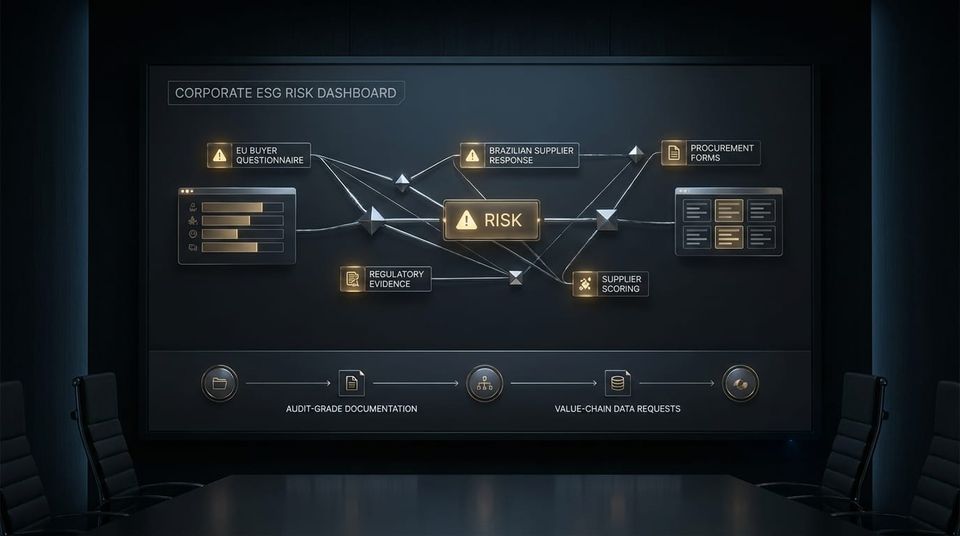

ESG questionnaires convert supplier claims into written records that buyers can use for procurement scoring, audit triggers and contractual escalation.

Financial Exposure

Procurement Scoring

Weak or inconsistent answers can reduce buyer confidence, increase audit cost, delay onboarding and weaken contract renewal probability.

Board Relevance

Evidence Consistency

The board-level question is whether answers submitted to buyers can be defended against the company’s actual evidence base.

The Strategic Change

European buyer questionnaires are becoming a transmission mechanism for regulatory pressure. They may ask about human rights, environmental controls, carbon data, traceability, supplier due diligence, waste handling, product information, data governance, audit rights and corrective action procedures. The form may look simple. The risk behind it is not.

When a Brazilian supplier answers a questionnaire, it creates a written representation. If that representation is not supported by records, the company exposes itself to procurement friction, credibility loss and future audit inconsistencies. The buyer may treat weak answers as risk signals. The supplier may treat them as paperwork. That mismatch is where financial exposure starts.

Board-Level Interpretation

Buyer questionnaires are not neutral forms. They are procurement risk instruments. Every answer should be treated as a claim that may need evidence, audit support and legal consistency.

Why Brazilian Suppliers Are Exposed

Brazilian suppliers often receive questionnaires from European customers without understanding the broader context. The form may be part of a supplier onboarding process. It may support CSRD value-chain data requests. It may reflect CSDDD-related due diligence pressure. It may prepare the buyer for internal risk scoring, audit prioritization, contract renewal or responsible sourcing review.

The exposure is not the questionnaire itself. The exposure is inconsistency. If commercial teams answer without legal, compliance, ESG, operations and finance alignment, the company may submit statements that exceed its actual evidence maturity. That can create a gap between what was claimed and what can be proven.

Questionnaire Risk Gap

- Commercial teams answer without evidence validation.

- Policies are declared but operational proof is incomplete.

- Carbon, waste, supplier or traceability data is estimated without methodology.

- Answers vary across customers because there is no controlled response library.

- Supporting records are not retained with the submitted questionnaire.

European Buyer Concern

- Can the supplier support each answer with evidence?

- Are responses consistent across procurement, ESG and legal files?

- Can high-risk answers trigger remediation?

- Can the buyer rely on the supplier’s data for reporting or due diligence?

- Should the supplier be audited before renewal or expansion?

Finance-Grade Risk Formula

Questionnaire Financial Exposure Model

Questionnaire Exposure = Customer Revenue Dependency × Response Materiality × Evidence Gap × Audit Trigger Probability

This is a board-level risk model, not a statutory formula. To quantify it, a company needs internal data: revenue by European customer, questionnaire frequency, high-risk topics, evidence maturity, audit history, renewal dates, buyer scoring criteria and remediation cost.

The CFO Problem: Forms Can Create Cash-Flow Exposure

CFOs should not treat ESG questionnaires as low-value paperwork. They can affect cash flow through procurement scoring, delayed onboarding, audit costs, customer retention, pricing pressure and remediation obligations. A poorly answered form can create a future cost that was invisible when the commercial team submitted it.

The risk is asymmetric. A supplier may answer quickly to protect a sale. The buyer may retain the answers as part of its formal due diligence file. If the answers are later tested and evidence is weak, the supplier’s credibility declines. That credibility loss can affect contract renewal and expansion.

CFO Diagnostic Question

Does the company retain evidence behind every ESG questionnaire answer submitted to European buyers — or does it rely on memory, good faith and scattered operational documents?

What a Questionnaire-Ready Evidence File Should Include

A questionnaire-ready evidence file should allow the company to answer buyer requests quickly without weakening legal, commercial or operational defensibility. The objective is not to slow down sales. The objective is to prevent sales teams from creating unsupported claims.

1. Controlled Response Library

Pre-approved answers for recurring buyer questions, validated by legal, compliance, operations, ESG and finance where material.

2. Evidence Attachment Map

Clear linkage between each answer and the documents that support it, including certificates, records, policies, logs, invoices, audits and corrective actions.

3. Risk Escalation Protocol

Internal rules defining when a questionnaire answer requires legal review, management approval, disclosure limitation or remediation before submission.

4. Submission and Retention Record

Version-controlled archive showing what was submitted, to whom, when, by whom and with which supporting evidence.

Brazil-Europe Evidence Bridge

Where Ecobraz and Villanova ESG Fit

Ecobraz proves what happens in the Brazilian operation. Villanova ESG translates that proof into regulatory evidence European boards, CFOs, procurement, legal and compliance teams can use.

In buyer questionnaires, the value is not fast form completion. The value is answer defensibility. The objective is to ensure that each response submitted to a European buyer is consistent with the company’s actual evidence base.

Decision Trigger for CFOs and Commercial Teams

A questionnaire evidence review should be triggered when at least one of the following conditions exists:

- A European buyer requests ESG, climate, human-rights, environmental, traceability or supplier due diligence information.

- Commercial teams answer buyer forms without legal or compliance validation.

- Different customers receive different answers to similar questions.

- Supporting evidence is not retained with the submitted questionnaire.

- Questionnaires include audit rights, contract clauses or corrective action commitments.

- The buyer uses supplier scoring, preferred-supplier programs or formal risk classification.

Executive Position

A buyer questionnaire is not a harmless form. It is a written risk position. The supplier that answers without evidence may be creating future audit exposure inside its own customer file.

Regulatory Source Trail

This dossier is based on official and institutional due diligence and reporting references. The analysis does not create legal advice and does not guarantee acceptance by buyers, auditors, lenders or regulators. Company-specific assessment requires buyer questionnaires, submitted responses, evidence files, contract clauses, customer exposure, legal review and jurisdiction-specific analysis.

- European Commission — Corporate sustainability due diligence: official CSDDD page.

- European Commission — Corporate sustainability reporting: official CSRD and sustainability reporting page.

- OECD — Due Diligence Guidance for Responsible Business Conduct: official OECD guidance page.

Executive Review

Assess Buyer Questionnaire Evidence Before ESG Forms Become Financial Risk

Villanova ESG supports companies that need to translate Brazilian operational evidence into European-facing regulatory and procurement documentation. The objective is not generic ESG response management. The objective is answer defensibility, buyer-risk reduction and board-level evidence architecture.

For confidential executive reviews: contact@villanovaesg.com