Audit-Grade Evidence and Brazilian Operations: Why Certificates Are Not Enough

Villanova ESG | Executive Regulatory Dossier

Audit-Grade Evidence and Brazilian Operations: Why Certificates Are Not Enough

Certificates can support a compliance file. They cannot replace it. For Brazilian operations connected to European buyers, the decisive question is whether documentation proves the operational chain, not whether the company can display isolated declarations, licenses, reports or certificates.

Risk Vector

Evidence Integrity

A certificate may confirm one status or event. Audit-grade evidence shows process, execution, traceability, control and accountability.

Financial Exposure

Buyer Confidence

Weak documentation can trigger audits, procurement delays, remediation requests, contract friction and credibility loss.

Board Relevance

Defensible File

The board-level question is whether the evidence file can be reviewed, challenged, reconstructed and defended.

The Strategic Change

European-facing regulatory pressure is changing the evidentiary standard expected from suppliers. Buyers no longer need only a document that says something happened. They need a file that shows how it happened, who executed it, what controls existed, what records support the claim and whether the process can be verified.

This distinction is critical. A certificate can be useful. But if it is disconnected from operational records, chain-of-custody data, supplier controls, risk assessment and corrective action evidence, it becomes a weak defense asset. It may satisfy a superficial checklist. It may fail a serious procurement, audit or regulatory review.

Board-Level Interpretation

Certificates are evidence fragments. Audit-grade documentation is an evidence architecture. The supplier that confuses the two may overestimate its regulatory defensibility.

Why Brazilian Operations Are Exposed

Brazilian suppliers often rely on certificates, licenses, invoices, disposal documents, environmental reports or internal declarations as proof of compliance. These documents matter. But European buyers increasingly need more than isolated proof points. They need to understand whether the supplier has a controlled process capable of supporting due diligence, reporting, traceability and procurement risk review.

The risk is highest when documents exist but cannot be connected. A certificate without traceability. A destination record without chain-of-custody. A policy without implementation evidence. A supplier declaration without verification. A spreadsheet without methodology. That fragmentation creates a false sense of readiness.

Certificate-Based Weakness

- Certificates stored without operational context.

- Documents not linked to lots, shipments, suppliers or service orders.

- Evidence issued after the event without process reconstruction.

- Records lacking responsible owner, date control or version control.

- Claims made in questionnaires that exceed the evidence available.

European Buyer Concern

- Can the supplier prove the process behind the certificate?

- Can evidence be connected to the specific product, service or operation?

- Can the buyer reconstruct the chain of custody?

- Can corrective actions be traced from finding to closure?

- Can the file survive legal, procurement, audit or regulator review?

Finance-Grade Risk Formula

Audit-Grade Evidence Exposure Model

Evidence Exposure = Revenue at Risk × Documentation Fragmentation × Process Criticality × Review Probability

This is a board-level risk model, not a statutory formula. To quantify it, a company needs internal data: European customer dependency, contract value, documentation maturity, certificate coverage, process criticality, audit frequency, buyer questionnaires, remediation cost and operational reconstruction capacity.

The CFO Problem: Certificates Can Hide Cost Exposure

CFOs should not treat certificates as proof that regulatory exposure is controlled. A certificate may reduce friction in a basic review. It may not protect margin, contract renewal or buyer confidence if deeper evidence is requested. The financial risk appears when the company discovers that its documentation cannot support what the sales, ESG or procurement team has already represented to the buyer.

The cost can appear through urgent evidence reconstruction, external consulting, legal review, operational remediation, supplier requalification, buyer audits, delayed payments, contract renegotiation or loss of preferred-supplier status. Weak documentation turns compliance into an unplanned cash-flow event.

CFO Diagnostic Question

If a European buyer challenged the evidence behind a certificate, could the company reconstruct the operational chain — or would it only resend the same certificate with no supporting file?

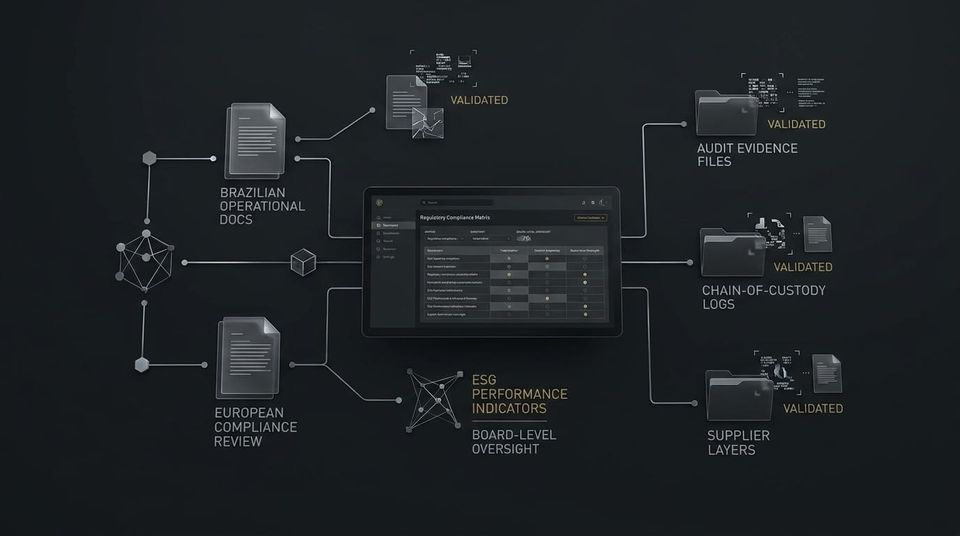

What Audit-Grade Evidence Should Include

Audit-grade evidence is not document volume. It is structured defensibility. The file must show connection, chronology, ownership, methodology and control. The objective is to make the evidence reviewable by procurement, legal, compliance, finance, auditors and board-level decision makers.

1. Process Chain

Documentation showing the sequence of events, operational responsibility, controls applied, records generated and final outcome.

2. Evidence Linkage

Clear connection between certificates, invoices, service orders, supplier records, transport documents, traceability data and operational logs.

3. Validation and Control Logic

Evidence of review, approval, version control, data ownership, corrective action tracking and exception management.

4. Buyer-Ready Narrative

Executive explanation translating operational records into a clear evidence file that European buyers can review without operational ambiguity.

Brazil-Europe Evidence Bridge

Where Ecobraz and Villanova ESG Fit

Ecobraz proves what happens in the Brazilian operation. Villanova ESG translates that proof into regulatory evidence European boards, CFOs, procurement, legal and compliance teams can use.

In audit-grade documentation, the value is not issuing one more certificate. The value is connecting operational proof into a defensible file. The objective is to reduce buyer uncertainty before documentation gaps become contract friction, audit escalation or board-level exposure.

Decision Trigger for CFOs and Compliance Teams

An audit-grade evidence review should be triggered when at least one of the following conditions exists:

- The company relies on certificates to answer European buyer questionnaires.

- Certificates are not linked to chain-of-custody or operational records.

- Buyer contracts include audit rights, reporting duties or remediation obligations.

- European customers request traceability, supplier due diligence, emissions or waste evidence.

- Evidence is stored across departments without ownership, chronology or version control.

- The company cannot reconstruct what happened behind a compliance claim within a short review window.

Executive Position

A certificate is not a risk system. It is only one evidence point. The company that cannot connect certificates to operational proof may be documenting compliance without building defensibility.

Regulatory Source Trail

This dossier is based on official and institutional due diligence, reporting and traceability references. The analysis does not create legal, audit or assurance advice and does not guarantee acceptance by buyers, auditors, lenders or regulators. Company-specific assessment requires operational records, contracts, buyer questionnaires, certificates, chain-of-custody documents, supplier files and jurisdiction-specific review.

- European Commission — Corporate sustainability due diligence: official CSDDD page.

- European Commission — Corporate sustainability reporting: official CSRD and sustainability reporting page.

- European Commission — EUDR Information System: official due diligence statement system page.

Executive Review

Assess Audit-Grade Evidence Before Certificates Become a False Sense of Compliance

Villanova ESG supports companies that need to translate Brazilian operational evidence into European-facing regulatory and procurement documentation. The objective is not certificate collection. The objective is evidence architecture, buyer-risk reduction and board-level regulatory defensibility.

For confidential executive reviews: contact@villanovaesg.com