The Audit-Grade Mindset

Executive Dossier · Trust Engineering Series

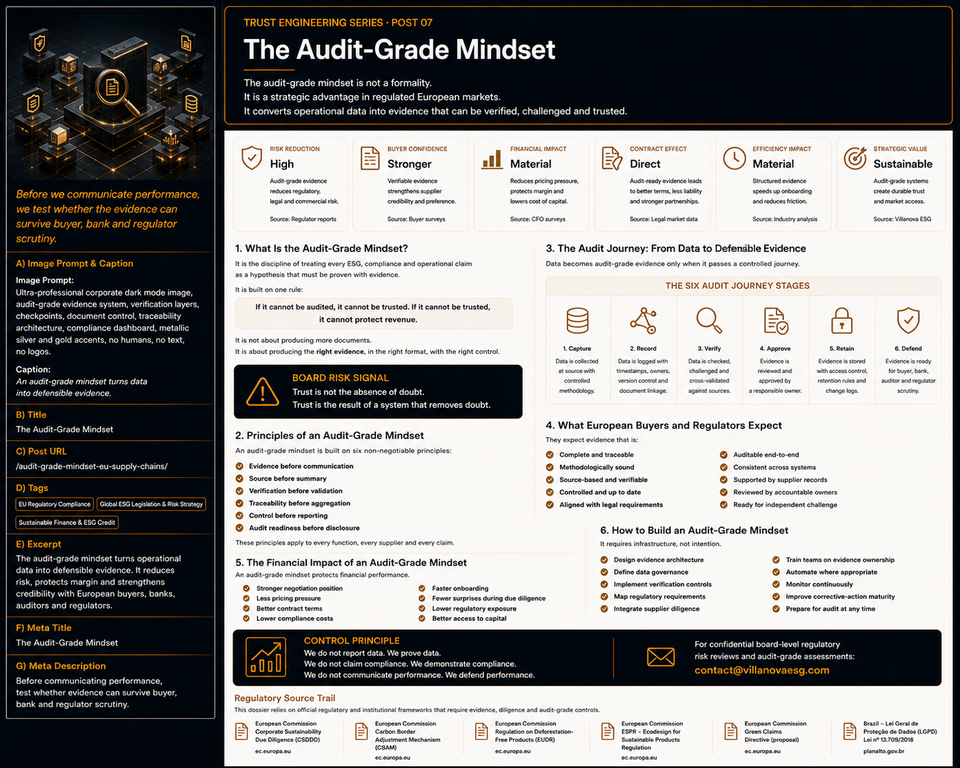

The audit-grade mindset is not a formality. It is a strategic advantage in regulated European markets. It converts operational data into evidence that can be verified, challenged and trusted.

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. Before a company communicates performance, it must test whether the evidence can survive buyer diligence, bank review, auditor scrutiny and regulator pressure.

Risk Reduction

Audit-grade evidence reduces regulatory, legal and commercial uncertainty.

Buyer Confidence

Verifiable evidence strengthens supplier credibility and preference.

Financial Impact

Strong proof protects margin, pricing power and cost-of-capital credibility.

Strategic Value

Audit-grade systems make trust repeatable, scalable and defensible.

What Is the Audit-Grade Mindset?

The audit-grade mindset is the discipline of treating every ESG, compliance and operational claim as a hypothesis that must be proven with evidence.

It is built on one rule:

If it cannot be audited, it cannot be trusted. If it cannot be trusted, it cannot protect revenue.

This mindset is not about producing more documents. It is about producing the right evidence, in the right format, with the right control.

Board Risk Signal

Trust is not the absence of doubt. Trust is the result of a system that removes doubt.

Principles of an Audit-Grade Mindset

An audit-grade mindset is built on six non-negotiable principles:

- Evidence before communication: no claim should be published, sold or negotiated before the evidence is tested.

- Source before summary: every number, statement or declaration must trace back to a controlled source.

- Verification before validation: supplier declarations, emissions data and compliance records must be checked before being accepted.

- Traceability before aggregation: aggregated ESG data is weak if the underlying records cannot be traced.

- Control before reporting: reporting without access control, ownership and version control creates exposure.

- Audit readiness before disclosure: if evidence cannot survive challenge, disclosure increases risk.

Audit-Grade Evidence Formula

Defensible Evidence = Source Integrity × Traceability × Verification × Governance Control × Audit Readiness

This formula requires internal company data. A real assessment depends on source records, supplier evidence, emissions methodology, data ownership, version control, approval logs, retention rules and audit history.

The Audit Journey: From Data to Defensible Evidence

Data becomes audit-grade evidence only when it passes through a controlled journey. Raw data alone is not enough. A spreadsheet is not a control system. A supplier declaration is not verification. A report is not proof.

Six Audit Journey Stages

Capture

Data is collected at source with methodology, context and ownership defined from the beginning.

Record

Information is logged with timestamps, owners, version control and linkage to documents or systems.

Verify

Data is checked, challenged and cross-validated against supplier records, operational evidence or approved methods.

Approve

Evidence is reviewed and approved by a responsible owner before use in reporting, contracts or buyer communication.

Retain

Evidence is stored with access control, retention rules, change logs and retrieval capacity.

Defend

The company can explain, prove and defend the evidence under buyer, bank, auditor or regulator scrutiny.

What European Buyers and Regulators Expect

European buyers and regulators do not expect perfection. They expect controlled evidence.

They expect evidence that is:

- complete and traceable;

- methodologically sound;

- source-based and verifiable;

- controlled and up to date;

- aligned with legal requirements;

- auditable end-to-end;

- consistent across systems;

- supported by supplier records;

- reviewed by accountable owners;

- ready for independent challenge.

The Financial Impact of an Audit-Grade Mindset

An audit-grade mindset protects financial performance because it reduces uncertainty.

When uncertainty falls, the company improves its position in buyer negotiations, lender conversations and Board-level risk reviews.

The financial impact appears as:

- stronger negotiation position;

- less pricing pressure;

- better contract terms;

- lower compliance response costs;

- faster onboarding;

- fewer surprises during due diligence;

- lower regulatory exposure;

- better access to capital conversations.

Control Principle

We do not report data. We prove data. We do not claim compliance. We demonstrate compliance. We do not communicate performance. We defend performance.

Decision Trigger for CFOs

The CFO should act when the company’s ESG, supplier or compliance evidence cannot be tested quickly under buyer pressure.

An audit-grade review becomes urgent when:

- key data exists but cannot be traced to source records;

- supplier declarations are accepted without verification;

- emissions, product or due-diligence data lacks methodology;

- evidence is dispersed across spreadsheets, emails and external consultants;

- commercial teams face recurring buyer requests for clarification;

- the Board cannot determine whether reported performance would survive independent review.

The Villanova ESG Audit-Grade Framework

Villanova ESG operates at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains.

The role is not to produce more reporting. The role is to make the company’s evidence defensible.

The framework includes:

- Evidence maturity diagnosis: assess whether operational, supplier, emissions and ESG data can survive scrutiny.

- Source-record mapping: trace every material claim back to documents, systems, owners and methodologies.

- Verification architecture: build checks, approvals, validations and challenge procedures before disclosure.

- Supplier evidence control: replace passive supplier declarations with active diligence and monitoring.

- Audit-readiness dashboard: translate evidence gaps into contract risk, buyer friction, margin exposure and market-access vulnerability.

- Board-level reporting: give leadership a clear view of what can be defended, what must be remediated and what should not be claimed.

Regulatory Source Trail

This dossier relies on official regulatory and institutional frameworks that require evidence, diligence and audit-grade controls:

- European Commission — Corporate Sustainability Due Diligence

- European Commission — Corporate Sustainability Reporting

- European Commission — Consultation on Revised European Sustainability Reporting Standards

- European Commission — Carbon Border Adjustment Mechanism

- European Commission — Green Claims

Closing CTA · Build Audit-Grade Trust

Before performance is communicated, evidence must be tested.

EU-facing companies cannot rely on claims that collapse under buyer, bank, auditor or regulator scrutiny. Audit-grade evidence converts operational reality into defensible trust and protects contracts, margin and market access.

Schedule a confidential audit-grade evidence review with our advisory team at contact@villanovaesg.com.