Engineering Discipline Beats ESG Storytelling

Executive Dossier · Trust Engineering Series

Sustainability narratives can attract attention. Engineering discipline, data integrity and audit-grade evidence are what protect margin, contracts and market access.

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. In regulated European markets, ESG storytelling is not a control system. It cannot prove supplier discipline, emissions integrity, traceability, due diligence or legal defensibility. Systems do.

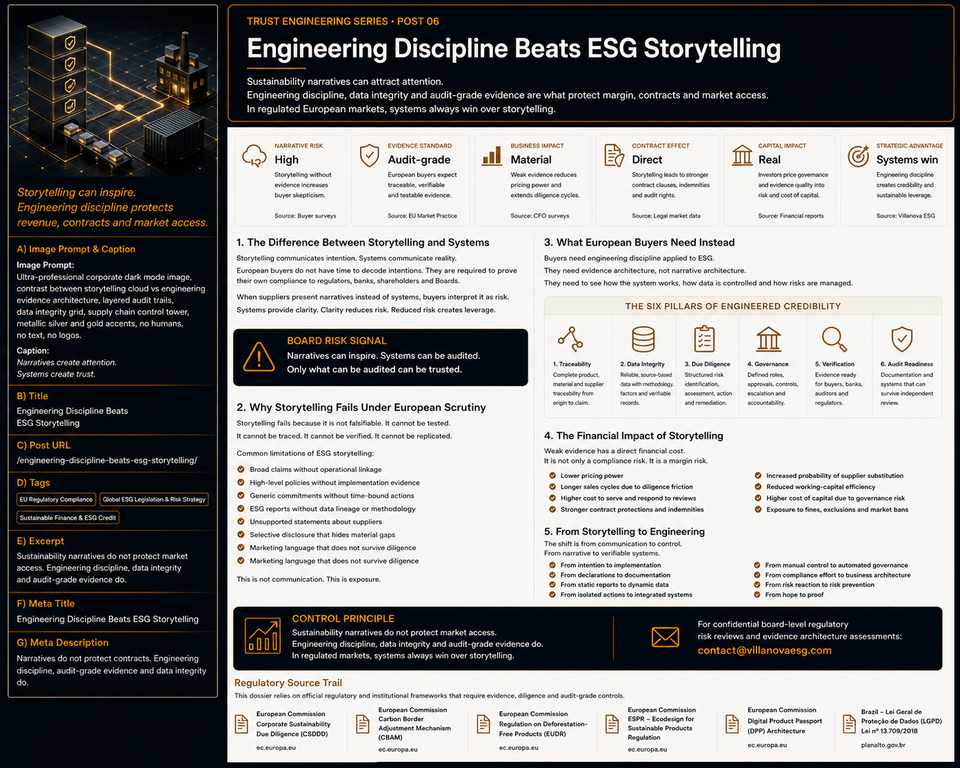

Narrative Risk

Storytelling without evidence increases buyer skepticism.

Evidence Standard

European buyers expect traceable, verifiable and testable evidence.

Business Impact

Weak evidence reduces pricing power and extends diligence cycles.

Strategic Advantage

Engineering discipline creates credibility and sustainable leverage.

The Difference Between Storytelling and Systems

Storytelling communicates intention. Systems communicate reality.

European buyers do not have time to decode intention. They are required to prove their own compliance to regulators, banks, shareholders and Boards. When suppliers present narratives instead of systems, buyers interpret it as risk.

Systems provide clarity. Clarity reduces risk. Reduced risk creates leverage.

Board Risk Signal

Narratives can inspire. Systems can be audited. Only what can be audited can be trusted.

Why Storytelling Fails Under European Scrutiny

Storytelling fails because it is not falsifiable. It cannot be tested. It cannot be traced. It cannot be verified. It cannot be replicated.

That creates exposure when buyers ask basic control questions:

- What evidence supports this claim?

- Which supplier generated the data?

- Which methodology was used?

- Who approved the record?

- Can the information be audited?

- Can corrective actions be verified?

- Can the data survive a regulator or buyer challenge?

If the answer depends on explanation instead of evidence, the claim is weak.

Engineering Discipline Formula

Regulatory Credibility = System Design × Data Integrity × Evidence Traceability × Verification Readiness × Governance Control

This formula requires internal company data. Real credibility depends on process maps, system controls, source records, supplier evidence, audit trails, access rules, corrective-action logs and Board-level accountability.

What European Buyers Need Instead

Buyers need engineering discipline applied to ESG.

They need to see how the system works, how data is controlled and how risks are managed. They need evidence that does not collapse under scrutiny.

Six Pillars of Engineered Credibility

Traceability

Complete product, material and supplier traceability from origin to buyer-facing claim.

Data Integrity

Reliable, source-based data with methodology, factors, owners, timestamps and verification records.

Due Diligence

Structured risk identification, assessment, prevention, mitigation, remediation and monitoring.

Governance

Defined roles, approvals, controls, escalation paths, access rules and Board accountability.

Verification

Evidence ready for buyers, banks, auditors, investors and regulators to test independently.

Audit Readiness

Documentation and systems that can survive internal review, external diligence and enforcement scrutiny.

The Financial Impact of Storytelling

Weak evidence has a direct financial cost. It is not only a compliance risk. It is a margin risk.

When companies rely on narrative instead of systems, the commercial damage appears as:

- lower pricing power;

- longer sales cycles due to diligence friction;

- higher cost to serve and respond to reviews;

- stronger contract protections and indemnities;

- increased probability of supplier substitution;

- reduced working-capital efficiency;

- higher cost of capital due to governance risk;

- exposure to fines, exclusions and market bans where applicable.

Control Principle

Sustainability narratives do not protect market access. Engineering discipline, data integrity and audit-grade evidence do.

From Storytelling to Engineering

The shift is from communication to control.

That means moving from:

- narrative to verifiable systems;

- intention to implementation;

- declarations to documentation;

- static reports to dynamic data;

- manual control to automated governance;

- compliance effort to business architecture;

- risk reaction to risk prevention;

- hope to proof.

This is how ESG becomes financially relevant. Not as messaging. As operating infrastructure.

Decision Trigger for CFOs

The CFO should act when the company’s ESG position depends more on communication than on verifiable systems.

An engineering-discipline review becomes urgent when:

- ESG claims are stronger than the evidence supporting them;

- supplier data cannot be traced to source records;

- emissions data lacks methodology, factors or verification;

- due diligence is described but not documented through controls;

- commercial teams face repeated buyer skepticism;

- the Board cannot connect sustainability claims to risk reduction, margin protection or capital credibility.

The Villanova ESG Engineering Discipline Framework

Villanova ESG operates at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains.

The role is not to improve ESG storytelling. The role is to replace fragile narratives with evidence architecture.

The framework includes:

- Storytelling-risk diagnosis: identify claims, reports and market messages unsupported by audit-grade evidence.

- System design review: assess whether the company has documented processes, controls and accountable owners behind each claim.

- Evidence architecture: organize product, supplier, emissions, due-diligence and governance data into a reviewable structure.

- Data integrity controls: define methodology, source records, timestamps, version control and access governance.

- Buyer-readiness assessment: test whether evidence can survive European diligence and contract negotiation.

- Board dashboard: translate weak narrative exposure into margin risk, contract risk, market-access risk and cost-of-capital implications.

Regulatory Source Trail

This dossier relies on official regulatory and institutional frameworks that require evidence, diligence and audit-grade controls:

- European Commission — Corporate Sustainability Due Diligence

- European Commission — Carbon Border Adjustment Mechanism

- European Commission — Green Claims

- European Commission — Implementing the Ecodesign for Sustainable Products Regulation

- European Commission — EU Due Diligence Navigator: CSDDD

Closing CTA · Replace Narrative with Evidence Architecture

In regulated markets, systems always win over storytelling.

EU-facing companies cannot protect contracts, margins or market access with ESG narratives alone. They need engineering discipline, data integrity, traceability, governance and audit-grade evidence capable of surviving buyer and regulator scrutiny.

Schedule a confidential engineering-discipline and evidence architecture review with our advisory team at contact@villanovaesg.com.