Why Boards Should Ask for Evidence Before Asking for ESG Claims

Board Risk Memo

Why Boards Should Ask for Evidence Before Asking for ESG Claims

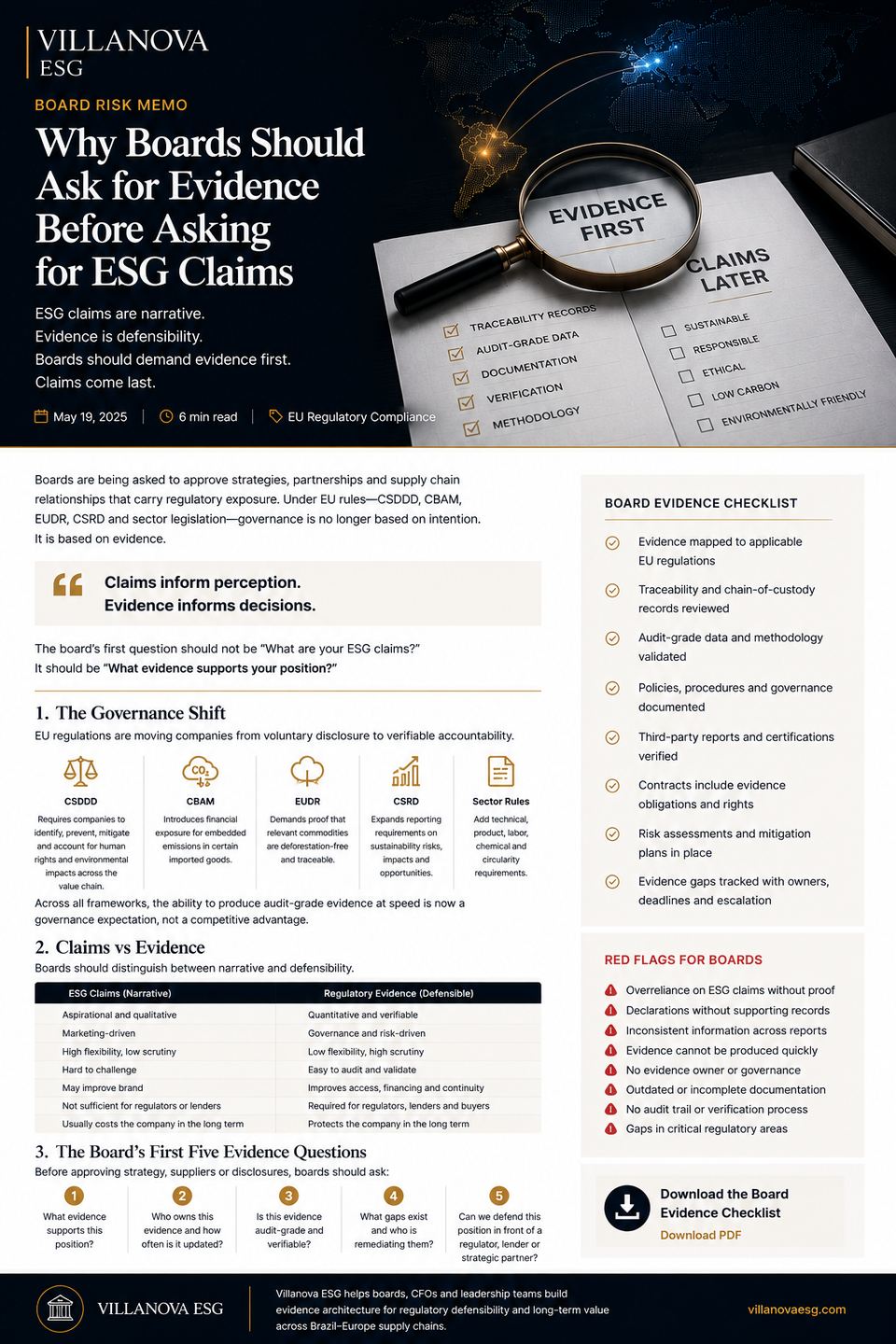

ESG claims are narrative. Regulatory evidence is defensibility. Boards should demand evidence before approving strategies, supplier relationships, disclosures or sustainability-linked positioning.

Board Lens

Evidence First

Risk Variable

Claim Defensibility

CFO Exposure

Reputation + Capital

Executive Thesis

Boards are often asked to approve ESG strategies, supplier programs, sustainability disclosures, financing narratives and stakeholder statements.

The wrong first question is: What is our ESG claim?

The right first question is: What evidence supports this position?

Claims inform perception. Evidence informs decisions.

In Brazil-Europe supply chains, a board that approves claims without evidence may be approving unpriced exposure. The risk may appear later in regulatory scrutiny, buyer questionnaires, lender review, investor diligence, supplier disruption or reputational damage.

The Governance Shift

EU regulation is moving corporate sustainability away from voluntary narrative and toward governance, traceability and accountability. The Corporate Sustainability Due Diligence Directive entered into force on 25 July 2024 and aims to foster responsible corporate behaviour across companies’ operations and global value chains, with companies in scope identifying and addressing adverse human rights and environmental impacts.

CSRD also reinforces the evidence discipline. Companies subject to the directive must report according to European Sustainability Reporting Standards, which increases the importance of documented sustainability risks, impacts and opportunities.

CBAM adds a financial and data layer for covered imports by confirming whether a carbon price has been paid for embedded emissions generated in the production of certain goods imported into the EU.

OECD responsible business conduct guidance is also explicit on risk-based due diligence. It calls for companies to assess and address real and potential negative impacts in operations, supply chains and business relationships.

ESG Claims vs. Regulatory Evidence

Boards must distinguish between statements that support reputation and evidence that supports defensibility.

| ESG Claim | Regulatory Evidence |

|---|---|

| A statement about commitment, ambition or values. | A document, dataset or record that supports a specific position. |

| Often produced for communication. | Produced for review, audit, due diligence or governance control. |

| May be broad, aspirational or qualitative. | Should be specific, current, traceable and internally consistent. |

| May help positioning. | Helps defend decisions, disclosures and supplier continuity. |

| Can create exposure if unsupported. | Can reduce exposure if complete, relevant and verifiable. |

The Board’s First Five Evidence Questions

1. What Evidence Supports the Claim?

Every ESG position should map to documents, data, operational records, supplier files or verified methodologies.

2. Who Owns the Evidence?

Evidence without an owner becomes stale. Boards should require accountability for validity, updates and response readiness.

3. Is the Evidence Audit-Grade?

Documents must be current, consistent, traceable, reviewable and connected to the claim being made.

4. What Gaps Exist?

Weak, expired, incomplete, estimated or unverifiable evidence should be tracked with owner, deadline and remediation priority.

5. Can We Defend This Externally?

The board should assume the claim may be reviewed by a buyer, lender, investor, auditor, regulator or strategic partner.

6. What Is the Cost of Being Wrong?

Unsupported claims can create remediation cost, reputational loss, buyer friction, financing risk or supplier continuity exposure.

CFO Formula for Claim Exposure

Unsupported ESG claims should be treated as financial exposure, not communication risk alone.

Claim Exposure = Claim Visibility × Evidence Gap × Stakeholder Scrutiny × Remediation Cost

This model requires internal company data. Inputs should include claim visibility, buyer dependency, reporting relevance, lender scrutiny, regulatory exposure, evidence maturity, remediation capacity and reputational sensitivity.

Board Defensibility Score = Evidence Quality + Traceability + Governance Ownership − Evidence Gap

If the company cannot calculate evidence quality or identify the evidence owner, the board should not approve the claim as defensible.

Red Flags for Boards

- ESG claims are approved before evidence is reviewed.

- Supplier claims are accepted without traceability records.

- Data methodology is unclear, estimated or not documented.

- Evidence is scattered across departments, emails and supplier portals.

- No executive owns evidence quality or update cycles.

- Claims appear in investor, lender or customer materials without defensibility review.

- There is no evidence gap register or remediation plan.

- Legal, finance, procurement and sustainability teams rely on different versions of the same claim.

What Boards Should Require Before Approval

- Evidence map: each material claim connected to supporting documentation.

- Evidence owner: accountable person or function responsible for validity and updates.

- Methodology note: explanation of how data was produced, estimated, verified or sourced.

- Supplier evidence file: when claims depend on value-chain information.

- Gap register: unresolved issues, risk rating, owner, deadline and remediation path.

- External review scenario: how the company would respond to buyer, lender, auditor, investor or regulator requests.

Decision Trigger for Boards

Do not approve the claim until the evidence can defend it.

Evidence should precede the narrative, the disclosure, the supplier commitment and the financing signal.

The board’s role is not to write ESG language. The board’s role is to ensure that material ESG positions are supported by disciplined, reviewable and defensible evidence.

Villanova ESG Position

Villanova ESG helps companies move from ESG claims to regulatory evidence architecture.

The objective is not to create sustainability narratives, guarantee legal certainty or promise compliance. The objective is to structure evidence so CFOs, Boards, procurement, legal and compliance teams can defend decisions under buyer, lender, investor and regulatory scrutiny.

In executive governance, claims may create attention. Evidence creates defensibility.

Regulatory Source Trail

- European Commission — Corporate Sustainability Due Diligence Directive: Directive 2024/1760 entered into force on 25 July 2024 and aims to foster responsible corporate behaviour across operations and global value chains.

- European Commission — Corporate Sustainability Reporting: companies subject to CSRD must report according to European Sustainability Reporting Standards.

- European Commission — Carbon Border Adjustment Mechanism: CBAM is designed to confirm that a carbon price has been paid for embedded emissions generated in the production of certain goods imported into the EU.

- OECD — Due Diligence for Responsible Business Conduct: risk-based due diligence helps companies assess and address real and potential negative impacts in operations, supply chains and business relationships.

Executive Review

Replace ESG claims with evidence architecture.

Villanova ESG supports Boards, CFOs and leadership teams with regulatory evidence architecture, supplier documentation frameworks and Brazil-Europe due diligence defensibility.

For private board-level briefings: contact@villanovaesg.com