No Evidence. No Leverage.

Executive Dossier · Trust Engineering Series

No evidence. No leverage. In European supply chains, evidence is not a supporting document. It is the currency of trust, the engine of negotiation power and the foundation of market access.

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. For EU-facing companies, the financial danger is not only non-compliance. It is entering negotiations without the proof required to defend price, reduce buyer uncertainty and protect contractual position.

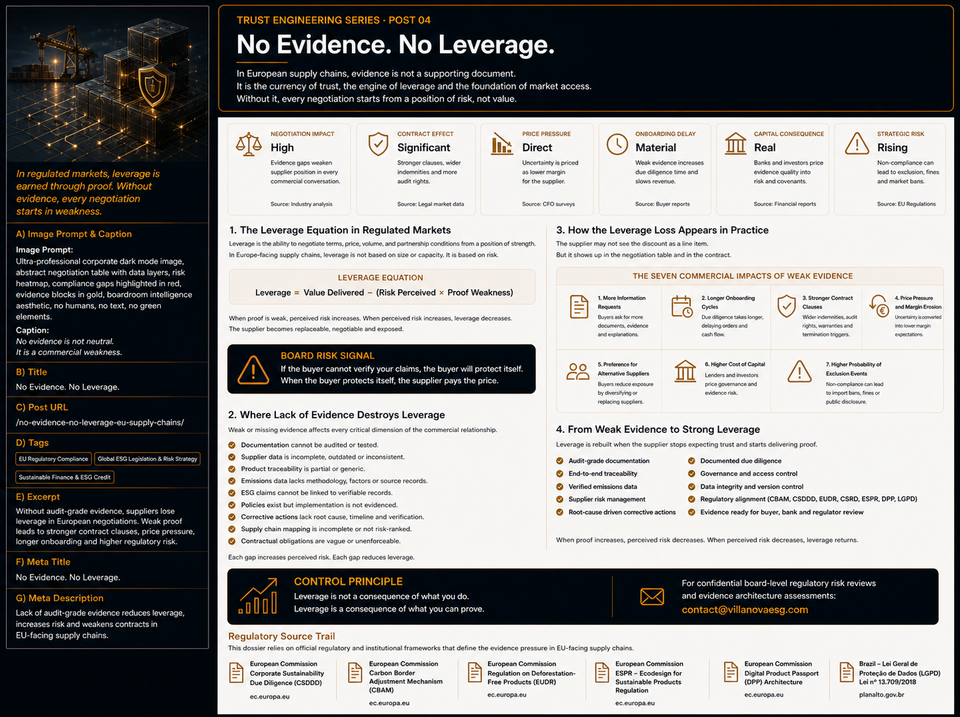

Negotiation Impact

Evidence gaps weaken supplier position before negotiation begins.

Contract Effect

Weak proof creates stronger clauses, wider indemnities and audit rights.

Price Pressure

Uncertainty is priced as lower margin for the supplier.

Strategic Risk

Non-compliance exposure can lead to exclusion, fines or market bans.

The Leverage Equation in Regulated Markets

Leverage is the ability to negotiate terms, price, volume and partnership conditions from a position of strength.

In EU-facing supply chains, leverage is not based only on size, capacity, quality or delivery history. It is based on risk.

If the buyer sees risk, the buyer protects itself. If the supplier cannot reduce that risk with evidence, the supplier pays through margin, contract terms and commercial friction.

Board Risk Signal

If the buyer cannot verify your claims, the buyer will protect itself. When the buyer protects itself, the supplier pays the price.

Where Lack of Evidence Destroys Leverage

Weak or missing evidence affects every critical dimension of the commercial relationship.

The most damaging evidence gaps include:

- documentation that cannot be audited or tested;

- supplier data that is incomplete, outdated or inconsistent;

- product traceability that is partial or generic;

- emissions data lacking methodology, factors or source records;

- ESG claims not linked to verifiable records;

- policies without evidence of implementation;

- corrective actions without root cause, timeline and verification;

- supply-chain mapping that is incomplete or not risk-ranked;

- contractual obligations that are vague or unenforceable.

Each gap increases perceived risk. Each perceived risk reduces leverage.

Leverage Equation

Commercial Leverage = Value Delivered − Regulatory Risk − Evidence Weakness − Buyer Liability Exposure

This equation requires internal company data. A real leverage assessment must evaluate buyer dependency, product criticality, evidence maturity, supplier risk, applicable EU frameworks, contract terms and financial exposure.

How Leverage Loss Appears in Practice

The supplier may not see the discount as a line item. But it appears inside the negotiation table and the contract.

Weak evidence creates measurable commercial consequences:

- more information requests from buyers;

- longer onboarding cycles and delayed sales;

- stronger contractual clauses and audit rights;

- wider warranties and indemnities;

- price pressure and margin erosion;

- preference for alternative suppliers with stronger documentation;

- higher probability of exclusion from strategic accounts;

- increased scrutiny from banks, investors and insurers.

Seven Commercial Impacts of Weak Evidence

More Information Requests

Buyers ask for more documents, explanations and supplementary evidence to compensate for uncertainty.

Longer Onboarding Cycles

Due diligence takes longer, delaying orders, approvals and cash-flow conversion.

Stronger Contract Clauses

Wider indemnities, audit rights, warranties and termination triggers are used to shift risk upstream.

Price Pressure

Uncertainty is converted into lower price expectations, rebate demands or margin compression.

Alternative Supplier Preference

Buyers reduce exposure by choosing suppliers with clearer evidence and lower perceived compliance risk.

Higher Cost of Capital

Banks and investors may price governance and evidence weakness into risk reviews, covenants or diligence intensity.

Market-Access Exposure

Evidence gaps can become obstacles under CBAM, CSDDD, EUDR, forced-labour regulation, CSRD or DPP pressure.

From Weak Evidence to Strong Leverage

Leverage is rebuilt when the supplier stops expecting trust and starts delivering proof.

Strong leverage requires:

- audit-grade documentation;

- end-to-end traceability;

- verified emissions data;

- supplier risk management;

- documented due diligence;

- governance and access control;

- data integrity and version control;

- regulatory alignment across CBAM, CSDDD, EUDR, CSRD, ESPR, DPP and LGPD;

- evidence ready for buyer, bank and regulator review.

When proof increases, perceived risk decreases. When perceived risk decreases, leverage returns.

Control Principle

Leverage is not a consequence of what you do. Leverage is a consequence of what you can prove.

Decision Trigger for CFOs

The CFO should act when commercial teams face buyer resistance but cannot isolate whether the problem is price, product or proof.

A leverage-risk review becomes urgent when:

- buyers request repeated clarifications before contract signature;

- sales cycles are slowing due to due-diligence friction;

- contracts include expanding warranties, indemnities or audit rights;

- pricing pressure is justified by compliance uncertainty;

- supplier, emissions or traceability data cannot be tested quickly;

- the company cannot quantify how evidence weakness affects margin and market access.

The Villanova ESG Leverage Recovery Framework

Villanova ESG works at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains.

The role is not to create more compliance documents. The role is to convert evidence into commercial leverage.

The framework includes:

- Leverage-risk diagnosis: identify where weak evidence is reducing pricing power, buyer confidence or contract strength.

- Evidence gap mapping: locate missing documentation across product, supplier, emissions, human-rights, deforestation and data-governance controls.

- Buyer-pressure analysis: assess which EU frameworks are driving diligence demands and contract protections.

- Contract exposure review: evaluate warranties, indemnities, audit rights, termination triggers and risk-shifting clauses.

- Proof architecture: structure evidence so it can be reviewed by buyers, banks, auditors and regulators.

- Board dashboard: translate evidence weakness into margin impact, contract risk, onboarding delay and revenue exposure.

Regulatory Source Trail

This dossier relies on official regulatory and institutional frameworks that define the evidence pressure in EU-facing supply chains:

- European Commission — Corporate Sustainability Due Diligence

- European Commission — Carbon Border Adjustment Mechanism

- European Commission — EUDR Information System and Due Diligence Statements

- European Commission — Implementing the Ecodesign for Sustainable Products Regulation

- Brazilian Federal Government — Lei Geral de Proteção de Dados Pessoais, Lei nº 13.709/2018

Closing CTA · Recover Commercial Leverage

Without evidence, every negotiation starts from weakness.

EU-facing companies cannot protect price, contracts or market access with operational confidence alone. They need audit-grade evidence capable of reducing buyer uncertainty and converting compliance into negotiation power.

Schedule a confidential leverage-risk and evidence architecture review with our advisory team at contact@villanovaesg.com.