CSRD + LGPD Harmonization

Executive Dossier · CSRD + LGPD Harmonization

CSRD forces sustainability information into financial-grade reporting. LGPD forces personal data into legal-grade governance. For EU-Brazil supply chains, the risk is not only reporting failure. It is building ESG disclosure on top of uncontrolled data flows.

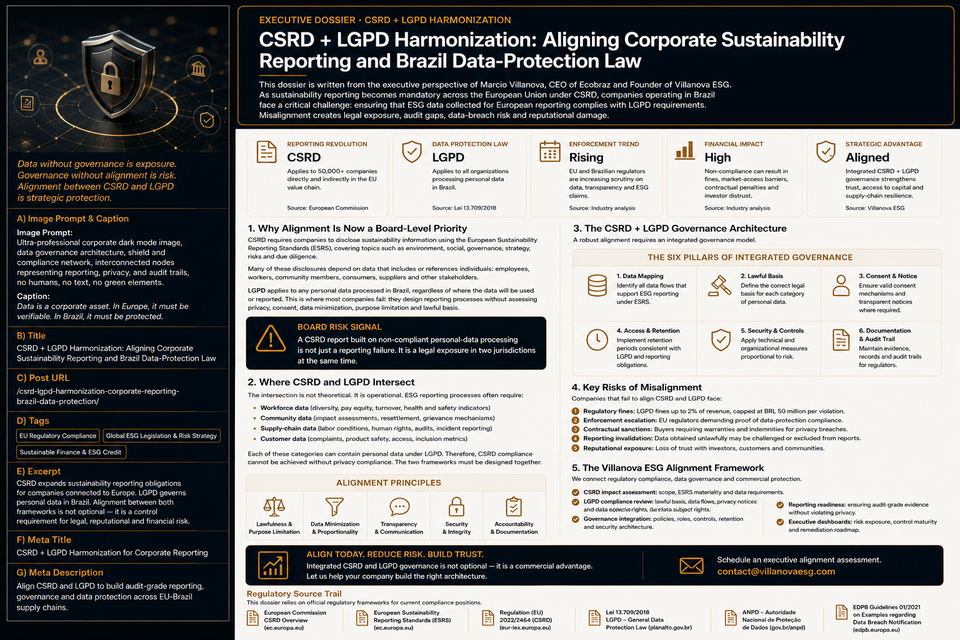

This dossier is written from the executive perspective of Marcio Villanova, CEO of Ecobraz and Founder of Villanova ESG. Sustainability reporting is becoming more auditable, more data-intensive and more dependent on supplier, workforce and operational evidence. In Brazil-connected chains, that evidence must be structured without violating privacy, access-control, retention or data-processing obligations under LGPD.

EU Reporting

CSRD requires reporting under European Sustainability Reporting Standards.

Brazilian Law

LGPD governs personal-data processing in Brazil.

Control Gap

ESG data may contain personal, supplier and operational evidence.

Board Risk

Disclosure without data governance creates dual exposure.

ESG Reporting Is Becoming a Data-Governance Problem

Corporate sustainability reporting is no longer a communication exercise. Under the European CSRD architecture, sustainability information moves closer to financial reporting, assurance logic and investor-grade comparability.

This creates a hidden problem for companies operating across Brazil and Europe. To report sustainability information, companies must collect, process, store, validate and disclose data from employees, suppliers, contractors, communities, facilities and operational systems.

Some of that information can include personal data, sensitive contextual data or records linked to identifiable individuals. That is where LGPD becomes financially relevant.

The Board-level issue is simple:

- CSRD increases demand for structured sustainability information.

- LGPD restricts how personal data can be processed, shared and retained.

- Supplier due diligence expands the volume of third-party evidence.

- Weak governance can create regulatory, audit and reputational exposure at the same time.

Board Risk Signal

A CSRD report built on uncontrolled personal-data processing is not a reporting achievement. It is legal exposure packaged as transparency.

Where CSRD and LGPD Collide

The intersection is not theoretical. It appears whenever ESG reporting requires evidence connected to people, suppliers, incidents, working conditions, health and safety, governance controls, grievance channels, training records or remediation processes.

These data points may support sustainability reporting. They may also trigger privacy obligations under Brazilian law when they involve personal data processed in Brazil or by Brazil-based entities.

The risk is not that companies should stop collecting ESG data. The risk is collecting it without lawful basis, clear purpose, access controls, retention rules, security governance and documentation.

Governance Exposure Formula

ESG Data Risk = Reporting Scope × Personal-Data Intensity × Supplier Complexity × Access Exposure × Control Weakness

This formula requires internal company data. A real risk score depends on data inventories, processing records, supplier maps, system access logs, retention policies, lawful-basis analysis and evidence-control maturity.

CSRD + LGPD Governance Map

Data Inventory

Identify which ESG data points contain personal, supplier, workforce, incident or community-related information.

Lawful Basis

Define the legal basis for each relevant processing activity before using data for reporting or assurance.

Purpose Limitation

Ensure ESG data collected for one purpose is not reused for reporting without legal and governance review.

Access Control

Limit access to ESG evidence according to role, sensitivity, reporting need and audit requirements.

Retention Discipline

Define how long ESG-related personal data is retained, archived, anonymized or deleted.

Audit Trail

Maintain records showing who collected, changed, validated, accessed and approved ESG data.

The Simplification Trap

European sustainability reporting and due-diligence requirements are currently subject to simplification and timing adjustments. That does not eliminate the strategic risk for companies connected to European value chains.

The trap is assuming that regulatory simplification equals evidence relaxation. It does not. Buyers, banks, auditors and investors will continue requesting reliable sustainability information because the underlying commercial need remains intact.

A company may fall outside a direct reporting wave and still face data requests from a European customer, lender, marketplace, investor or parent company. That is the operational reality for Brazil-linked supply chains.

Control Principle

Simplified reporting does not protect a company with uncontrolled ESG data. The market still demands evidence. LGPD still governs personal-data processing.

From Reporting Compliance to Data-Control Architecture

The correct approach is not to separate CSRD, LGPD, supplier due diligence and ESG reporting into disconnected workstreams. That creates duplication, legal blind spots and inconsistent evidence.

The correct approach is a unified data-control architecture. Sustainability information must be classified, governed, protected, validated and connected to reporting needs before it becomes a disclosure asset.

This is where Villanova ESG positions the work: at the intersection between European regulatory risk and cash-flow protection for cross-border supply chains. The objective is not to make reporting more complex. The objective is to reduce legal uncertainty, audit friction and buyer distrust.

Decision Trigger for CFOs

The CFO should intervene when ESG reporting begins to depend on data that legal, compliance, IT and procurement cannot jointly control.

A CSRD + LGPD harmonization review becomes urgent when:

- European buyers or investors request ESG data from Brazilian operations or suppliers.

- Sustainability teams collect workforce, supplier or incident data without formal privacy review.

- ESG reporting depends on spreadsheets, email attachments or external consultants without access-control records.

- The company cannot identify which ESG datasets contain personal data.

- Supplier data is transferred across borders without clear governance, purpose or documentation.

- The Board wants to avoid building CSRD readiness on top of LGPD exposure.

The Villanova ESG Alignment Framework

Villanova ESG treats CSRD + LGPD harmonization as a financial-risk control project. The purpose is to protect reporting credibility, legal defensibility and commercial trust.

The advisory framework includes:

- Reporting-scope assessment: identify direct and indirect CSRD relevance across EU-facing operations, buyers and corporate structures.

- ESG data inventory: map data sources, owners, systems, suppliers, personal-data categories and evidence flows.

- LGPD compliance review: assess lawful basis, purpose limitation, data minimization, retention, security and data-subject governance.

- Supplier data governance: define custody, transfer rules, documentation, access control and contract obligations.

- Audit-readiness architecture: build evidence trails that support reporting without creating privacy exposure.

- Board dashboard: translate data-governance gaps into legal risk, reporting risk, remediation cost and market-access exposure.

Regulatory Source Trail

This dossier relies on official regulatory frameworks verified for current compliance positions:

- European Commission — Corporate Sustainability Reporting

- Directive (EU) 2022/2464 — Corporate Sustainability Reporting Directive

- Directive (EU) 2026/470 — Amendments to CSRD and CSDDD Reporting Requirements

- Brazilian Federal Government — Lei nº 13.709/2018, Lei Geral de Proteção de Dados Pessoais

- ANPD — Brazilian Data Protection Law, English Version

Closing CTA · Secure Your ESG Data Governance

Sustainability reporting without data governance creates exposure in two jurisdictions.

EU-facing ESG disclosure requires evidence. Brazilian personal-data law requires control. Companies that fail to align both frameworks risk building reporting credibility on legally fragile data flows.

Schedule a CSRD + LGPD data-governance review with our advisory team to protect your cross-border reporting architecture at contact@villanovaesg.com.