Contract Clause Risk Review

EU-Brazil Supplier Evidence | Contract Risk

Contract Clause Risk Review

A focused executive review for companies that need to assess whether supplier evidence can support European buyer clauses on audit rights, reporting, traceability, origin, carbon data and due diligence cooperation.

Problem

Contract Clauses Are Becoming Evidence Tests

Supplier contracts increasingly include obligations that require evidence, not only acceptance of legal wording.

Commercial Risk

Signing Without Evidence

A supplier may accept a clause but still lack the documentation needed to support it under buyer review.

Response

Clause Evidence Review

Villanova ESG reviews whether supplier evidence can support the clauses before they become procurement, audit or contract friction.

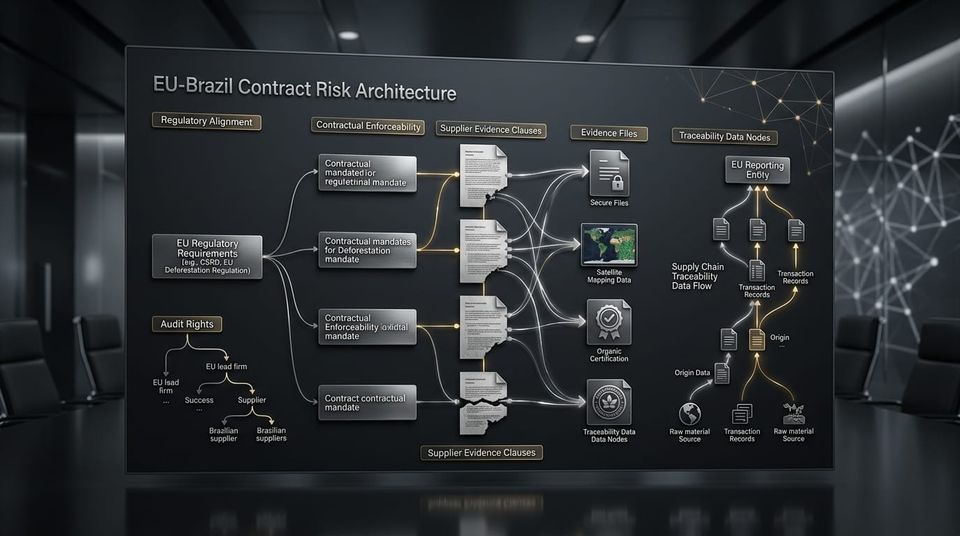

The contract is no longer only a legal document. It is becoming an evidence architecture.

European buyers are increasingly using supplier contracts to formalize evidence obligations. These clauses may involve audit rights, reporting duties, cooperation obligations, traceability records, origin documentation, emissions data, product information, supplier declarations and due diligence support.

For Brazilian suppliers, the commercial risk is not only whether the clause can be signed. The real question is whether the supplier can produce the evidence needed to support the clause if the buyer asks for documentation.

The Contract Clause Risk Review helps companies identify which contractual obligations are supported by existing evidence, which are only partially supported and which may create exposure if accepted without stronger documentation.

Decision Trigger for CFOs and Procurement Teams

If a European buyer inserts audit, traceability, reporting or carbon-data clauses into a supplier contract, can the company prove the commitments behind the signature?

Who this review is for

Brazilian suppliers negotiating with European buyers

Companies reviewing buyer contracts, supplier codes, procurement terms or due diligence annexes linked to European value chains.

Exporters receiving contract evidence clauses

Exporters asked to accept clauses on reporting, origin, traceability, carbon data, audit cooperation or supplier due diligence.

Procurement, legal and compliance teams

Teams that need to understand whether supplier obligations are supported by documentation before contracts are signed or renewed.

CFOs and boards managing contract exposure

Executive teams that need visibility on whether contractual commitments could affect revenue continuity, margin, working capital or buyer confidence.

Contract Evidence Exposure

What the review identifies

The review is designed to identify evidence risk inside supplier contract clauses. It does not replace legal advice. It supports the commercial and evidentiary assessment of whether the supplier can support the obligations it is being asked to accept.

Audit rights evidence

Whether the supplier has records that can support buyer audit requests without emergency reconstruction.

Traceability clauses

Whether origin, chain-of-custody, product, shipment or supplier-tier data can support traceability obligations.

Carbon and product-data clauses

Whether carbon, embedded emissions, product identity or material data can be documented in a buyer-readable format.

Due diligence cooperation clauses

Whether the supplier can respond to evidence requests linked to CSDDD, EUDR, CBAM, CSRD, Scope 3 or buyer due diligence workflows.

Clause risk categories

Category 1

Supported Clauses

Clauses supported by existing documentation, clear data ownership and traceable records.

Category 2

Partially Supported Clauses

Clauses where evidence exists but is fragmented, incomplete, outdated or not buyer-readable.

Category 3

Unsupported Clauses

Clauses that the supplier may sign but cannot currently support with reliable documentation.

Category 4

Escalation Clauses

Clauses that may require legal, audit, tax, customs, environmental or technical specialist review before acceptance.

Executive output

At the end of the review, the company receives an executive view of contract evidence exposure designed to support commercial, procurement, legal, compliance and board-level decisions.

- Clause Evidence Gap Map.

- Supported / Partial / Unsupported clause classification.

- Buyer-readability assessment.

- Evidence ownership and documentation gap notes.

- Contract support risk indicators.

- Priority corrective action list.

- Executive summary for CFO, board, procurement, legal and compliance discussion.

- Recommended next step: evidence remediation, legal review, buyer response preparation or board evidence file.

Finance-Grade Risk Logic

Contract Evidence Risk Model

Villanova ESG prioritizes contract evidence gaps according to commercial consequence. The first correction should target the clause most likely to affect buyer review, contract timing or revenue continuity.

CER = CV × EG × BRF × TS × ER

CER = Contract Evidence Risk

CV = Contract Value

EG = Evidence Gap

BRF = Buyer Review Friction

TS = Time Sensitivity

ER = Escalation Relevance

This model is a management diagnostic framework. It is not a legal opinion, audit conclusion, certification or guarantee of buyer acceptance.

What this review is not

This review is not a legal opinion, contract drafting service, audit assurance, certification, tax opinion, customs filing service, emissions verification or guarantee of buyer acceptance.

It is an executive evidence architecture review designed to identify whether supplier evidence can support contractual obligations before those obligations become buyer friction, audit pressure or board-level exposure.

Regulatory Source Trail

This review is informed by European regulatory and reporting frameworks that increase buyer attention to supplier evidence, due diligence, traceability, carbon data and value-chain documentation.

- Directive (EU) 2024/1760 on corporate sustainability due diligence entered into force on 25 July 2024 and focuses on responsible corporate behaviour across operations and global value chains.

- The European Commission states that CBAM applies in its definitive regime from 2026, increasing the importance of embedded emissions data and related import documentation.

- The EU Deforestation Regulation focuses on deforestation-free products and due diligence obligations connected to relevant commodities and products.

- Companies subject to CSRD must report according to European Sustainability Reporting Standards, increasing pressure on structured value-chain information.

Sources: European Commission, EUR-Lex, European Commission Taxation and Customs Union, European Commission Environment, European Commission Finance.

Related Villanova ESG review services

30-Day Supplier Evidence Readiness Review

Executive diagnostic for identifying whether supplier evidence is ready, partial, missing or not buyer-readable.

EU-Brazil Supply Chain Risk Review

Mapping of regulatory exposure, buyer evidence needs, supplier documentation gaps and commercial risk points in Brazil-Europe supply chains.

Board Evidence File Review

Structuring of supplier evidence for executive, board-level and buyer-facing risk review.

CBAM / EUDR Evidence Review

Evidence-readiness support for supplier data, origin, traceability, embedded emissions, product scope and buyer documentation requests.

Executive Contact

Request a Contract Clause Risk Review

Villanova ESG supports Brazilian suppliers, exporters, European buyers and board-level teams with supplier evidence reviews, contract clause risk analysis and executive evidence architecture.

To assess whether supplier evidence can support European buyer contract clauses, contact:

contact@villanovaesg.com

Request a Clause Risk Review