CBAM 2026: Why Carbon Data Became a Cash-Flow File

CBAM 2026 · EU-Brazil Supply Chain Risk · Carbon Data · CFO Exposure

CBAM 2026: Why Carbon Data Became a Cash-Flow File

CBAM is no longer a future compliance discussion. Since 2026, carbon data has become a financial file for EU-facing supply chains. For Brazilian suppliers, the exposure is not only regulatory. It is commercial, contractual and cash-flow related.

Risk Vector

Embedded Emissions

Board Impact

Cost, Margin & Contract Exposure

Supplier Requirement

Buyer-Readable Carbon Evidence

The strategic mistake is to treat CBAM as a European importer problem only.

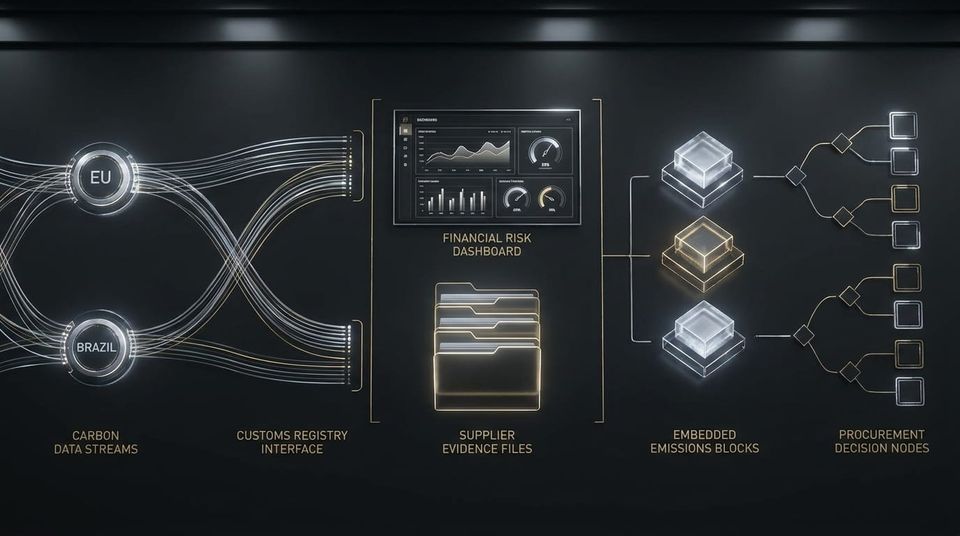

Legally, CBAM obligations sit primarily with EU importers or authorised CBAM declarants. Commercially, however, the pressure moves upstream. European buyers will need reliable supplier data to calculate embedded emissions, assess exposure, maintain customs continuity and defend procurement decisions.

That is where Brazilian suppliers become exposed.

The supplier that cannot provide structured, traceable and finance-readable carbon data may still have a product. But it becomes harder for an EU buyer to price, justify, contract and defend that product inside the organisation.

The CFO Issue Is Not the Regulation. It Is the Conversion of Carbon Data Into Financial Exposure.

CBAM changes the financial role of emissions information. Carbon data is no longer a sustainability appendix. It becomes an input for landed cost, working capital, contract pricing and supplier comparison.

Finance Exposure Logic

CBAM Exposure = Imported Volume × Embedded Emissions × Applicable Carbon Price Adjustment × Data Confidence Factor

This formula cannot be completed with generic ESG claims. It requires product-level data, operational evidence, emissions calculation logic and documentation that a buyer can use.

Why Brazilian Suppliers Should Not Wait for Buyer Pressure

1. Procurement will ask for usable data

European procurement teams need information that can be tested, reconciled and inserted into internal risk files. A PDF sustainability statement is not enough.

2. Carbon uncertainty becomes price pressure

If emissions data is weak, buyers may price uncertainty into negotiations. The supplier may face margin pressure before any formal dispute exists.

3. Contract teams will seek evidence obligations

Carbon data gaps can move into contract clauses, warranties, data delivery obligations and audit rights.

4. Board files need defensibility

EU buyers do not only need supplier data. They need supplier data that can support internal governance, audit trails and regulatory defensibility.

The Supplier Evidence Gap

Many Brazilian suppliers are not failing because they lack operational substance. They are exposed because their evidence is not structured for European use.

Operational Data

Production route, input origin, volumes, suppliers and process boundaries.

Carbon Logic

Embedded emissions calculation, assumptions, emission factors and verification readiness.

Buyer File

Evidence formatted for procurement, finance, compliance and board-level review.

What EU Buyers Are Likely to Demand From Brazilian Suppliers

| Buyer Question | Supplier Evidence Required | Financial Risk If Missing |

|---|---|---|

| What is the embedded emissions profile? | Product-level emissions data and calculation method. | Pricing uncertainty and procurement hesitation. |

| Can the data be reconciled? | Operational records, volume logic and data trail. | Lower buyer confidence and greater audit friction. |

| Who owns the assumptions? | Documented methodology, boundaries and responsible parties. | Contractual disputes and liability transfer attempts. |

| Can the file support regulatory defensibility? | Buyer-readable evidence package. | Supplier replacement risk or tighter commercial terms. |

Decision Trigger for CFOs

The CFO should not ask whether the company has a sustainability report.

The correct question is whether the supplier can produce carbon evidence that protects price, contract continuity and buyer confidence under CBAM exposure.

If the answer is unclear, the issue is not communication. It is evidence architecture.

The Villanova ESG View

CBAM will not reward Brazilian suppliers for broad ESG narratives. It will reward suppliers capable of delivering operational, carbon and traceability evidence in a format European buyers can use.

This is the commercial gap between Brazilian execution and European regulatory defensibility.

The companies that move first will not simply appear more sustainable. They will become easier to evaluate, easier to contract and easier to defend inside EU-facing procurement and finance processes.

Regulatory Source Trail

- European Commission — Carbon Border Adjustment Mechanism official page.

- European Commission — CBAM Registry and Reporting.

- European Commission — CBAM successfully entered into force on 1 January 2026.

- Regulation (EU) 2023/956 establishing the Carbon Border Adjustment Mechanism.

This article provides strategic regulatory risk analysis. It does not constitute legal, tax or customs advice.

30-Day Supplier Evidence Readiness Review

Villanova ESG supports EU-facing suppliers and buyers in reviewing whether supplier evidence is structured, buyer-readable and defensible for European procurement, compliance and board-level documentation.

The review focuses on evidence architecture, supplier documentation, traceability logic, carbon data readiness and regulatory risk exposure.

Request a Supplier Evidence Readiness ReviewContact: contact@villanovaesg.com