Financial Provisioning for Environmental Liabilities: The Direct Impact on Dividend Distribution

The End of Off-Balance-Sheet Environmental Risk

For decades, corporate treasuries treated environmental liabilities as contingent risks—relegated to the footnotes of the annual report and rarely impacting the core financial statements unless a massive, public disaster occurred. The integration of the Corporate Sustainability Reporting Directive (CSRD) and the new IFRS Sustainability Disclosure Standards (IFRS S1 and S2) has violently closed this accounting loophole.

Environmental and climate-related risks must now be mathematically quantified and formally recognized on the corporate balance sheet. If a multinational matrix or a Latin American exporter operates with unmapped supply chain risks, historical deforestation liabilities, or high carbon-intensity assets facing future CBAM taxation, international auditors are now legally mandated to force the CFO to create immediate financial provisions for these future losses. This is not an abstract ESG rating adjustment; it is a direct, mathematical deduction from the company’s current Net Income.

The Mathematics of Dividend Destruction

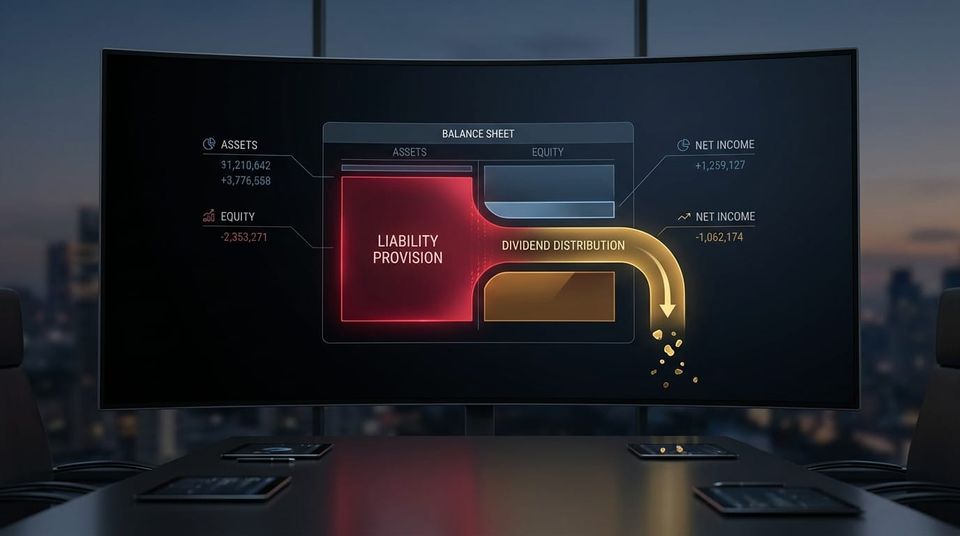

When auditors mandate the formal provisioning of environmental liabilities, the financial damage bypasses operations and directly strikes the shareholders. The math is brutal and unavoidable.

- Net Income Compression: Financial provisions are recognized as immediate expenses on the Profit and Loss (P&L) statement. A $50 million provision for future environmental remediation or anticipated CSDDD cross-border fines instantly erases $50 million from the Net Income, severely depressing the Earnings Per Share (EPS).

- The Dividend Slash: Corporate dividend distribution policies are mathematically tethered to Net Income. When mandatory environmental provisioning slashes profitability, the Board of Directors is forced to cut the dividend yield. For income-focused institutional investors, a sudden, unforecasted dividend cut is a catastrophic event, triggering an immediate and aggressive sell-off of the corporate stock.

- The Valuation Multiplier Effect: The market heavily penalizes companies that surprise investors with massive liability provisions. The resulting loss of investor trust structurally compresses the company's Price-to-Earnings (P/E) ratio, destroying Enterprise Value far beyond the actual dollar amount of the provision itself.

(Source reference: International Financial Reporting Standards (IFRS) guidelines on provisions, contingent liabilities, and the integration of climate-related risks in financial statements).

The "Worst-Case Scenario" Auditing Trap

The critical danger for the CFO lies in the "data void." When independent financial auditors review a company's exposure to European directives (EUDR, CSDDD), they require forensic proof of compliance.

If the corporate board cannot provide georeferenced, cryptographically sealed data proving that their deep-tier supply chain is free of environmental infractions, the auditor applies the principle of conservatism. They will mathematically assume the worst-case scenario—maximum regulatory fines and full remediation costs—and force the CFO to provision for that extreme amount. The lack of primary data directly inflates the financial provision, maximizing the destruction of shareholder dividends.

The Villanova ESG Shield: Strategic Intervention

At Villanova ESG, we engineer the forensic data architecture required to defend your balance sheet from aggressive auditor assumptions. We protect your Net Income and your shareholders' yield through our four uncompromising pillars:

- P&L and Revenue Protection: We defend your Net Income against forced environmental provisioning. By providing auditors with mathematical, unassailable proof of your supply chain's regulatory compliance, we eliminate the "worst-case scenario" assumptions, minimizing liability provisions and protecting your Earnings Per Share (EPS) and dividend distribution capacity.

- Logistical Reality Audit: We eradicate the data voids that trigger auditor panic. We execute deep-tier, georeferenced audits of your physical operations and supply chain, extracting the primary, cryptographic truth required to mathematically prove the absence of hidden environmental liabilities to international accounting firms.

- Cross-Border Regulatory Shield: We perfectly align your operational reality with the strict financial reporting mandates of the CSRD and IFRS S2. We ensure that your risk quantification is accurate, defensible, and structurally immune to cross-border regulatory shocks, protecting the integrity of your consolidated financial statements.

- Cost of Capital Optimization: A balance sheet free of unverified environmental provisions is a premium financial asset. By protecting your dividend yield and proving structural resilience, we maintain the attractiveness of your equity to institutional investors and leverage this stability to negotiate Sustainability-Linked Loans (SLLs), aggressively reducing your Weighted Average Cost of Capital (WACC).

Unmapped environmental risks are actively destroying your Net Income and threatening your dividend distributions. Do not allow data voids to force massive liability provisions onto your balance sheet. Contact our risk assessment team immediately to structure your cross-border regulatory shield and defend your corporate valuation at contact@villanovaesg.com

Marcio Villanova CEO, Ecobraz | Founder, Villanova ESG