CBAM and Brazilian Exporters: Why Embedded Emissions Become Cash-Flow Risk

Villanova ESG | Executive Regulatory Dossier

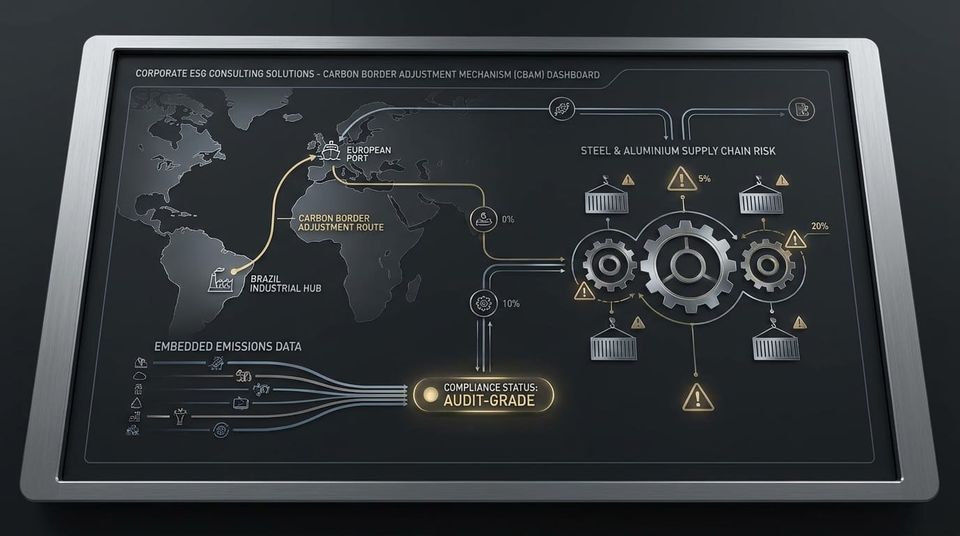

CBAM and Brazilian Exporters: Why Embedded Emissions Become Cash-Flow Risk

The Carbon Border Adjustment Mechanism changes the financial logic of carbon-intensive exports into Europe. For Brazilian exporters, the issue is no longer limited to operational emissions. The decisive question is whether embedded emissions data can be measured, documented and defended before European buyers translate uncertainty into commercial pressure.

Risk Vector

Embedded Emissions

CBAM places a carbon cost signal on selected imported goods entering the EU, based on emissions embedded in production.

Financial Exposure

Cash-Flow Pressure

Poor emissions data can create pricing friction, buyer hesitation, contract renegotiation and margin compression.

Board Relevance

Carbon Defensibility

Carbon data becomes board-relevant when it affects access to European customers, pricing power and contractual continuity.

The Strategic Change

CBAM is not a generic sustainability rule. It is a carbon cost adjustment mechanism applied at the EU border. Its function is to place a fair price on carbon emitted during the production of certain carbon-intensive goods entering the European Union.

For Brazilian exporters, the first exposure may not appear as a direct legal obligation imposed by Brussels. It may appear as pressure from EU importers. European buyers need data. Importers need declarations. Customs systems need validation. Finance teams need cost visibility. Procurement teams need lower-risk suppliers.

Board-Level Interpretation

CBAM converts emissions data from a technical metric into a commercial qualification factor. The exporter that cannot document embedded emissions may become more expensive, less predictable and harder to defend inside a European procurement file.

Why Brazilian Exporters Are Exposed

Brazil may not be the largest CBAM-origin market in every covered category. That is not the central point. The exposure is product-specific, buyer-specific and contract-specific. A Brazilian exporter selling CBAM-covered goods, components or inputs into European value chains can face pressure to provide emissions data that is reliable enough for the EU importer’s compliance process.

Exporter Data Gap

- Embedded emissions calculated inconsistently across facilities.

- Energy consumption records disconnected from product-level outputs.

- Supplier inputs lacking emissions traceability.

- Operational data stored outside an audit-ready structure.

- Carbon evidence prepared reactively after buyer pressure begins.

European Importer Concern

- Can the exporter provide actual emissions data?

- Can the methodology be explained and reviewed?

- Can product-level emissions be linked to production records?

- Can documentation support annual declarations?

- Can the importer avoid customs and compliance disruption?

Finance-Grade Risk Formula

CBAM Cash-Flow Exposure Model

CBAM Cash-Flow Exposure = EU Revenue Dependency × Embedded Emissions Intensity × Certificate Cost Signal × Data Uncertainty Factor

This is a board-level risk model, not a statutory formula. To quantify it, a company needs internal data: EU revenue exposure, product category, production emissions, energy source, export volumes, buyer concentration, contract terms, declared carbon price paid outside the EU and expected compliance cost.

The CFO Problem: Carbon Data Becomes Margin Risk

CFOs should not treat CBAM as a technical issue owned only by sustainability or operations. CBAM creates a direct interface between emissions data, import compliance and pricing economics. If the European importer carries a higher compliance burden because the exporter cannot provide reliable information, that burden may return to the exporter through commercial pressure.

The practical financial impact can appear through slower onboarding, buyer preference for better-documented suppliers, price discounts, additional verification costs, contract clauses, working capital pressure or reduced renewal probability. The exposure is not only environmental. It is contractual and financial.

CFO Diagnostic Question

If a European importer requested product-level embedded emissions evidence this month, could the company deliver a defensible file — or only a spreadsheet built after the request arrived?

What a CBAM-Ready Evidence File Should Include

A CBAM-ready evidence file should connect emissions calculation, operational records and commercial exposure. It should not be a generic carbon statement. It should help the EU importer understand whether the exporter’s data can support the compliance process.

1. Product Classification

Identification of goods, inputs, production routes and export flows that may fall within CBAM-covered categories.

2. Embedded Emissions Calculation

Structured calculation logic linking production activity, energy use, process emissions and product-level output.

3. Source Data Traceability

Records that connect emissions values to invoices, metering data, production logs, facility controls and supplier inputs.

4. Commercial Exposure Map

Revenue, volume, contract and customer mapping to estimate where CBAM-related friction can affect cash flow.

Brazil-Europe Evidence Bridge

Where Villanova ESG Fits

Villanova ESG supports companies that need to translate Brazilian operational and emissions evidence into European-facing regulatory documentation. The objective is not climate marketing. The objective is carbon-data defensibility for commercial, compliance and finance teams.

In CBAM-exposed trade, weak documentation can become a pricing problem. Strong documentation can reduce uncertainty, support buyer conversations and improve the company’s position in procurement and finance discussions.

Decision Trigger for CFOs

A CFO should trigger a CBAM evidence review when at least one of the following conditions exists:

- The company exports or supplies goods connected to cement, iron and steel, aluminium, fertilisers, electricity or hydrogen value chains.

- European customers are requesting embedded emissions data.

- Revenue depends on EU importers that must manage CBAM obligations.

- Carbon data is not connected to product-level records.

- Emissions calculations depend on manual spreadsheets without audit structure.

- Commercial teams cannot explain how CBAM could affect price, margin or contract renewal.

Executive Position

Under CBAM, emissions data quality becomes part of export competitiveness. The exporter with stronger carbon evidence may carry lower commercial friction than the exporter that treats emissions as an afterthought.

Regulatory Source Trail

This dossier is based on official regulatory references. The analysis does not create legal advice and does not guarantee compliance outcomes. Company-specific risk assessment requires product classification, emissions data, contract exposure, customs documentation and jurisdiction-specific legal review.

- European Commission — Carbon Border Adjustment Mechanism: official CBAM page.

- European Commission — CBAM Registry and Reporting: official registry and reporting page.

- European Commission — CBAM successfully entered into force on 1 January 2026: official news release.

Executive Review

Assess CBAM Evidence Before Embedded Emissions Become Margin Pressure

Villanova ESG supports companies exposed to European regulatory pressure by structuring operational, emissions and supplier evidence into board-level documentation. The objective is regulatory defensibility, carbon-data clarity and financial exposure reduction.

For confidential executive reviews: contact@villanovaesg.com